|

시장보고서

상품코드

1833681

수면무호흡증용 임플란트 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Sleep Apnea Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

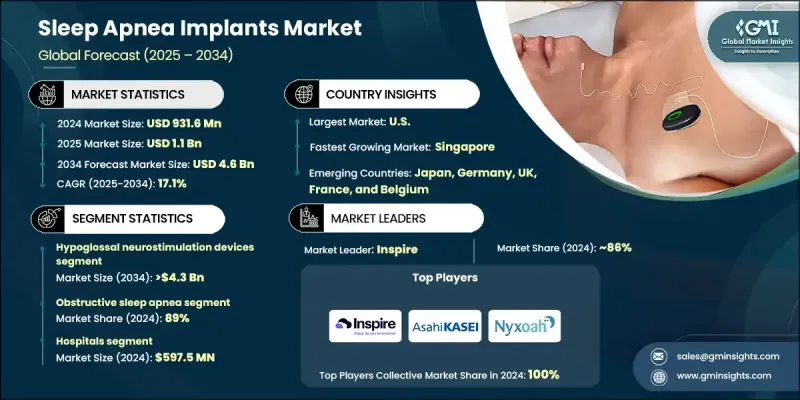

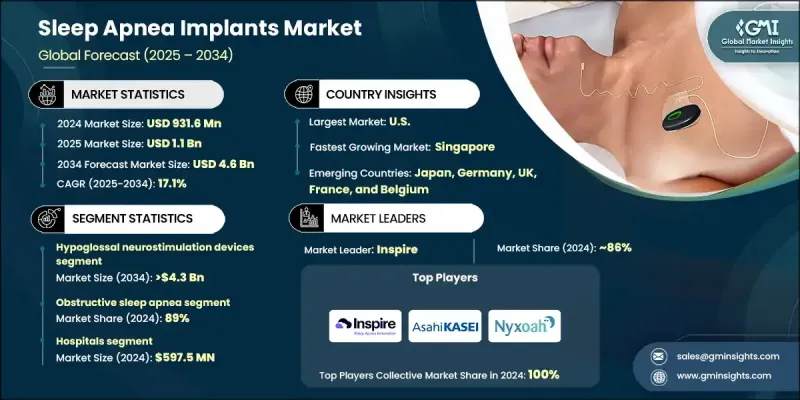

세계 수면무호흡증용 임플란트 시장은 2024년에는 9억 3,160만 달러로 평가되었으며, CAGR 17.1%로 성장하고, 2034년에는 46억 달러에 달할 것으로 추정됩니다.

이러한 급격한 성장은 폐쇄성 수면무호흡증 유병률 증가, CPAP 치료의 제한적인 순응도, 수면 관련 건강 상태에 대한 인식의 증가에 의해 촉진되고 있습니다. 수면무호흡증 임플란트는 마스크 기반 치료의 대안으로, 수면 중 막힘을 방지하기 위해 기도 근육을 자극하여 수면 중 막힘을 방지하는 최소침습적이고 마스크가 필요 없는 솔루션을 제공합니다. 많은 환자들이 기존 치료법에 대한 불편함, 불내성, 불편함을 느끼기 때문에 이러한 장치들이 인기를 끌고 있습니다. 임상적 혁신과 환자 친화적인 장치에 대한 관심이 높아지면서 임플란트는 장기적이고 효과적인 솔루션을 원하는 환자들에게 중요한 선택이 되고 있습니다. 또한, 의사의 지지 증가, 기술 발전, 치료되지 않은 OSA와 심혈관, 대사, 신경학적 위험의 연관성에 대한 인식이 높아짐에 따라 시장이 확대되고 있습니다. 경쟁 구도는 Inspire, Nyxoah, Asahi Kasei와 같은 대기업이 주도하고 있으며, 대기업은 광범위한 제품 포트폴리오와 전 세계적인 영향력을 활용하는 반면, 중소기업은 틈새 기술과 집중적인 연구 노력으로 성장을 도모하고 있습니다. 이러한 역동성이 결합되어 전 세계적으로 수면무호흡증 치료의 변화를 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034 |

| 시장 규모 | 9억 3,160만 달러 |

| 예측 금액 | 46억 달러 |

| CAGR | 17.1% |

설하 신경 자극기 부문은 2024년 86.7%의 점유율을 차지했으며, 입증된 임상 결과, 의사의 선호도, 기존 치료법에 불내성이 있는 환자들에 대한 폭넓은 채택이 뒷받침되고 있습니다. CPAP의 장기적인 순응도에는 한계가 있으며, 환자의 약 1/3만이 꾸준히 사용하는 것으로 나타나 삶의 질과 편의성을 향상시키는 이식형 옵션에 대한 수요가 더욱 증가하고 있습니다.

