|

시장보고서

상품코드

1844345

심실보조장치 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Ventricular Assist Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

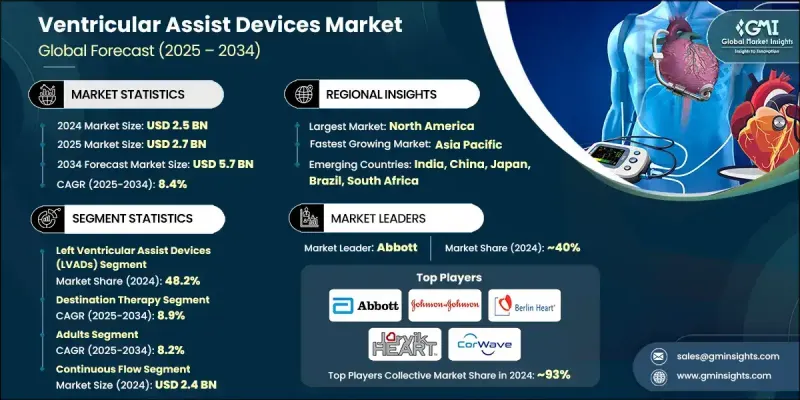

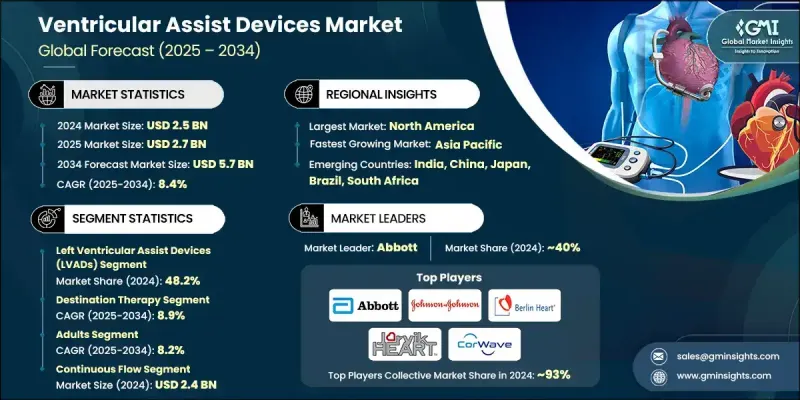

세계의 심실보조장치 시장은 2024년 25억 달러로 평가되었으며 CAGR 8.4%로 성장해 2034년까지 57억 달러에 이를 것으로 추정됩니다.

시장 성장의 원동력은 심혈관 질환과 심부전의 유병률 증가, 환자 의식 증가, 심장 기증자의 지속적인 부족입니다. 심장 이식이 제한된 상태로 남아 있기 때문에 심실보조장치는 장기적인 지원과 이식에 이르기까지 필수적인 선택입니다. 급속한 기술 진화는 임상 성능과 사용자의 안전성을 모두 향상시켜 환자 생존율을 향상시키고 세계적인 보급으로 이어지고 있습니다. 이식 가능한 기술, 재료 과학 및 디지털 건강 통합의 발전은 중요한 치료와 외래 환자 모두에서의 사용 확대를 지원합니다. 소형화된 생체적합성이 높은 컴포넌트는 무선 모니터링 및 원격 진단과 같은 스마트한 기능과 결합하여 심실보조장치를 침습적인 기계적 지원에서 지능형 심장 관리 시스템으로 이동시키는 데 도움이 됩니다. 신흥국 시장과 개척시장 모두가 심장치료 능력을 확대함에 따라 심실보조장치는 특히 내과적 치료만으로는 불충분한 경우의 종합적 심부전 치료에 있어서 점점 중요한 역할을 하게 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 25억 달러 |

| 예측 금액 | 57억 달러 |

| CAGR | 8.4% |

우심실보조장치(RVADs) 부문은 2034년까지 연평균 복합 성장률(CAGR) 9.4%로 성장할 것으로 예상됩니다. RVAD 수요 증가는 우심 합병증을 가진 환자 증가와 첨단 심장 치료에서 특별한 심실 지원의 필요성과 밀접하게 관련되어 있습니다. 컴팩트한 장치 아키텍처와 거부 반응의 위험을 줄이는 소재의 지속적인 개선으로 RVAD는 목표를 좁힌 개입이 필요한 복잡한 심장 수술에서 점점 더 선호되고 있습니다. 이러한 장치는 현재 이식에 대한 교량 치료 및 단기 회복 용도에 적합하며 여러 관리 경로의 관련성이 향상되었습니다.

