|

시장보고서

상품코드

1844307

위장관기질종양 치료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Gastrointestinal Stromal Tumor Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

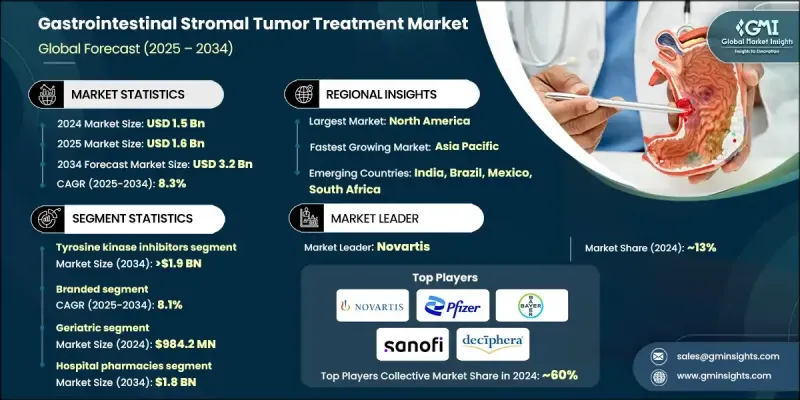

세계의 위장관기질종양 치료 시장은 2024년에는 15억 달러로 평가되었고, CAGR 8.3%로 성장할 전망이며, 2034년에는 32억 달러에 이를 것으로 추정됩니다.

이 성장은 소화기 암의 세계적인 유병률 증가와 희귀 종양 유형에 대한 의식 증가에 기인하고 있습니다. 표적 치료제, 특히 티로신 키나아제 억제제(TKI)의 진보는 치료 성과와 생존율을 현저하게 향상시킵니다. 전이성 및 치료 저항성 GIST 사례 증가로 인해 리프레티닙, 아바프리티닙, 레고라페닙과 같은 혁신적인 약물에 대한 수요가 더욱 증가하고 있으며, 이러한 약물은 질병 진행을 관리하고 다양한 병기에서 환자의 QOL을 증가시키는 데 사용됩니다. GIST의 치료는 일반적으로 경구 투여이며 병원 약국, 소매 약국 및 온라인 플랫폼을 통해 이용할 수 있습니다. 이러한 치료에는 티로신 키나아제 억제제, 멀티키나제 억제제, 병용 요법 등의 범주가 있으며, 모두 원발성 및 전이성 종양 모두를 대상으로 합니다. 이 시장에는 연구개발에 많은 투자를 계속하는 수많은 세계 제약기업들이 참가하고 있으며, 그 결과 새로운 치료법의 승인과 치료 적응의 확대가 가져오고 있습니다. Precision 종양 및 돌연변이 특이적 치료의 도입은 특정 유전자 변이에 맞는 약물이 더 높은 효능과 부작용이 적고 시장이 재구성되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 15억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 8.3% |

2024년, 티로신 키나아제 억제제 부문은 GIST 치료 시장에서 62.3%의 점유율을 차지하였고, 그 표적 작용과 입증된 임상 효과에 견인되었습니다. 맞춤형 의료가 보급됨에 따라 티로신 키나아제 억제제에 대한 수요가 급증하고 있습니다. 이러한 치료제, 특히 이마티닙은 전이성 GIST에 대한 표준 제1선택 치료제로 여겨지고 있으며, 미국 국립위생연구소(NIH)의 조사에서도 지적된 바와 같이, 그 높은 효능으로부터 계속 선호되고 있습니다.

브랜드 의약품 부문은 2034년까지 연평균 복합 성장률(CAGR) 8.1%로 성장할 전망입니다. 브랜드 치료제가 선호되는 이유는 임상적 성공이 입증되었고, FDA의 승인을 받고 있으며, 세계 치료 지침에 일관되게 통합되어 있기 때문입니다. 이러한 치료는 GIST 환자에게 흔한 KIT 및 PDGFRA와 같은 특정 유전자 변이를 표적으로 합니다. 연구개발에 대한 지속적인 투자는 약물내성을 극복하고 치료성적을 개선하기 위해 고안된 차세대 티로신 키나아제 억제제(TKI)와 병용요법의 창출을 뒷받침하고 있습니다.

