|

시장보고서

상품코드

1844301

깃털 가공 장비 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Feather Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 깃털 가공 장비 시장은 2024년에는 12억 4,000만 달러로 평가되었고, CAGR 4.8%로 성장하여 2034년에는 19억 8,000만 달러에 이를 것으로 추정되고 있습니다.

환경 친화적인 폐기물 관리를 중시하는 경향이 강해지면서 깃털 재활용 기술 채택이 크게 증가하고 있습니다. 추정에 따르면, 매년 약 800만 톤의 가금류 깃털이 발생하여 지속 가능한 이용에 큰 기회가 되고 있습니다. 과거에는 폐기물로 버려지던 이 깃털은 현재 비료, 섬유, 사료 등 유익한 제품으로 재사용되고 있습니다. 이러한 전환은 환경에 미치는 영향을 줄이는 동시에 비즈니스에 새로운 수익원을 창출할 수 있습니다. 지속가능성 목표와 환경 규정 준수 기준이 엄격해짐에 따라 제조업체들은 차세대 깃털 가공 기계에 대한 투자를 늘리고 있습니다. 이러한 발전으로 시장 상황은 변화하고 있으며, 지속가능성이 성장의 핵심 원동력이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 12억 4,000만 달러 |

| 예측 금액 | 19억 8,000만 달러 |

| CAGR | 4.8% |

지속적인 기술 개선으로 깃털의 가공 방법이 변화하고 있습니다. 자동화와 에너지 효율이 높은 기계는 생산성을 높이고, 위생 기준을 개선하며, 운영을 간소화합니다. 폐기물 처리에 대한 규제가 강화됨에 따라 식조류 처리업체들은 보다 효과적이고 환경 친화적인 솔루션을 채택하고 있습니다. 현재, 점점 더 많은 식용 조류 처리 공장이 깃털 처리 장비를 더 광범위한 렌더링 시스템과 통합하고 있습니다. 이러한 변화는 기존 워크플로우에 원활하게 적용되고, 운영의 유연성과 효율성을 높이고, 모듈식이며 설치가 용이한 기계에 대한 수요를 불러일으키고 있습니다.

탈피 장치 부문은 2024년 4억 9,730만 달러로 평가되며 2025년부터 2034년까지 연평균 4.4% 성장할 것으로 예측됩니다. 특히 신흥 경제권에서 가금류 제품에 대한 수요가 급증하면서 가공 시설들이 수작업에 대한 의존도를 줄이기 위해 자동화를 추진하고 있습니다. 탈피기는 닭고기 가공의 초기 단계에서 높은 처리 능력을 달성하고 청결을 유지하며 균일성을 보장하는 데 중요한 역할을합니다. 생산 규모가 확대됨에 따라 신속하고 위생적인 탈피 솔루션의 필요성이 더욱 중요해졌습니다.

조류 처리 시설 부문은 2024년 52.9%의 점유율을 차지할 것으로 예상되며, 2034년까지 연평균 4.5%의 성장률을 보일 것으로 예측됩니다. 전 세계적으로 가금육 소비가 지속적으로 증가함에 따라 가공업체들은 생산 능력을 확장하고, 깃털 제품별로 비용 효율적이고 위생적이며 지속 가능한 방식으로 관리하기 위해 기존 시스템을 업그레이드하고 있습니다. 깃털 세척, 탈지, 탈지, 건조, 포장을 할 수 있는 통합 시스템은 공장이 작업의 각 단계를 최적화하는 것을 목표로 하고 있기 때문에 수요가 증가하고 있습니다.

미국 깃털 가공 장비 2024년 시장 규모는 2억 6,640만 달러로 평가되었으며, 2025-2034년 연평균 4.7% 성장할 것으로 예측됩니다. 미국의 깃털 가공 산업은 높은 소비율과 엄격한 규제 프레임워크에 힘입어 강력한 국내 가금류 부문의 혜택을 누리고 있습니다. 기업들은 식품 안전 의무화, 환경 정책, 생산성 목표에 부합하기 위해 첨단 에너지 효율이 높은 자동화 설비에 많은 투자를 하고 있습니다. 이러한 발전으로 미국은 최신 깃털 처리 기술 도입의 선두주자로 자리매김하고 있습니다.