2024년 병원 부문의 점유율은 43.1%로 2034년까지 24억 달러에 이를 것으로 예측됩니다. 병원은 여전히 심실보조장치 환자의 수술 이식, 실시간 모니터링, 수술 후 관리의 진원지입니다. 고도의 개입을 필요로 하는 심각한 심부전 환자의 부담이 증가하고 있는 것은 병원 환경에서 장비 설치에 대한 수요를 부추기고 있습니다. 또한 전문 심장병 유닛과 훈련된 인원은 장비 배치의 효율성과 안전성을 높이고 병원 시장 지배적 지위를 강화하고 있습니다. 현대 인프라가 존재하고 혁신적인 도구에 대한 접근이 확대됨에 따라 병원 시스템은 심실보조장치 프로그램의 장기적인 성공에 필수적인 중요한 기여자로 자리매김하고 있습니다.

2024년 미국 심실보조장치 시장 규모는 13억 달러였습니다. 고급 의료시설, 훈련된 심장혈관 외과 의사의 대규모 기반, 최신 수술 기술에 대한 접근이 VAD 도입의 주요 촉진 요인이 되었습니다. 이 나라는 수술 건수, 기술 혁신의 도입, 이식 후 케어에 있어서 리드를 계속하고 있습니다. 확고한 상환의 틀과 환자의 강한 의식으로 미국은 VAD 솔루션을 확대하는 기업에게 유리한 환경을 제공합니다.

세계 심실보조장치 시장에서 유력한 기업으로는 CorWave, Berlin Heart, Abbott, BrioHealth, Jarvik HEART, EVAHEART, Johnson & Johnson 등이 있습니다. 심실보조장치 시장의 주요 기업은 소형화, 무선 접속성, 생체적합성을 중시한 차세대 기술을 개발해 혁신 주도의 성장에 중점을 두고 있습니다. 대부분은 스마트 소재와 플로우 알고리즘을 통해 장비 수명을 연장하고 합병증의 위험을 줄입니다. 보다 광범위한 환자층을 수용하기 위해 기업은 침습성이 낮은 이식 기술과 완전히 이식 가능한 시스템에 투자하고 있습니다. 병원 및 연구센터와의 전략적 파트너십은 임상시험을 추진하고 규제 당국의 승인을 가속화하는 데 도움이 됩니다. 또한 판매 제휴 및 수술 팀을 위한 교육 프로그램을 통해 신흥 헬스케어 시장에 진출하여 지리적 확대를 도모하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심부전 및 심혈관 질환 증가

- 기술적 진보

- 심부전 치료에 관한 의식 고조

- 심장 기증자의 부족

- 업계의 잠재적 위험 및 과제

- 장치의 높은 비용

- 수술의 위험과 합병증

- 시장 기회

- 신흥 시장에서의 도입

- 환자 친화적인 솔루션에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 상황

- 현재의 기술

- 신흥기술

- 미래 시장 동향

- 환급 시나리오

- 세계의 심장 이식 시나리오

- 역학의 정세

- 파이프라인 분석

- 투자 상황

- 가격 분석, 2024년

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 좌심실 보조장치(LVAD)

- 우심실 보조장치(RVAD)

- 양심실 보조 장치(BIVAD)

- 경피적 심실보조장치

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 목적치 테라피

- Bridge-to-candidacy(BTC) 요법

- Bridge-to-transplant(BTT) 요법

- Bridge-to-recovery(BTR) 요법

- 기타 용도

제7장 시장 추계 및 예측 : 환자별, 2021-2034년

- 주요 동향

- 성인

- 소아

제8장 시장 추계 및 예측 : 플로우별, 2021-2034년

- 주요 동향

- 박동 플로우

- 연속 플로우

- 축방향 연속 플로우

- 원심 연속 플로우

제9장 시장 추계 및 예측 : 디자인별, 2021-2034년

- 주요 동향

- 경피

- 임플란트

제10장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 심장 카테터 검사실

- 외래수술센터(ASC)

- 기타 용도

제11장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Abbott

- Berlin Heart

- BrioHealth

- CorWave

- EVAHEART

- Jarvik HEART

- Johnson & Johnson

The Global Ventricular Assist Devices Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 5.7 billion by 2034.

