|

시장보고서

상품코드

1844367

백선 치료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Ringworm Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

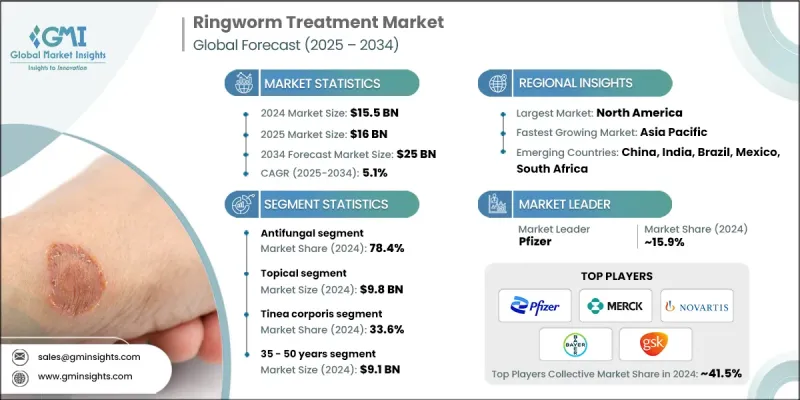

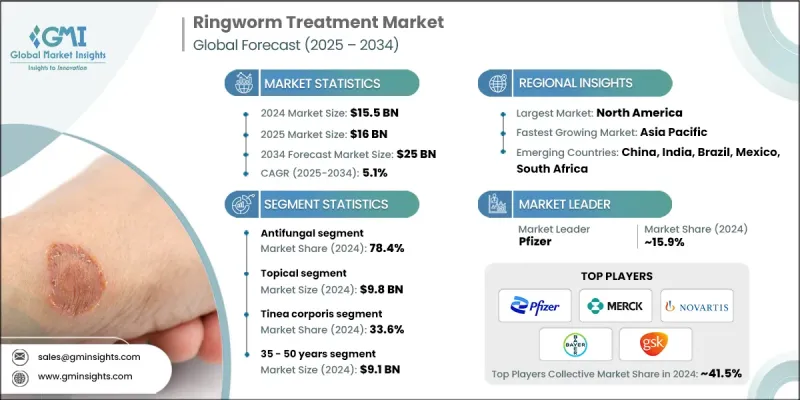

세계의 백선 치료 시장은 2024년 155억 달러로 평가되었으며 CAGR 5.1%로 성장해 2034년까지 250억 달러에 이를 것으로 추정됩니다.

선진국과 신흥국 모두에서 피부사상균증과 같은 표재성 진균 감염의 유병률이 증가하고 있는 것은 효과적인 치료 옵션에 대한 수요를 크게 촉진하고 있습니다. 이 성장의 주요 요인은 시판약(OTC)의 채용이 증가하고 소비자에게 치료가 더 친숙해졌다는 것입니다. 이러한 제형은 소매 약국 및 디지털 플랫폼에서 사용할 수 있기 때문에 특히 경증에서 중등도 감염의 셀프 케어에 자주 사용됩니다. 도시화와 헬스케어에 대한 접근성의 향상도 치료의 신속한 보급에 한몫하고 있습니다. 조직화된 소매 약국과 온라인 약국의 확대가 시장 기세를 더욱 가속화하고 있습니다. 소비자는 편의성, 프라이버시 및 저렴한 솔루션을 강력하게 선호하는 경향이 있으며, 제약 회사는 전자상거래 채널의 존재감을 높이고 있습니다. 이 전환은 또한 번들 치료 키트의 도입과 소비자에게 직접 판매 전략을 뒷받침합니다. 감염은 보통 팔, 다리, 두피에 나타나며 중증도에 따라 외용제 또는 경구 항진균 요법이 필요합니다. 제형 기술의 진보와 광범위한 유통망은 백선 치료가 더 효과적이며 모든 층에서 사용하기 쉽습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 155억 달러 |

| 예측 금액 | 250억 달러 |

| CAGR | 5.1% |

2024년 항진균제 부문은 78.4%의 점유율을 차지했으며 다양한 유형의 피부사상균증의 최전선 치료제로 널리 사용되고 있음을 반영합니다. 미코나졸, 클로트리마졸, 테르비나핀, 케토코나졸 등의 활성 성분을 함유한 제품은 진균의 증식을 멈추고 증상을 신속하게 완화하는 능력이 증명되어 널리 이용되고 있습니다. 이러한 항진균제는 합리적인 가격, 광범위한 효능 및 여러 복용 형태가 있다는 것이 치료 이점의 이유가 되었습니다. 이러한 항진균제는 종종 체부백선, 족부백선, 두부백선, 사타구니 백선, 손톱백선과 같은 일반적인 증상에 대해 처방되거나 자가 투여되는 경우가 많습니다.

