|

시장보고서

상품코드

1844330

피부과 치료제 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Dermatology Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

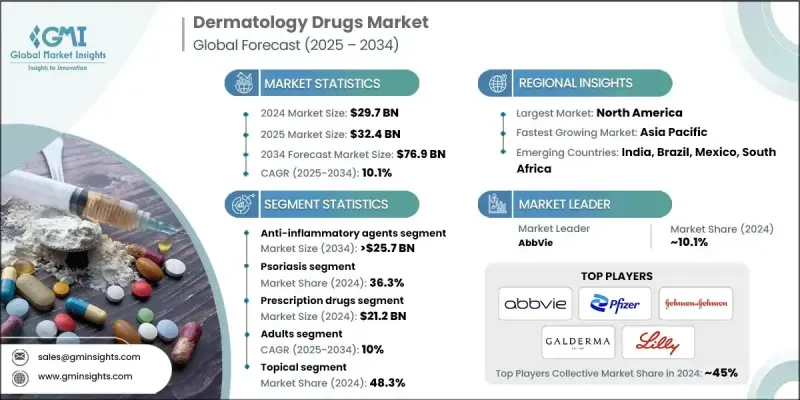

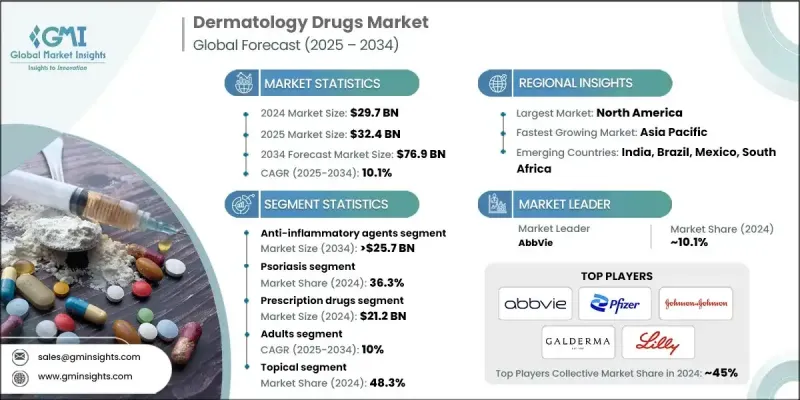

세계의 피부과 치료제 시장 규모는 2024년에는 297억 달러로 평가되었고, CAGR 10.1%로 성장할 전망이며, 2034년에는 769억 달러에 이를 것으로 추정됩니다.

이 증가 추세는 여드름, 습진, 건선과 같은 만성 및 급성 피부 질환의 유병률 증가 외에도 희귀 피부 질환에 대한 관심 증가로 인한 것입니다. 이 시장은 단일클론항체와 저분자 억제제를 포함한 표적 치료제의 기술적 진보로 더욱 효과적이고 환자 친화적인 결과를 가져오고 강력한 기세를 보이고 있습니다. 또한, 약물 내성 피부 질환에 대응하는 치료에 대한 수요도 높아지고 있으며, 증상을 억제하고 질병의 진행을 늦추도록 설계된 새로운 제제의 공간이 탄생하고 있습니다. 병원, 피부과 클리닉 및 재택 헬스케어에서 의료 접근의 확대는 특히 선진 및 신흥 지역 모두에서 약물의 채택을 뒷받침하고 있습니다. 환자 의식 증가는 맞춤형 의료에 대한 소비자 선호의 진화와 함께 성장을 형성하고 있습니다. 대형 제약 기업은 규제 당국의 승인을 확보하고 특정 염증 경로 및 면역 경로에 작용하는 치료제를 출시하기 위해 연구개발에 많은 투자를 실시했습니다. 이러한 노력은 정밀 피부과학으로의 이동과 부작용의 최소화 및 환자의 장기 복약 준수의 향상을 목표로 하는 약물 전달 플랫폼의 최적화를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 297억 달러 |

| 예측 금액 | 769억 달러 |

| CAGR | 10.1% |

항염증 요법 분야는 2024년에 32.6%의 점유율을 차지했으며, CAGR 10.4%로 성장하면서 2034년에는 257억 달러에 달할 것으로 예측됩니다. 이 이점은 코르티코스테로이드와 비 스테로이드계 약물이 광범위한 염증성 피부 질환에 높은 효능을 보이는 데 도움이 됩니다. 이러한 제형은 신속한 완화를 제공하기 때문에 급성 및 지속성 증상을 모두 관리하는 표준 접근법입니다. 아토피 피부염이나 건선 등의 피부 질환이 증가하는 길을 따라가는 가운데, 이러한 약제의 채용은 증가하고 있으며, 임상 현장에서는 대부분이 제일 선택약이 되고 있습니다.