폐쇄성 수면무호흡증은 OSA의 높은 유병률과 기존 치료법의 단점으로 인해 2024년 89%의 점유율을 차지했습니다. 수백만 명의 환자가 진단을 받지 못했지만, 이 질환이 심장병, 당뇨병, 인지기능 저하와 관련이 있다는 인식이 높아지면서 장기적으로 혜택을 줄 수 있는 임플란트 치료를 추진하는 원동력이 되고 있습니다.

병원 부문은 2024년 5억 9,750만 달러를 벌어들일 것으로 예상되며, 임플란트 치료가 그 원동력이 되고 있습니다. 병원의 우위는 첨단 인프라, 전문 외과의사 확보, 종합적인 수술 후 관리, 설하신경자극기, 호흡신경자극기 등 장치의 안전한 삽입과 지속적인 모니터링에 기인합니다. 다학제적 팀과 첨단 진단 도구가 병원 내 도입률을 더욱 높이고 있습니다.

미국 수면무호흡증 임플란트 시장 규모는 2024년 8억 4,000만 달러에 달했습니다. 이 지역의 성장 원동력은 많은 OSA 환자 수, 유리한 상환 제도, 이식형 기기의 조기 도입입니다. 탄탄한 의료 인프라와 활발한 임상 연구, 그리고 Asahi Kasei, Inspire Medical Systems, Nyxoah와 같은 기업의 존재가 이 분야에서 일본의 리더십을 견인하고 있습니다.

수면무호흡증용 임플란트 업계의 유력 기업으로는 Inspire, Nyxoah, Asahi Kasei 등이 있습니다. 수면무호흡증용 임플란트 시장에서 발판을 마련하기 위해 각 업체들은 제품 혁신, 임상 연구, 지역 확대를 중심으로 전략을 펼치고 있습니다. 각 업체들은 기존 치료법보다 순응도를 높일 수 있는 최소침습적이고 환자 친화적인 기기 개발에 많은 투자를 하고 있습니다. 임상시험 프로그램의 확대는 유효성을 검증하고, 규제 당국의 승인을 확보하고, 의사들의 신뢰를 구축하는 데에도 필수적입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 폐쇄성 수면무호흡증 유병률 증가

- CPAP에 대한 낮은 순응도와 준수율

- 기술적 진보

- 수면무호흡증에 관한 인식 확산

- 업계의 잠재적 리스크와 과제

- 수면무호흡증용 임플란트의 고비용

- 수면무호흡증용 임플란트 관련 합병증

- 시장 기회

- OSA로 진단되는 환자 수 증가

- 신흥 시장에 대한 진출

- 성장 촉진요인

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 미국

- 유럽

- 테크놀러지와 혁신 상황

- 현재 기술 동향

- 신기술

- 향후 시장 동향

- 신흥국에서의 도입

- OSA 발생률과 유병률, 2021-2024

- 제품 파이프라인 분석

- 기동 시나리오

- 가격 분석, 2024

- 투자 상황

- 소비자 행동 분석

- 환자 여정 맵

- Porters 분석

- PESTEL 분석

- 격차 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 미국

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정과 예측 : 제품별, 2021-2034

- 주요 동향

- 설하 신경자극 기기

- 횡격막 신경자극 기기

제6장 시장 추정과 예측 : 적응증별, 2021-2034

- 주요 동향

- 폐쇄성 수면무호흡증

- 중추성 수면무호흡증

제7장 시장 추정과 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래 수술 센터

제8장 시장 추정과 예측 : 지역별, 2021-2034

- 주요 동향

- 미국

- 유럽

- 독일

- 영국

- 스위스

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 벨기에

- 오스트리아

- 핀란드

- 일본

- 싱가포르

제9장 기업 개요

- Asahi Kasei

- Inspire

- Nyxoah

The Global Sleep Apnea Implants Market was valued at USD 931.6 million in 2024 and is estimated to grow at a CAGR of 17.1% to reach USD 4.6 billion by 2034.