미국의 위장관기질종양 치료 2024년 시장 규모는 5억 6,180만 달러로 큰 수요를 반영하고 있습니다. 이미징 및 분자 검사의 진보로 미국에서 더 많은 GIST 사례가 정확하게 검출되고 치료를 원하는 환자 수가 증가하고 있습니다. 게다가 FDA의 규제와 상환 정책은 브랜드 치료와 제네릭 치료 모두의 승인과 채용을 촉진하고 시장 기회를 더욱 확대하고 있습니다.

위장관기질종양 치료 시장의 주요 기업으로는 Bayer, Pfizer, Takeda Pharmaceuticals, F. Hoffmann-La Roche, Novartis, Sun Pharma, Shorla Oncology, Glenmark, AngioDynamics, Argon Medical Products, Natco Pharma, and Deciphera Pharma 등이 있습니다. 위장관기질종양 치료 시장에서의 지위를 강화하기 위해 기업은 몇 가지 중요한 전략에 주력하고 있습니다. 여기에는 혁신적인 치료를 시장에 투입하고 기존 제품 라인을 확대하기 위한 연구개발(R&D)에 대한 많은 투자가 포함됩니다. 많은 기업들은 차세대 티로신 키나아제 억제제와 병용 요법, 특히 내성 기전을 표적으로 하는 치료제의 개발을 선호합니다. 또한 각 회사는 연구기관 및 기타 제약기업과 전략적 제휴를 맺고 의약품 개발을 가속화하고 판매망을 넓혀 시장에서 발판을 굳히고 있습니다. 장기간의 임상시험 데이터, FDA 승인, 세계 치료 가이드라인 통합을 통해 브랜드 자금을 강화하는 것도 중요한 초점이 되고 있습니다. 마지막으로 기업은 지리적 도달 범위를 확대하고 GIST 이환율이 증가하는 신흥 시장에서 치료에 대한 접근성을 늘려 성장 가능성을 극대화하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 위장관기질종양의 유병률 증가

- 노화 및 유전적 소인

- 표적 치료에서의 돌파구

- 재발 및 내성에 대한 의식의 고조

- 업계의 잠재적 위험 및 과제

- 부작용 및 치료 저항성

- 저소득 지역에서의 제한된 접근

- 시장 기회

- 변이 특이적 치료법 및 병용 치료법의 개발

- 유전체 검사 및 맞춤형 의료 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 장래 시장 동향

- 기술적 상황

- 현재의 기술

- 신흥 기술

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 약제 유형별(2021-2034년)

- 주요 동향

- 멀티 키나아제 억제제

- 티로신 키나아제 억제제

- VEGF 억제제

제6장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 브랜드

- 제네릭 의약품

제7장 시장 추계 및 예측 : 연령별(2021-2034년)

- 주요 동향

- 성인

- 고령자

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Bayer

- Deciphera Pharmaceuticals

- F. Hoffmann-La Roche

- Glenmark

- Natco Pharma

- Novartis

- Pfizer

- Sanofi

- Shorla Oncology

- Sun Pharmaceuticals

- Takeda Pharmaceuticals

The Global Gastrointestinal Stromal Tumor Treatment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 3.2 billion by 2034.

