|

시장보고서

상품코드

1844317

헬리코박터 파일로리 검사 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Helicobacter Pylori Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

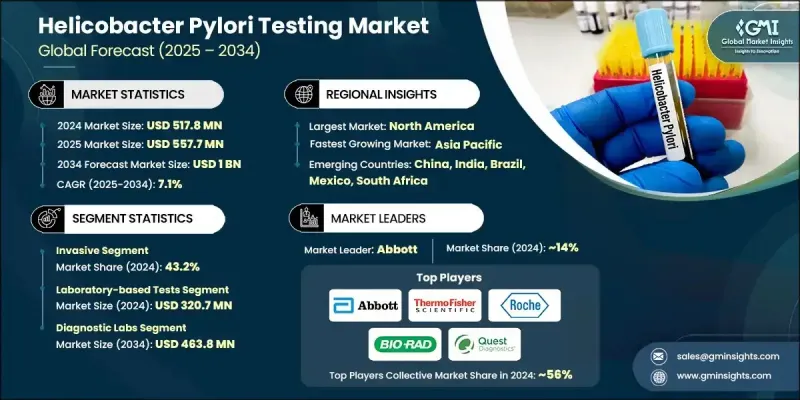

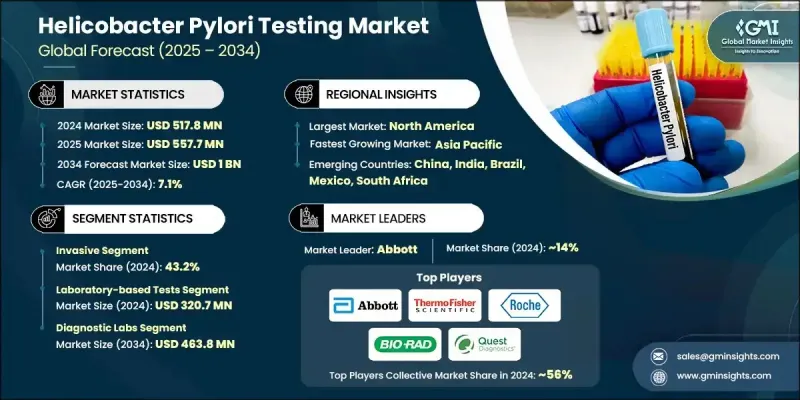

세계의 헬리코박터 파일로리 검사 시장은 2024년 5억 1,780만 달러로 평가되었고, CAGR 7.1%로 성장할 전망이며, 2034년에는 10억 달러에 이를 것으로 추정됩니다.

꾸준한 성장의 배경은 위 질환의 유병률 증가, 노인 인구 증가, 비침습적 진단 접근법에 대한 관심 증가입니다. 임상 진단에서 큰 전환이 진행 중이며 세계 헬스케어 시스템이 고급 검사 도구로 질병의 조기 발견에 주력하고 있습니다. 소화기 질환이 보편화됨에 따라 정확하고 환자 친화적인 검사에 대한 수요가 증가하고 있습니다. 동시에 조기 발견에 대한 인식과 선호도 증가는 병원과 진단센터가 헬리코박터 파일로리 검사 능력을 확대하는 데 영향을 미쳤습니다. 포인트 오브 케어 검사도 그 신속성, 편리성, 다양한 헬스케어 환경에서의 사용의 용이성으로부터 널리 지지를 모으고 있습니다. 이러한 장비는 임상의가 신속한 결과를 얻을 수 있으며 환자의 결과와 치료 기간을 향상시킬 수 있습니다. 또한 분자진단학과 AI 기반 결과 해석 및 원격검사 플랫폼을 포함한 디지털 헬스툴의 혁신은 시장 접근성을 크게 확대하여 임상 정확도를 향상시키고 있습니다. 이러한 요소들이 결합되어 헬리코박터 파일로리 검사 영역은 세계 소화기 건강 진단의 중요한 분야로 형성되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 5억 1,780만 달러 |

| 예측 금액 | 10억 달러 |

| CAGR | 7.1% |

침습적 검사 부문은 조직 생검과 현미경 분석을 통해 달성된 우수한 진단 정확도로 2024년에 43.2%의 점유율을 획득했습니다. 이러한 방법은 특히 위험이 높은 경우와 복잡한 경우에 박테리아 감염과 관련된 위장 이상에 대한 신뢰할 수 있는 발견을 제공합니다. 임상의는 정확성 및 상세한 병리학적 검사가 필요한 경우 침습적 검사에 의존하고 있으며, 종합 진단과 암 스크리닝에서 중요한 역할을 강화하고 있습니다.

실험실 기반 검사 부문은 2024년 3억 2,070만 달러를 창출했습니다. 이 분야는 제공되는 진단 정보의 높은 신뢰성과 깊이로 리드를 유지합니다. 조직학적 분석, 배양, 혈청학적 분석과 같은 실험실 검사는 박테리아 균주의 확인, 감염 단계 결정, 항생제 내성 평가에 필수적입니다. 궤양 및 만성 위염과 같은 헬리코박터 파일로리와 관련된 위장 질환 증가율은 병원과 독립적인 실험실 환경에서 정밀한 실험실 기반 진단에 대한 수요를 계속 증가시킵니다.

