|

시장보고서

상품코드

1844263

고인산혈증 치료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Hyperphosphatemia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

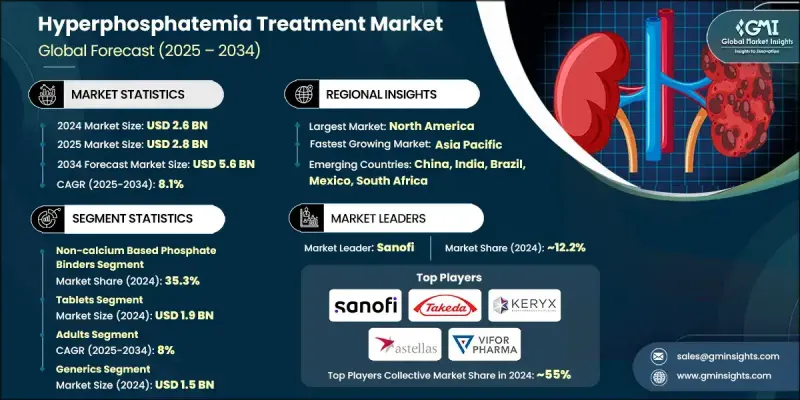

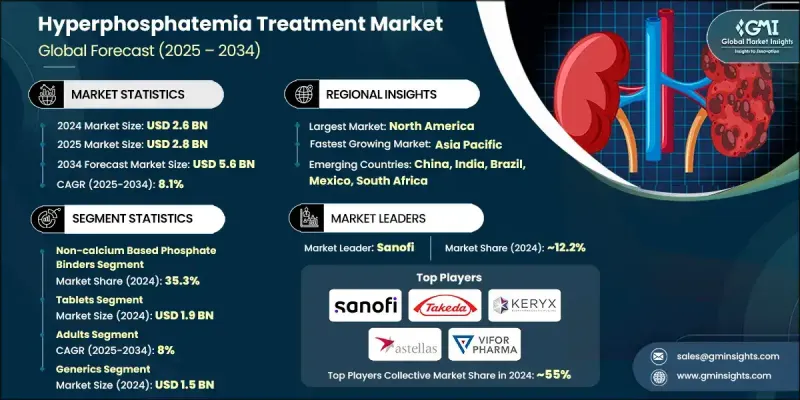

세계의 고인산혈증 치료 시장 규모는 2024년에는 26억 달러로 평가되었고, CAGR 8.1%로 성장할 전망이며, 2034년에는 56억 달러에 이를 것으로 추정됩니다.

만성 신장병(CKD) 환자 증가, 말기 신장병(ESRD) 환자 수 확대, 세계적인 투석 도입 증가가 성장의 원동력이 되고 있습니다. 인구의 고령화는 당뇨병 및 고혈압의 이환율 상승과 함께 세계적인 CKD 유병률의 상승을 촉진하고 있으며, 고인산혈증 치료제 수요에 직접적인 영향을 주고 있습니다. 가공식품이나 앉아만 있는 생활로의 시프트도 인산염 불균형의 원인이 되어, 환자를 장기의 치료 요법으로 내몰고 있습니다. 이에 따라 치료법은 급속히 진화하고 있으며, 종래의 칼슘계 결합제에 그치지 않고 철계 결합제 및 인산염 흡수 억제제 등 보다 혁신적인 선택으로 이행하고 있습니다. 이러한 차세대 요법은 내약성이 개선되어 부작용이 적고 어드히어런스와 치료 성적이 향상됩니다. 규제 당국의 승인과 임상시험 증가에 따라, 비칼슘 결합제 및 신규 약제는 지역 간에 보다 널리 채용되고 시장의 장기적인 기세를 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 26억 달러 |

| 예측 금액 | 56억 달러 |

| CAGR | 8.1% |

2024년 비칼슘계 인산염 결합제의 점유율은 35.3%로 평가되었고, 2034년에는 CAGR 8%의 성장률로 20억 달러에 달할 것으로 예측됩니다. 이러한 치료제는 정제의 크기가 작고 위장의 불편함을 줄여 환자의 복약 충동을 향상시킵니다. 고인산혈증에는 평생 치료가 필요하기 때문에 보다 편리하고 내약한 선택을 요구하는 환자 수요가 꾸준히 증가하고 있습니다. 의료 제공자와 투석 센터는 심혈관 결과 개선과 인산염 조절 강화에 중점을 둔 현대의 가치관에 근거한 케어 목표와의 무결성을 통해 비칼슘 결합제를 점점 선호하게 되어 시장 확대에 있어서 이 부문의 역할을 강화하고 있습니다.