Market growth is driven by the increasing prevalence of cardiovascular disorders and heart failure, coupled with growing patient awareness and the persistent shortage of heart donors. With heart transplants remaining limited, VADs have become an essential alternative for long-term support and bridge-to-transplant cases. Rapid technological evolution has enhanced both clinical performance and user safety, leading to better patient survival rates and wider global adoption. Advancements in implantable technologies, material science, and digital health integration are supporting expanded use in both critical care and outpatient settings. Miniaturized and biocompatible components, combined with smart functionalities such as wireless monitoring and remote diagnostics, are helping shift VADs from invasive mechanical supports to intelligent cardiac care systems. As both emerging and developed markets expand their cardiac care capabilities, VADs are playing an increasingly important role in comprehensive heart failure treatment, especially in cases where medical therapy alone falls short.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 8.4% |

The right ventricular assist devices (RVADs) segment will grow at a CAGR of 9.4% through 2034. Their rising demand is closely tied to the growing number of patients with right-sided heart complications and the need for specialized ventricular support in advanced cardiac therapies. With continuous enhancements in compact device architecture and materials that reduce rejection risks, RVADs are increasingly favored in complex cardiac procedures requiring targeted intervention. These devices are now more suitable for bridge-to-transplant procedures and short-term recovery applications, strengthening their relevance across multiple care pathways.

In 2024, the hospitals segment held a 43.1% share and is projected to reach USD 2.4 billion by 2034. Hospitals remain the epicenter of surgical implantation, real-time monitoring, and postoperative care for VAD patients. The increasing burden of severe heart failure cases requiring advanced intervention is fueling demand for device installation in hospital environments. Additionally, specialized cardiac units and trained personnel enhance the efficiency and safety of device deployment, reinforcing hospitals' dominant market position. The presence of modern infrastructure and growing access to innovative tools are positioning hospital systems as critical contributors to the long-term success of VAD programs.

United States Ventricular Assist Devices Market was valued at USD 1.3 billion in 2024, owing to its well-established cardiac care ecosystem. Advanced medical facilities, a large base of trained cardiovascular surgeons, and access to the latest surgical innovations are major enablers for VAD adoption. The nation continues to lead in surgical volumes, innovation uptake, and post-implantation care. With its robust reimbursement frameworks and strong patient awareness, the U.S. offers a favorable environment for companies expanding VAD solutions.

Prominent players in the Global Ventricular Assist Devices Market include CorWave, Berlin Heart, Abbott, BrioHealth, Jarvik HEART, EVAHEART, and Johnson & Johnson. Leading companies in the ventricular assist devices market are focusing heavily on innovation-driven growth by developing next-gen technologies that emphasize miniaturization, wireless connectivity, and biocompatibility. Many are enhancing device lifespans and lowering complication risks through smart materials and flow algorithms. To reach wider patient populations, firms are investing in less-invasive implantation techniques and fully implantable systems. Strategic partnerships with hospitals and research centers help drive clinical trials and accelerate regulatory approvals. Additionally, players are expanding geographically by entering emerging healthcare markets through distribution alliances and training programs for surgical teams.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Patient trends

- 2.2.5 Flow trends

- 2.2.6 Design trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in the number of heart failures and cardiovascular diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rise in awareness regarding heart failure treatment

- 3.2.1.4 Shortage of heart donors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Surgical risks and complications

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in emerging markets

- 3.2.3.2 Growing demand for patient-friendly solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.8 Global heart transplantation scenario

- 3.9 Epidemiology landscape

- 3.10 Pipeline analysis

- 3.11 Investment landscape

- 3.12 Pricing analysis, 2024

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Left ventricular assist devices (LVADs)

- 5.3 Right ventricular assist devices (RVADs)

- 5.4 Biventricular assist devices (BIVADs)

- 5.5 Percutaneous ventricular assist devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Destination therapy

- 6.3 Bridge-to-candidacy (BTC) therapy

- 6.4 Bridge-to-transplant (BTT) therapy

- 6.5 Bridge-to-recovery (BTR) therapy

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adults

- 7.3 Pediatrics

Chapter 8 Market Estimates and Forecast, By Flow, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pulsatile flow

- 8.3 Continuous flow

- 8.3.1 Axial continuous flow

- 8.3.2 Centrifugal continuous flow

Chapter 9 Market Estimates and Forecast, By Design, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Transcutaneous

- 9.3 Implantable

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Cardiac catheterization labs

- 10.4 Ambulatory surgical centers

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Abbott

- 12.2 Berlin Heart

- 12.3 BrioHealth

- 12.4 CorWave

- 12.5 EVAHEART

- 12.6 Jarvik HEART

- 12.7 Johnson & Johnson