국소 치료제 부문은 2024년 63%의 점유율을 차지했으며 98억 달러를 창출했습니다. 이 분야의 주도적 지위는 OTC 외용 제품이 선호되는 선택인 자기 치료 추세 증가로 인한 것입니다. 이러한 제품은 특히 합병증이 없는 감염의 경우 실제 상점과 온라인 약국에서 쉽게 구할 수 있습니다. 제약회사는 폼제, 스프레이제, 크림제, 파우더제, 젤제, 약용 티슈 등 보다 사용하기 쉬운 새로운 외용제 출시에 점점 힘을 쏟고 있습니다. 이러한 기술 혁신은 조기 개입에 대한 의식이 높아짐에 따라 국소용 항진균제의 세계 수요를 크게 견인하고 있습니다.

2024년 북미 백선 치료 시장 점유율은 40.3%였습니다. 이는 의료 인프라가 확립되어 주요 제약 기업이 존재하기 때문입니다. 의료용 의약품과 일반용 의약품 모두에 대한 액세스가 널리 보급되고 있는 것 외에도, 셀프 케어에 대한 의식 증가와 동향이 이 지역의 우위성을 지원하고 있습니다. 이 시장의 소비자는 신뢰할 수 있는 치료 옵션에 대한 편리한 액세스를 활용하고 집에서 솔루션을 선택하는 경향이 커지고 있습니다. 소매 약국과 전자상거래 플랫폼은 이 지역의 제품 가용성과 소비자 행동에 강한 영향을 미치고 있습니다.

세계 백선 치료 시장에서 사업을 전개하는 주요 기업으로는 Johnson and Johnson, Mankind Pharma, Sun Pharmaceuticals, AbbVie, Pfizer, Sanofi, Novartis, Glenmark Pharmaceuticals, Cipla, Biofield Pharma, Gilead Sciences, Teva Pharmaceutical Industries, Bayer, Merck, Perrigo Company, GlaxoSmithKline, Eli Lilly and Company 등이 있습니다. 경쟁력을 유지하기 위해 백선 치료 분야의 기업은 전자상거래 및 조직 소매 약국을 포함한 다중 채널 유통에 주력하여 제품에 대한 접근성을 높이고 있습니다. 많은 기업들은 사용자의 컴플라이언스와 효율성을 높이는 신규 외용 제형 개발에 투자하고 있습니다. 디지털 건강 플랫폼 및 약국 체인과의 전략적 파트너십은 더욱 광범위한 홍보를 가능하게 하는 반면 마케팅 이니셔티브는 곰팡이 감염과 조기 개입에 관한 계발 캠페인을 목표로 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 백선 감염의 만연

- 시판 항진균제를 간단하게 입수할 수 있음

- 백선 감염과 그 증상에 관한 의식 향상

- 업계의 잠재적 위험 및 과제

- 일반적인 항진균제에 대한 약제 내성 증가

- 환자의 치료 준수 부족

- 시장 기회

- 신규 의약품 제제의 개발

- 복합약 채용 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 백선 감염의 역학 분석

- 파이프라인 분석

- 미래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 약제 클래스별, 2021-2034년

- 주요 동향

- 항진균제

- 복합약

제6장 시장 추계 및 예측 : 투여 경로별, 2021-2034년

- 주요 동향

- 국부

- 경구

- 비경구

제7장 시장 추계 및 예측 : 감염종별, 2021-2034년

- 주요 동향

- 체부백선

- 족부백선

- 사타구니 백선

- 두부백선

- 손백선

- 기타 유형

제8장 시장 추계 및 예측 : 연령별, 2021-2034년

- 주요 동향

- 18세 미만

- 18-35세

- 35-50세

- 50세 이상

제9장 시장 추계 및 예측 : 약 유형별, 2021-2034년

- 주요 동향

- 처방전

- 시판약

제10장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제11장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- AbbVie

- Biofield Pharma

- Bayer

- Cipla

- Eli Lilly and Company

- Gilead Sciences

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Johnson and Johnson

- Mankind Pharma

- Merck

- Novartis

- Perrigo Company

- Pfizer

- Sanofi

- Sun Pharmaceuticals

- Teva Pharmaceutical Industries

The Global Ringworm Treatment Market was valued at USD 15.5 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 25 billion by 2034.