This rapid growth is being propelled by the rising prevalence of obstructive sleep apnea, limited compliance with CPAP therapy, and increasing awareness of sleep-related health conditions. Sleep apnea implants provide an alternative to mask-based treatments, offering minimally invasive, mask-free solutions that stimulate airway muscles to prevent obstruction during sleep. These devices are gaining traction as many patients experience discomfort, intolerance, or inconvenience with conventional therapies. With clinical innovations and a growing focus on patient-friendly devices, implants are becoming a critical option for individuals seeking long-term, effective solutions. The market is also expanding due to growing physician support, technological advancements, and heightened recognition of the link between untreated OSA and cardiovascular, metabolic, and neurological risks. Major players such as Inspire, Nyxoah, and Asahi Kasei are shaping the competitive landscape, with larger companies leveraging extensive product portfolios and global reach while smaller firms drive growth through niche technologies and focused research efforts. Collectively, these dynamics are driving a transformative shift in sleep apnea treatment worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $931.6 Million |

| Forecast Value | $4.6 Billion |

| CAGR | 17.1% |

The hypoglossal neurostimulation devices segment held 86.7% share in 2024, supported by proven clinical outcomes, physician preference, and widespread adoption among patients intolerant to traditional therapies. The limited long-term adherence to CPAP, with only about one-third of patients maintaining consistent use, has further reinforced demand for implantable options that offer improved quality of life and convenience.

The obstructive sleep apnea segment held an 89% share in 2024, driven by the high prevalence of OSA and the shortcomings of conventional treatment methods. Millions of individuals remain undiagnosed, yet awareness of the condition's connection to heart disease, diabetes, and cognitive decline is rising, driving the push for implant-based therapies that can deliver long-term benefits.

The hospitals segment generated USD 597.5 million in 2024, driven by the implant procedures. Their dominance stems from advanced infrastructure, availability of expert surgeons, and comprehensive post-operative care, ensuring safe implantation and ongoing monitoring of devices such as hypoglossal and phrenic nerve stimulators. Multidisciplinary teams and advanced diagnostic tools further strengthen hospital adoption rates.

United States Sleep Apnea Implants Market was valued at USD 840 million in 2024. Growth in the region is fueled by the high number of OSA patients, favorable reimbursement frameworks, and early adoption of implantable devices. A robust healthcare infrastructure, combined with active clinical research and the presence of companies like Asahi Kasei, Inspire Medical Systems, and Nyxoah, continues to drive the country's leadership in this space.

Prominent players in the Sleep Apnea Implants Industry include Inspire, Nyxoah, and Asahi Kasei. To strengthen their foothold in the sleep apnea implants market, companies are implementing strategies centered on product innovation, clinical research, and regional expansion. Firms are investing heavily in developing minimally invasive, patient-friendly devices that improve adherence compared to traditional therapies. Expanding clinical trial programs is also critical to validate efficacy, secure regulatory approvals, and build physician confidence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Indication channel trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of obstructive sleep apnea

- 3.2.1.2 Low compliance and adherence towards CPAP

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness regarding sleep apnea

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of sleep apnea implants

- 3.2.2.2 Complications associated with sleep apnea implants

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing number of diagnosed OSA patients

- 3.2.3.2 Expansion into emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Future market trends

- 3.8 Adoption in emerging countries

- 3.9 Hypoglossal neurostimulation devices market, 2021 - 2034 (Units)

- 3.10 Incidence and prevalence of OSA, 2021-2024

- 3.11 Product pipeline analysis

- 3.12 Start-up scenario

- 3.13 Pricing analysis, 2024

- 3.14 Investment landscape

- 3.15 Consumer behaviour analysis

- 3.16 Patient journey map

- 3.17 Porter's analysis

- 3.18 PESTEL analysis

- 3.19 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 U.S.

- 4.2.2 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hypoglossal neurostimulation devices

- 5.3 Phrenic nerve stimulators

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Obstructive sleep apnea

- 6.3 Central sleep apnea

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 U.S.

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Switzerland

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Italy

- 8.3.7 Netherlands

- 8.3.8 Belgium

- 8.3.9 Austria

- 8.3.10 Finland

- 8.4 Japan

- 8.5 Singapore

Chapter 9 Company Profiles

- 9.1 Asahi Kasei

- 9.2 Inspire

- 9.3 Nyxoah