북미의 헬리코박터 파일로리 검사 시장은 2024년에 34.6%의 점유율을 차지했는데, 이는 이 지역의 확립된 헬스케어 인프라와 소화기 질환 부담 증가 때문입니다. 진단 실험실 존재감의 강도, 임상 의식의 고조, 조기 스크리닝의 실시가 검사 보급에 기여하고 있습니다. 이 지역은 또한 첨단 진단에 대한 지속적인 투자와 비침습적 솔루션의 이용 증가의 혜택을 누리고 있으며 미국과 캐나다의 지속적인 시장 성장을 지원합니다.

세계의 헬리코박터 파일로리 검사 시장에서 적극적으로 경쟁하는 주요 기업은 Abbott, bioMerieux, Thermo Fisher Scientific, Bio-Rad Laboratories, Meridian Biosciences, Quidel Corporation, Gulf Coast Scientific, CERTEST, Coris BioConcept, Quest Diagnostics, Roche, Cardinal Health, BIOHIT 등이 있습니다. 헬리코박터 파일로리 검사 시장의 기업은 시장에서의 존재감을 높이기 위해 다면적인 전략을 채택하고 있습니다. 선도적인 제조업체는 연구개발 투자를 선호하고 짧은 납기에 임상적 유용성이 높은 고감도 진단 키트를 개발하고 있습니다. 많은 기업들은 환자 친화적인 진단제에 대한 수요가 증가함에 따라 비침습적인 검사 포트폴리오를 확대하고 있습니다. 병원, 진단 체인 및 연구 기관과의 전략적 파트너십을 통해 기업은 판매 네트워크를 확장하고 검사 솔루션을 주류 임상 워크플로에 통합할 수 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 위궤양의 유병률 상승

- 위험에 처하는 노인 인구 증가

- 포인트 오브 케어 검사 기기 수요 증가

- 비침습성 파일로리균 검사의 도입 증가

- 업계의 잠재적 위험 및 과제

- 침습적 검사를 실시하는 숙련된 전문가의 부족

- 헬리코박터 파일로리균 감염에 관한 인식의 부족

- 시장 기회

- 분자 검사에서의 기술 혁신

- 집에서 할 수 있는 자기 검사 키트

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 현재의 기술 동향

- 비침습적 검사의 도입(우레아 호기, 변항원, 혈청학)

- 자동화 및 고처리량 진단 시스템

- 검사 정보 시스템(LIS)과의 통합

- 분석의 감도 및 특이성 향상

- 신흥 기술

- 포인트 오브 케어(POC) 휴대용 헬리코박터 파일로리 검출 키트

- 정확한 검출을 위한 분자 및 PCR 기반 분석

- 생검 및 조직학적 분석을 위한 AI와 머신러닝

- 동시병원체 검출을 위한 멀티플렉스 검사 플랫폼

- 현재의 기술 동향

- 장래 시장 동향

- 비침습성 가정용 헬리코박터 파일로리 검사 키트의 보급률

- 보다 신속하고 정확한 검출을 위한 AI 구동형 진단 툴의 확장

- 검사 모니터링을 위한 디지털 헬스 플랫폼 및 원격 의료의 통합 확대

- 시장 개척 전략

- 가격 분석

- GAP 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 검사 유형별(2021-2034년)

- 주요 동향

- 침습적

- 신속 우레아제 시험

- 조직학

- HP 문화

- 비침습적

- 혈청학적 검사

- 우레아 호기 검사

- 대변 항원 검사

제6장 시장 추계 및 예측 : 방법별(2021-2034년)

- 주요 동향

- 실험실에서의 검사

- 포인트 오브 케어(POC) 검사

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 진단 실험실

- 병원

- 클리닉

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- BIOHIT

- bioMerieux

- Bio-Rad Laboratories

- Cardinal Health

- CERTEST

- Coris BioConcept

- Gulf Coast Scientific

- Meridian Biosciences

- Quest Diagnostics

- Quidel Corporation

- Roche

- Thermo Fisher Scientific

The Global Helicobacter Pylori Testing Market was valued at USD 517.8 million in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 1 billion by 2034.