깃털 가공 기계 시장 경쟁 구도를 형성하는 주요 기업은 Kuiper &Zonen,Taizy Machinery,Bayle,TALSA,Bettcher Industries,Cantrell-Gainco,MAJA,LINCO,Baader Group,Meyn, Scott Automation, Bans, Stork(Marel), Hubbard Systems, Hubbard Systems, Ruvii 등입니다. Scott Automation, Banss, Stork(Marel), Hubbard Systems, Ruvii 등이 있습니다. 깃털 가공 기계 시장의 기업들은 시장에서의 입지를 강화하기 위해 몇 가지 전략을 채택하고 있습니다. 주요 초점은 자동화와 에너지 효율을 통한 제품 혁신으로 진화하는 지속가능성 및 규제 기준을 충족하는 데 초점을 맞추었습니다. 많은 업체들이 기존 가공 시스템에 쉽게 통합할 수 있는 모듈식 플러그 앤 플레이 솔루션으로 제품 라인을 확장하고 있습니다. 식용 조류 처리 공장과의 제휴 및 장기 서비스 계약은 기업이 반복적인 수익원을 확보하는 데 도움이 되고 있습니다. 전략적 합병과 인수합병도 기술력 강화와 지리적 범위 확대에 활용되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 표준과 컴플라이언스 요건

- 지역 규제 구조

- 인증 기준

- Porter의 Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 기기 유형별, 2021년-2034년

- 주요 동향

- 깃털 제거 장비

- 세정 및 건조 장비

- 분쇄 및 절단 장비

- 선별 및 등급 분류 장비

- 악착 및 묶음 장비

- 건조 및 탈수 시스템

- 포장 및 취급 장비

- 기타(살균 및 소독 시스템, 송풍기, 집진기 등)

제6장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 재생 깃털

- 새 깃털

제7장 시장 추산·예측 : 용량별, 2021년-2034년

- 주요 동향

- 최대 500 kg/hr

- 500-2,500 kg/hr

- 2,500 kg/hr 이상

제8장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 가금류

- 닭

- 거위

- 집오리

- 기타

- 공작

- 기타(타조 등)

제9장 시장 추산·예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 가금 가공 공장

- 가금 사육

- 축산 처리

- 다운 및 패더

- 의류

- 침구 제품

- 깃털 분말 생산자

- 예술과 공예

- 기타(비료, 건축 단열재, 여과 시스템 등)

제10장 시장 추산·예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 직접

- 간접

제11장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카공화국

제12장 기업 개요

- Baader Group

- Banss

- Bayle

- Bettcher Industries

- Cantrell-Gainco

- Hubbard Systems

- Kuiper &Zonen

- LINCO

- MAJA

- Meyn

- Ruvii

- Scott Automation

- Stork(Marel)

- TALSA

- Taizy Machinery

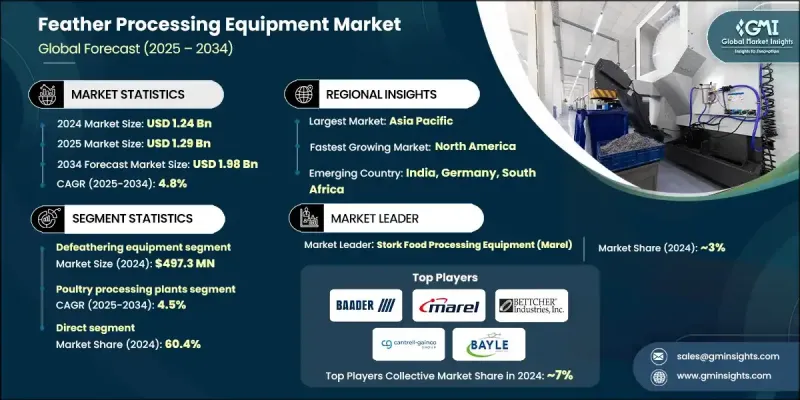

The Global Feather Processing Equipment Market was valued at USD 1.24 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 1.98 billion by 2034.

Growing emphasis on eco-friendly waste management practices is significantly driving the adoption of feather recycling technologies. According to estimates, around 8 million metric tons of poultry feathers are generated each year, presenting a major opportunity for sustainable utilization. These feathers, once discarded as waste, are now being repurposed into profitable products such as fertilizers, textiles, and animal feed. This shift is helping to cut down environmental impact while opening new revenue streams for businesses. As sustainability targets and stricter environmental compliance standards become more prominent, manufacturers are increasing investments in next-gen feather processing equipment. These developments are reshaping the market landscape, making sustainability a central driver of growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.24 Billion |

| Forecast Value | $1.98 Billion |

| CAGR | 4.8% |

Ongoing technological improvements are transforming how feather processing is carried out. Enhanced automation and energy-efficient machinery are boosting productivity, improving hygiene standards, and streamlining operations. Tighter regulations related to waste disposal are prompting poultry processors to adopt more effective and environmentally conscious solutions. A growing number of poultry processing plants are now integrating feather processing units with broader rendering systems. This shift is fueling demand for modular, easy-to-install machines that seamlessly fit into existing workflows, boosting operational flexibility and efficiency.