성인 환자 그룹은 2034년까지 연평균 복합 성장률(CAGR) 8%로 성장할 전망입니다. 40세 이상의 성인은 만성 신장병과 ESRD 모두에서 가장 위험한 층이며 인산염 감소 치료의 가장 큰 소비자가 되었습니다. 세계 성인 CKD 인구가 증가함에 따라 고인산혈증 치료제에 대한 수요는 특히 신장 전문의 및 투석 센터에 대한 접근이 보급되는 시장에서 계속 확대되고 있습니다. 첨단 지역에서는 체계화된 치료 프로토콜과 조기 개입의 틀이 진단 및 치료 규정 준수를 개선하고 성인 지역 시장 우위를 유지하는 데 도움이 됩니다.

북미의 고인산혈증 치료 2024년 시장 점유율은 44.3%로 미국이 지역별 수익의 최대 부분을 차지했습니다. CKD의 높은 부담과 투석의 보급이 이 지역 전체의 인산강하약에 대한 왕성한 수요를 견인하고 있습니다. 선도적인 공급자가 관리하는 투석 클리닉 네트워크가 확립되어 있어 신뢰할 수 있는 인산염 모니터링 및 일관된 치료가 가능합니다. 이러한 인프라는 전통적인 치료와 차세대 치료 모두의 확대를 지원하고 있으며, 북미는 세계 시장의 역학과 치료 혁신을 형성하는 중심적인 존재가 되고 있습니다.

세계의 고인산혈증 치료 시장을 형성하고 있는 주요 기업으로는 Fresenius Medical Care, Vifor Pharma (CSL Limited), Dr. Reddy's, Takeda Pharmaceuticals, Astellas Pharma, Sanofi, Lupin, Cipla, Glenmark, Teva Pharmaceuticals, Amneal, Mitsubishi Tanabe Pharma, Aurobindo Pharma, Macleods 및 Keryx Biopharmaceuticals 등이 있습니다. 고인산혈증 치료 시장에서 사업을 전개하는 기업은 의약품의 혁신과 전략적 라이선싱 계약을 통해 치료 포트폴리오의 확대에 주력하고 있습니다. 많은 기업들이 보다 뛰어난 안전성 프로파일과 환자 결과를 개선하는 비칼슘 및 철 기반 결합제를 개발하기 위한 임상 연구에 투자하고 있습니다. 투석 네트워크와 신장 내과 클리닉과의 제휴는 일관된 유통과 환자 접근을 보장하는 데 도움이 됩니다. 사노피와 비포파마와 같은 기업들은 지역적인 제휴를 통해 세계 전개를 강화하고 있으며, 시플러와 테바 파머슈티컬즈와 같은 제네릭 의약품 제조업체는 비용 효율적인 제제로 신흥 시장에 진출하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성신장병(CKD) 및 투석환자의 유병률 상승

- 고령화 및 생활습관병

- 의약품 개발 및 신규 치료법의 진보

- 의식 향상 및 예방 헬스케어의 대처

- 업계의 잠재적 위험 및 과제

- 약의 큰 부담 및 환자의 낮은 컴플라이언스

- 고액의 치료비

- 시장 기회

- 저약제 부담 요법의 개발

- 맞춤형 의료 및 병용 요법

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 북미

- 기술의 상황

- 현재의 기술 동향

- 신흥 기술

- 장래 시장 동향

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 칼슘계 인산 결합제

- 비칼슘계 인산 결합제

- 철계 인산 결합제

- 탄산란탄

- 기타 제품

제6장 시장 추계 및 예측 : 제형별(2021-2034년)

- 주요 동향

- 태블릿

- 분말

- 기타 제형

제7장 시장 추계 및 예측 : 연령별(2021-2034년)

- 주요 동향

- 성인

- 소아

제8장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 브랜드

- 제네릭 의약품

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 재택 케어의 설정

- 투석 센터

- 기타 용도

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Amneal

- Astellas Pharma

- Aurobindo Pharma

- Cipla

- Dr. Reddy's

- Glenmark

- Fresenius Medical Care

- Keryx Biopharmaceuticals

- Lupin

- Macleods

- Mitsubishi Tanabe Pharma

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceuticals

- Vifor Pharma(CSL Limited)

The Global Hyperphosphatemia Treatment Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 5.6 billion by 2034.