처방약 부문은 2024년에 212억 달러를 창출했습니다. 이러한 약물의 지속적인 사용은 강력한 임상 증거, 일관된 기술 혁신 및 표적 브랜드 의약품의 개발에 지원됩니다. 이러한 치료제는 중등도 내지 중증 피부 질환, 특히 생물학적 제제, 코르티코스테로이드 및 항진균제를 이용한 장기적인 치료를 필요로 하는 피부 질환의 치료의 중심적 존재입니다. 규제 당국의 승인과 제형의 개선은 특히 환자에게 맞는 지속적인 치료가 필요한 분야에서 시장 침투를 가속화하고 있습니다.

북미의 피부과 치료제 2024년 시장 점유율은 40.4%로, 높은 인지도, 선진 의료에 대한 접근성 향상, 만성 피부 질환을 앓고 있는 환자 증가가 배경에 있습니다. 이 지역의 성장은 바이오마커 기반의 의약품 개발 및 유전자 프로파일링과 같은 개인화된 피부과 치료의 채택에도 영향을 받고 있습니다. 캐나다와 미국을 포함한 이 지역의 국가들은 유리한 상환 정책과 공중 보건 지원 프로그램에 도움을 받고 피부과에 대한 접근성을 개선하기 위해 헬스케어의 틀을 강화하고 있습니다.

세계의 피부과 치료제 산업의 전망을 형성하고 있는 주요 기업으로는 Galderma, Pfizer, Incyte, Sanofi, Eli Lilly and Company, AstraZeneca, AbbVie, GlaxoSmithKline, Leo Pharma, Bausch Health, Dermavant Sciences, Novartis, Amgen, Johnson & Johnson, F. Hoffmann La Roche, Almirall, and Merck KGaA 등이 있습니다. 선도적인 피부과 의약품 제조업체는 그 존재를 확대하기 위해 다방면에 걸친 전략을 채택하고 있습니다. 대부분은 포트폴리오를 다양화하고 진화하는 치료 요구를 충족시키기 위해 차세대 생물 제제 및 유전자 표적 치료에 투자하고 있습니다. 생명공학 및 연구기관과의 전략적 제휴는 창약과 파이프라인 개발을 가속화하는 데 도움이 됩니다. 각 회사는 또한 지리적 확장, 특히 헬스케어 인프라가 성장하고 있는 신흥 시장으로의 진출을 우선시하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 피부 질환 증가

- 인구동태의 변화 및 라이프스타일 요인

- 생물제제 및 저분자 의약품의 진보

- 피부의 건강 및 미용에 대한 의식의 고조

- 업계의 잠재적 위험 및 과제

- 부작용과 약제 내성

- 자원이 적은 환경에서 제한된 액세스

- 시장 기회

- 맞춤형 피부과 확대

- AI 및 원격 피부과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 장래 시장 동향

- 기술적 상황

- 투자 및 자금 조달의 상황

- 특허 분석

- 환급 시나리오

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 면역조절제

- 레티노이드

- 항생제

- 항염증제

- 항진균제

- 기타 약물 클래스

제6장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 건선

- 아토피 피부염

- 여드름

- 피부암

- 기타 적응증

제7장 시장 추계 및 예측 : 모드별(2021-2034년)

- 주요 동향

- 처방약

- 시판약

제8장 시장 추계 및 예측 : 연령별(2021-2034년)

- 주요 동향

- 소아

- 성인

- 고령자

제9장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 비경구

- 주제

- 경구

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 피부과 클리닉

- 재택 케어의 설정

- 기타 용도

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- AbbVie

- Almirall

- Amgen

- AstraZeneca

- Bausch Health

- Dermavant Sciences

- Eli Lilly and Company

- F. Hoffmann La Roche

- Galderma

- GlaxoSmithKline

- Incyte

- Johnson & Johnson

- Leo Pharma

- Merck KGaA

- Novartis

- Pfizer

- Sanofi

The Global Dermatology Drugs Market was valued at USD 29.7 billion in 2024 and is estimated to grow at a CAGR of 10.1% to reach USD 76.9 billion by 2034.