The steady growth is driven by the increasing prevalence of gastric disorders, a rise in the elderly population, and growing interest in non-invasive diagnostic approaches. A major shift is underway in clinical diagnostics, with healthcare systems across the world focusing on early disease detection through advanced testing tools. As gastrointestinal diseases become more common, the demand for accurate and patient-friendly tests is climbing. Simultaneously, rising awareness and preference for early detection are influencing hospitals and diagnostic centers to expand their H. pylori testing capabilities. Point-of-care testing is also gaining widespread traction due to its speed, convenience, and accessibility in a variety of healthcare settings. These devices enable clinicians to deliver rapid results, which enhances patient outcomes and treatment timelines. Additionally, innovations in molecular diagnostics and digital health tools including AI-based result interpretation and remote testing platforms are significantly broadening market accessibility and improving clinical precision. Combined, these elements are shaping the helicobacter pylori testing space into a key sector of gastrointestinal healthcare diagnostics worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $517.8 Million |

| Forecast Value | $1 Billion |

| CAGR | 7.1% |

The invasive testing segment captured 43.2% share in 2024, due to its superior diagnostic accuracy achieved through tissue biopsies and microscopic analysis. These methods offer reliable insights into bacterial infection and associated gastric abnormalities, particularly in high-risk or complicated cases. Clinicians continue to rely on invasive procedures when precision and detailed pathology are required, reinforcing their critical role in comprehensive diagnosis and cancer screening.

The laboratory-based tests segment generated USD 320.7 million in 2024. This segment holds its lead due to the high reliability and depth of diagnostic information provided. Laboratory tests like histological analysis, cultures, and serological assays are essential for identifying bacterial strains, determining infection stages, and assessing antibiotic resistance. Rising rates of H. pylori-associated gastrointestinal conditions such as ulcers and chronic gastritis continue to fuel the demand for precise lab-based diagnostics in both hospital and independent lab environments.

North American Helicobacter Pylori Testing Market held 34.6% share in 2024, driven by the region's well-established healthcare infrastructure and increasing gastrointestinal disease burden. Strong presence of diagnostic laboratories, growing clinical awareness, and early screening practices contribute to widespread test adoption. The region also benefits from ongoing investments in advanced diagnostics and rising uptake of non-invasive solutions, supporting sustained market growth across the US and Canada.

Key players actively competing in the Global Helicobacter Pylori Testing Market include Abbott, bioMerieux, Thermo Fisher Scientific, Bio-Rad Laboratories, Meridian Biosciences, Quidel Corporation, Gulf Coast Scientific, CERTEST, Coris BioConcept, Quest Diagnostics, Roche, Cardinal Health, and BIOHIT. Companies in the helicobacter pylori testing market are adopting multifaceted strategies to reinforce their market presence. Leading manufacturers are prioritizing R&D investments to develop high-sensitivity diagnostic kits with shorter turnaround times and broader clinical utility. Many firms are expanding their non-invasive testing portfolios to align with rising demand for patient-friendly diagnostics. Strategic partnerships with hospitals, diagnostic chains, and research institutions allow companies to widen distribution networks and integrate testing solutions into mainstream clinical workflows.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Method trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in prevalence of gastric ulcer

- 3.2.1.2 Increasing geriatric population at risk

- 3.2.1.3 Growing demand for point-of-care testing devices

- 3.2.1.4 Rising adoption of non-invasive H. pylori testing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals for invasive testing

- 3.2.2.2 Lack of awareness regarding H. pylori infection

- 3.2.3 Market opportunities

- 3.2.3.1 Technological innovations in molecular testing

- 3.2.3.2 Home-based and self-testing kits

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Non-invasive testing adoption (urea breath, stool antigen, serology)

- 3.5.1.2 Automation and high-throughput diagnostic systems

- 3.5.1.3 Integration with laboratory information systems (LIS)

- 3.5.1.4 Improved sensitivity and specificity of assays

- 3.5.2 Emerging technologies

- 3.5.2.1 Point-of-Care (POC) portable H. pylori detection kits

- 3.5.2.2 Molecular and PCR-based assays for precise detection

- 3.5.2.3 AI and machine learning for biopsy and histology analysis

- 3.5.2.4 Multiplex testing platforms for simultaneous pathogen detection

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.6.1 Increased adoption of non-invasive home-based H. pylori testing kits

- 3.6.2 Expansion of AI-driven diagnostic tools for faster and more accurate detection

- 3.6.3 Growing integration of digital health platforms and telemedicine for test monitoring

- 3.7 Go-to-market strategies

- 3.8 Pricing analysis

- 3.9 GAP analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LAMEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Invasive

- 5.2.1 Rapid urease test

- 5.2.2 Histology

- 5.2.3 HP culture

- 5.3 Non-invasive

- 5.3.1 Serologic test

- 5.3.2 Urea breath test

- 5.3.3 Stool/fecal antigen test

Chapter 6 Market Estimates and Forecast, By Method, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Laboratory based tests

- 6.3 Point of care (POC) tests

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostic labs

- 7.3 Hospitals

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 BIOHIT

- 9.3 bioMerieux

- 9.4 Bio-Rad Laboratories

- 9.5 Cardinal Health

- 9.6 CERTEST

- 9.7 Coris BioConcept

- 9.8 Gulf Coast Scientific

- 9.9 Meridian Biosciences

- 9.10 Quest Diagnostics

- 9.11 Quidel Corporation

- 9.12 Roche

- 9.13 Thermo Fisher Scientific