The increasing prevalence of superficial fungal infections like dermatophytosis across both developed and emerging nations is significantly driving the demand for effective treatment options. A key contributor to this growth is the rising adoption of over-the-counter (OTC) medications, making treatments more accessible for consumers. These formulations are commonly used in self-care routines, especially for mild to moderate infections, thanks to their availability across retail pharmacies and digital platforms. Urbanization and better healthcare access have also played a role, encouraging faster treatment adoption. The growing expansion of organized retail and online pharmacies is further fueling market momentum. Consumers are showing a strong preference for convenience, privacy, and affordable solutions, prompting pharmaceutical companies to enhance their presence in e-commerce channels. This shift also supports the introduction of bundled treatment kits and direct-to-consumer engagement strategies. Infections typically appear on the arms, legs, or scalp, and depending on severity, require either topical application or oral antifungal therapies. Advancements in formulation technology and broader distribution networks have made ringworm treatments more effective and accessible across all demographics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $25 Billion |

| CAGR | 5.1% |

In 2024, the antifungal drugs segment accounted for 78.4% share, reflecting their widespread usage as the frontline treatment for various types of dermatophytosis. Products containing active ingredients like miconazole, clotrimazole, terbinafine, and ketoconazole are widely utilized due to their proven ability to stop fungal growth and relieve symptoms quickly. Their affordability, broad-spectrum efficacy, and availability in multiple formats contribute to their dominance in the treatment landscape. These antifungals are frequently prescribed or self-administered for common conditions like tinea corporis, tinea pedis, tinea capitis, tinea cruris, and tinea unguium.

The topical treatments segment held a 63% share and generated USD 9.8 billion in 2024. Their leadership position stems from the growing trend of self-treatment, which has made OTC topical products a preferred option. These are easily accessible via both physical and online pharmacies, especially for uncomplicated infections. Pharmaceutical companies are increasingly focused on launching new and more user-friendly topical formulations like foams, sprays, creams, powders, gels, and medicated wipes. This innovation, coupled with increased awareness around early intervention, is significantly driving global demand for topical antifungals.

North America Ringworm Treatment Market held 40.3% share in 2024, due to its well-established healthcare infrastructure and the presence of leading pharmaceutical companies. Widespread access to both prescription and OTC medications, coupled with growing awareness and self-care trends, supports the region's dominance. Consumers in this market increasingly opt for at-home solutions, leveraging convenient access to trusted treatment options. Retail drugstores and e-commerce platforms continue to make a strong impact on product availability and consumer behavior in this region.

Key companies operating in the Global Ringworm Treatment Market include Johnson and Johnson, Mankind Pharma, Sun Pharmaceuticals, AbbVie, Pfizer, Sanofi, Novartis, Glenmark Pharmaceuticals, Cipla, Biofield Pharma, Gilead Sciences, Teva Pharmaceutical Industries, Bayer, Merck, Perrigo Company, GlaxoSmithKline, and Eli Lilly and Company. To maintain a competitive edge, companies in the ringworm treatment space are focusing on multi-channel distribution, including e-commerce and organized retail pharmacies, to increase product accessibility. Many are investing in the development of novel topical formulations that enhance user compliance and effectiveness. Strategic partnerships with digital health platforms and pharmacy chains allow for broader outreach, while marketing initiatives target awareness campaigns around fungal infections and early intervention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Route of administration trends

- 2.2.4 Infection type trends

- 2.2.5 Age group trends

- 2.2.6 Medication type trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of ringworm infections

- 3.2.1.2 Easy availability of over-the-counter antifungal medications

- 3.2.1.3 Increased awareness about ringworm infections and their symptoms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing drug resistance to common antifungal medications

- 3.2.2.2 Lack of patient compliance with treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Development of novel drug formulations

- 3.2.3.2 Rising adoption of combination drugs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Epidemiology analysis of ringworm infection

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antifungal

- 5.3 Combination drugs

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Parenteral

Chapter 7 Market Estimates and Forecast, By Infection Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Tinea corporis

- 7.3 Tinea pedis

- 7.4 Tinea cruris

- 7.5 Tinea capitis

- 7.6 Tinea manuum

- 7.7 Other types

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 18 years

- 8.3 18 - 35 years

- 8.4 35 - 50 years

- 8.5 50 years and above

Chapter 9 Market Estimates and Forecast, By Medication Type, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Prescription

- 9.3 OTC

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacies

- 10.3 Retail pharmacies

- 10.4 Online pharmacies

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Biofield Pharma

- 12.3 Bayer

- 12.4 Cipla

- 12.5 Eli Lilly and Company

- 12.6 Gilead Sciences

- 12.7 GlaxoSmithKline

- 12.8 Glenmark Pharmaceuticals

- 12.9 Johnson and Johnson

- 12.10 Mankind Pharma

- 12.11 Merck

- 12.12 Novartis

- 12.13 Perrigo Company

- 12.14 Pfizer

- 12.15 Sanofi

- 12.16 Sun Pharmaceuticals

- 12.17 Teva Pharmaceutical Industries