This growth can be attributed to the increasing global prevalence of gastrointestinal cancers and heightened awareness of rare tumor types. Advancements in targeted therapies, particularly tyrosine kinase inhibitors (TKIs), are improving treatment outcomes and survival rates significantly. The rising incidence of metastatic and treatment-resistant GIST cases has further fueled demand for innovative drugs like ripretinib, avapritinib, and regorafenib, which are used to manage disease progression and enhance patient quality of life at various stages of the condition. Treatments for GIST are typically administered orally and are available through hospital pharmacies, retail pharmacies, and online platforms. These therapies include categories such as tyrosine kinase inhibitors, multikinase inhibitors, and combination treatments, all aimed at both primary and metastatic tumors. The market is populated by numerous global pharmaceutical companies that continue to invest heavily in research and development, resulting in the approval of new therapies and expanded treatment indications. The introduction of precision oncology and mutation-specific treatments is reshaping the market, with drugs tailored to specific genetic mutations demonstrating higher efficacy and fewer side effects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 8.3% |

In 2024, the tyrosine kinase inhibitors segment held a share of 62.3% in the GIST treatment market, driven by their targeted action and proven clinical effectiveness. As personalized medicine becomes more prevalent, the demand for tyrosine kinase inhibitors has surged. These drugs, particularly imatinib, are considered the standard first-line treatment for metastatic GIST and continue to be preferred due to their high efficacy, as noted by research from the National Institutes of Health (NIH).

The branded drug segment will grow at a CAGR of 8.1% through 2034. Branded therapies are favored due to their demonstrated clinical success, FDA approvals, and consistent inclusion in global treatment guidelines. These treatments target specific genetic mutations like KIT and PDGFRA, which are commonly found in GIST patients. Ongoing investments in research and development are driving the creation of next-generation tyrosine kinase inhibitors (TKIs) and combination therapies designed to overcome drug resistance and improve treatment outcomes.

United States Gastrointestinal Stromal Tumor Treatment Market was valued at USD 561.8 million in 2024, reflecting significant demand. With the advancement of diagnostic imaging and molecular testing, more GIST cases are being accurately detected in the U.S., leading to an increased number of patients seeking treatment. Additionally, supportive FDA regulations and reimbursement policies are facilitating the approval and adoption of both branded and generic treatments, further expanding market opportunities.

Major players in the Gastrointestinal Stromal Tumor Treatment Market include Bayer, Pfizer, Takeda Pharmaceuticals, F. Hoffmann-La Roche, Novartis, Sun Pharma, Shorla Oncology, Glenmark, AngioDynamics, Argon Medical Products, Natco Pharma, and Deciphera Pharma. To strengthen their position in the gastrointestinal stromal tumor treatment market, companies are focusing on several key strategies. This includes heavy investment in research and development (R&D) to bring innovative treatments to market and expand existing product lines. Many companies are prioritizing the development of next-generation tyrosine kinase inhibitors and combination therapies, particularly those targeting resistance mechanisms. Additionally, companies are enhancing their market foothold by forming strategic partnerships with research institutions and other pharmaceutical companies to accelerate drug development and broaden distribution networks. Strengthening brand equity through long-term clinical trial data, FDA approvals, and integration into global treatment guidelines is also a critical focus. Finally, companies are expanding their geographical reach and increasing access to treatments in emerging markets, where the incidence of GIST is rising, thereby maximizing growth potential.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug type trends

- 2.2.3 Type trends

- 2.2.4 Age group trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence gastrointestinal stromal tumors

- 3.2.1.2 Advancing age and genetic predisposition

- 3.2.1.3 Breakthroughs in targeted therapy

- 3.2.1.4 Growing awareness of recurrence and resistance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects and resistance to therapy

- 3.2.2.2 Limited access in low-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of mutation-specific and combination therapies

- 3.2.3.2 Expansion of genomic testing and personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multikinase inhibitors

- 5.3 Tyrosine kinase inhibitors

- 5.4 VEGF inhibitors

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Branded

- 6.3 Generics

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adults

- 7.3 Geriatric

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer

- 10.2 Deciphera Pharmaceuticals

- 10.3 F. Hoffmann-La Roche

- 10.4 Glenmark

- 10.5 Natco Pharma

- 10.6 Novartis

- 10.7 Pfizer

- 10.8 Sanofi

- 10.9 Shorla Oncology

- 10.10 Sun Pharmaceuticals

- 10.11 Takeda Pharmaceuticals