The defeathering equipment segment was valued at USD 497.3 million in 2024 and is forecasted to grow at a CAGR of 4.4% between 2025 and 2034. Surging demand for poultry products, particularly in emerging economies, is prompting processing facilities to automate their operations and reduce their reliance on manual labor. Defeathering machines play a critical role in achieving high throughput, maintaining cleanliness, and ensuring uniformity during the early stages of poultry processing. As production scales up, the need for fast and hygienic defeathering solutions becomes more essential.

The poultry processing facilities segment held a 52.9% share in 2024 and is projected to grow at a CAGR of 4.5% through 2034. With poultry meat consumption continuing to rise globally, processors are expanding capacity and upgrading existing systems to manage feather by-products in a cost-effective, sanitary, and sustainable manner. Integrated systems that can clean, defeather, dry, and package feathers are seeing rising demand as plants aim to optimize every step of the operation.

United States Feather Processing Equipment Market was valued at USD 266.4 million in 2024 and is expected to grow at a CAGR of 4.7% from 2025 to 2034. The U.S. feather processing industry benefits from a strong domestic poultry sector supported by high consumption rates and stringent regulatory frameworks. Companies are investing heavily in advanced, energy-efficient, and automated equipment to align with food safety mandates, environmental policies, and productivity goals. These developments are positioning the U.S. as a frontrunner in the adoption of modern feather processing technologies.

Key players shaping the competitive landscape of the Feather Processing Equipment Market include Kuiper & Zonen, Taizy Machinery, Bayle, TALSA, Bettcher Industries, Cantrell-Gainco, MAJA, LINCO, Baader Group, Meyn, Scott Automation, Banss, Stork (Marel), Hubbard Systems, and Ruvii. Companies in the Feather Processing Equipment Market are adopting several strategies to reinforce their market position. A primary focus is on product innovation through automation and energy efficiency to meet evolving sustainability and regulatory standards. Many players are expanding their product lines with modular, plug-and-play solutions that integrate easily into existing processing systems. Collaborations with poultry processing plants and long-term service agreements are helping companies secure recurring revenue streams. Strategic mergers and acquisitions are also being used to strengthen technical capabilities and broaden geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Usage

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid expansion of poultry industry

- 3.2.1.2 Increased demand for sustainable waste management

- 3.2.1.3 Rising demand for feather-based by-products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Maintenance and technical expertise

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Defeathering equipment

- 5.3 Cleaning and drying equipment

- 5.4 Grinding & cutting equipment

- 5.5 Sorting & grading equipment

- 5.6 Pressing & bunching equipment

- 5.7 Drying and dehydration systems

- 5.8 Packaging and handling equipment

- 5.9 Others (sterilization and disinfection systems, blowers, dusting, etc.)

Chapter 6 Market Estimates & Forecast, By Usage, 2021 - 2034, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Recycling feathers

- 6.3 Virgin feathers

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Upto 500 kg/hr

- 7.3 500-2,500 kg/hr

- 7.4 Above 2.500 kg/hr

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Poultry

- 8.3 Chicken

- 8.4 Goose

- 8.5 Duck

- 8.6 Others

- 8.7 Peacock

- 8.8 Others (ostrich, etc.)

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Poultry processing plants

- 9.3 Poultry rearing

- 9.4 Slaughtering

- 9.5 Down & feather

- 9.6 Clothing

- 9.7 Bedding products

- 9.8 Feather meal producers

- 9.9 Arts & crafts

- 9.10 Others (fertilizer, construction insulation, filtration system, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Baader Group

- 12.2 Banss

- 12.3 Bayle

- 12.4 Bettcher Industries

- 12.5 Cantrell-Gainco

- 12.6 Hubbard Systems

- 12.7 Kuiper & Zonen

- 12.8 LINCO

- 12.9 MAJA

- 12.10 Meyn

- 12.11 Ruvii

- 12.12 Scott Automation

- 12.13 Stork (Marel)

- 12.14 TALSA

- 12.15 Taizy Machinery