This upward trend is driven by the increasing prevalence of chronic and acute skin conditions such as acne, eczema, and psoriasis, along with a growing focus on rare dermatological disorders. The market is witnessing strong momentum due to technological advances in targeted therapies, including monoclonal antibodies and small molecule inhibitors, which are delivering more effective and patient-friendly outcomes. Demand is also rising for treatments addressing drug-resistant skin diseases, which is creating space for new formulations designed to control symptoms and slow disease progression. The expanding access to care across hospitals, dermatology clinics, and home-based healthcare continues to boost drug adoption, particularly in both developed and emerging regions. Rising patient awareness, coupled with evolving consumer preference for personalized medicine, is also shaping growth. Leading pharmaceutical players are investing heavily in R&D to secure regulatory approvals and launch therapies that act on specific inflammatory or immune pathways. These efforts have strengthened the shift toward precision dermatology and optimized drug delivery platforms aimed at minimizing side effects and improving long-term patient adherence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.7 Billion |

| Forecast Value | $76.9 Billion |

| CAGR | 10.1% |

The anti-inflammatory therapies segment held a 32.6% share in 2024 and is projected to reach USD 25.7 billion by 2034, growing at a CAGR of 10.4%. This dominance is supported by the high efficacy of corticosteroids and non-steroidal agents in addressing a wide range of inflammatory skin disorders. These formulations offer quick relief, making them the standard approach in managing both acute and persistent conditions. As skin disorders such as atopic dermatitis and psoriasis continue to rise, the adoption of these medications increases, with most being first-line therapies in clinical practice.

The prescription drugs segment generated USD 21.2 billion in 2024. Their continued use is supported by strong clinical evidence, consistent innovation, and the development of targeted branded drugs. These therapies are central in managing moderate to severe skin conditions, especially those that require long-term treatment using biologics, corticosteroids, and antifungals. Regulatory approvals and enhanced formulations are fueling their market penetration, particularly in segments where patients require customized, ongoing medical care.

North America Dermatology Drugs Market held a 40.4% share in 2024, driven by high awareness levels, better access to advanced medical care, and an increasing number of individuals affected by chronic skin conditions. The region's growth is also being influenced by the adoption of personalized dermatological treatments, such as biomarker-based drug development and genetic profiling. Countries across the region, including Canada and the U.S., are enhancing their healthcare frameworks to improve dermatological access, aided by favorable reimbursement policies and public health outreach programs.

Key players shaping the landscape of the Global Dermatology Drugs Industry include Galderma, Pfizer, Incyte, Sanofi, Eli Lilly and Company, AstraZeneca, AbbVie, GlaxoSmithKline, Leo Pharma, Bausch Health, Dermavant Sciences, Novartis, Amgen, Johnson & Johnson, F. Hoffmann La Roche, Almirall, and Merck KGaA. To expand their presence, leading dermatology drug manufacturers are embracing multi-pronged strategies. Many are investing in next-generation biologics and gene-targeted therapies to diversify their portfolios and meet evolving treatment needs. Strategic collaborations with biotech firms and research institutions help accelerate drug discovery and pipeline development. Companies are also prioritizing geographic expansion, particularly into emerging markets with growing healthcare infrastructure.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Indication trends

- 2.2.4 Mode trends

- 2.2.5 Age group trends

- 2.2.6 Route of administration

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic skin conditions

- 3.2.1.2 Demographic shifts and lifestyle factors

- 3.2.1.3 Advancements in biologics and small molecule drugs

- 3.2.1.4 Growing awareness of skin health and aesthetics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects and drug resistance

- 3.2.2.2 Limited access in low-resource settings

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized dermatology

- 3.2.3.2 Integration of AI and telehealth dermatology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.7 Investment and funding landscape

- 3.8 Patent analysis

- 3.9 Reimbursement scenario

- 3.10 Pipeline analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Immunomodulators

- 5.3 Retinoids

- 5.4 Antibiotics

- 5.5 Anti-inflammatory agents

- 5.6 Antifungal drugs

- 5.7 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Psoriasis

- 6.3 Atopic dermatitis

- 6.4 Acne

- 6.5 Skin cancer

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prescription drugs

- 7.3 Over the counter drugs

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Paediatric

- 8.3 Adults

- 8.4 Geriatric

Chapter 9 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Parenteral

- 9.3 Topical

- 9.4 Oral

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Dermatologist clinics

- 10.4 Homecare settings

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Almirall

- 12.3 Amgen

- 12.4 AstraZeneca

- 12.5 Bausch Health

- 12.6 Dermavant Sciences

- 12.7 Eli Lilly and Company

- 12.8 F. Hoffmann La Roche

- 12.9 Galderma

- 12.10 GlaxoSmithKline

- 12.11 Incyte

- 12.12 Johnson & Johnson

- 12.13 Leo Pharma

- 12.14 Merck KGaA

- 12.15 Novartis

- 12.16 Pfizer

- 12.17 Sanofi