The growth is fueled by rising cases of chronic kidney disease (CKD), the expanding number of end-stage renal disease (ESRD) patients, and the increasing adoption of dialysis worldwide. An aging population, together with higher rates of diabetes and hypertension, continues to drive up CKD prevalence globally, directly impacting the demand for hyperphosphatemia treatments. The shift toward processed food and sedentary lifestyles has also contributed to phosphate imbalances, pushing patients into long-term therapeutic regimens. In response, the treatment landscape is evolving rapidly, moving beyond traditional calcium-based binders toward more innovative options like iron-based binders and phosphate absorption inhibitors. These next-generation therapies offer improved tolerability and fewer side effects, boosting adherence and outcomes. As regulatory approvals and clinical trials increase, non-calcium binders and novel agents are being adopted more broadly across regions, supporting long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 8.1% |

In 2024, the non-calcium-based phosphate binders held a 35.3% share and are anticipated to reach USD 2 billion by 2034, growing at a CAGR of 8%. These treatments offer smaller pill sizes and reduced gastrointestinal discomfort, leading to better patient adherence. As lifelong therapy is required for hyperphosphatemia, patient demand for more convenient and better-tolerated options is increasing steadily. Healthcare providers and dialysis centers increasingly prefer non-calcium binders due to their alignment with modern value-based care goals, which focus on improved cardiovascular outcomes and enhanced phosphate regulation, thereby reinforcing this segment's role in market expansion.

The adult patient group segment is growing at a CAGR of 8% throughout 2034. Adults over the age of 40 represent the highest-risk demographic for both chronic kidney disease and ESRD, making them the largest consumers of phosphate-lowering treatments. As the global adult CKD population grows, demand for hyperphosphatemia therapies continues to scale, especially in markets where access to nephrology specialists and dialysis centers is widespread. In developed regions, structured care protocols and early intervention frameworks are improving diagnosis and treatment compliance, helping maintain the adult segment's market dominance.

North America Hyperphosphatemia Treatment Market held 44.3% share in 2024, with the United States contributing the largest portion of regional revenue. The high burden of CKD and the widespread adoption of dialysis drive strong demand for phosphate-lowering drugs across the region. A well-established network of dialysis clinics, managed by leading providers, enables reliable phosphate monitoring and consistent therapy delivery. This infrastructure supports the expansion of both traditional and next-generation treatments, making North America a central force in shaping global market dynamics and therapeutic innovation.

Key players shaping the Global Hyperphosphatemia Treatment Market include Fresenius Medical Care, Vifor Pharma (CSL Limited), Dr. Reddy's, Takeda Pharmaceuticals, Astellas Pharma, Sanofi, Lupin, Cipla, Glenmark, Teva Pharmaceuticals, Amneal, Mitsubishi Tanabe Pharma, Aurobindo Pharma, Macleods, and Keryx Biopharmaceuticals. Companies operating in the hyperphosphatemia treatment market are focusing on expanding their therapeutic portfolios through drug innovation and strategic licensing deals. Many are investing in clinical research to develop non-calcium and iron-based binders that provide better safety profiles and improved patient outcomes. Partnerships with dialysis networks and nephrology clinics help ensure consistent distribution and patient access. Firms like Sanofi and Vifor Pharma are strengthening global reach through regional collaborations, while generics players such as Cipla and Teva Pharmaceuticals are entering emerging markets with cost-effective formulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Dosage form trends

- 2.2.4 Age group trends

- 2.2.5 Type trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic kidney disease (CKD) and dialysis patients

- 3.2.1.2 Aging population and lifestyle-related disorders

- 3.2.1.3 Advancements in drug development and novel therapies

- 3.2.1.4 Increasing awareness and preventive healthcare initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High pill burden and poor patient compliance

- 3.2.2.2 High treatment costs

- 3.2.3 Market opportunities

- 3.2.3.1 Development of low-pill-burden therapies

- 3.2.3.2 Personalized medicine and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Calcium-based phosphate binders

- 5.3 Non-calcium based phosphate binders

- 5.4 Iron-based phosphate binders

- 5.5 Lanthanum carbonate

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets

- 6.3 Powder

- 6.4 Other dosage forms

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adults

- 7.3 Pediatrics

Chapter 8 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Branded

- 8.3 Generics

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Homecare settings

- 9.4 Dialysis centers

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amneal

- 11.2 Astellas Pharma

- 11.3 Aurobindo Pharma

- 11.4 Cipla

- 11.5 Dr. Reddy's

- 11.6 Glenmark

- 11.7 Fresenius Medical Care

- 11.8 Keryx Biopharmaceuticals

- 11.9 Lupin

- 11.10 Macleods

- 11.11 Mitsubishi Tanabe Pharma

- 11.12 Sanofi

- 11.13 Takeda Pharmaceuticals

- 11.14 Teva Pharmaceuticals

- 11.15 Vifor Pharma (CSL Limited)