|

시장보고서

상품코드

1844369

재생 송풍기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Regenerative Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

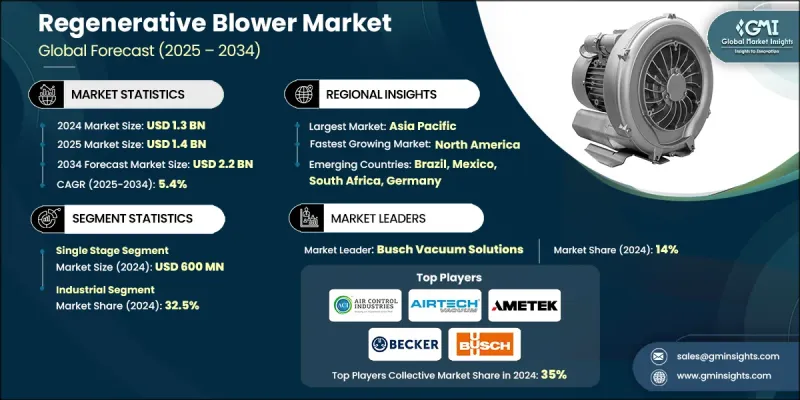

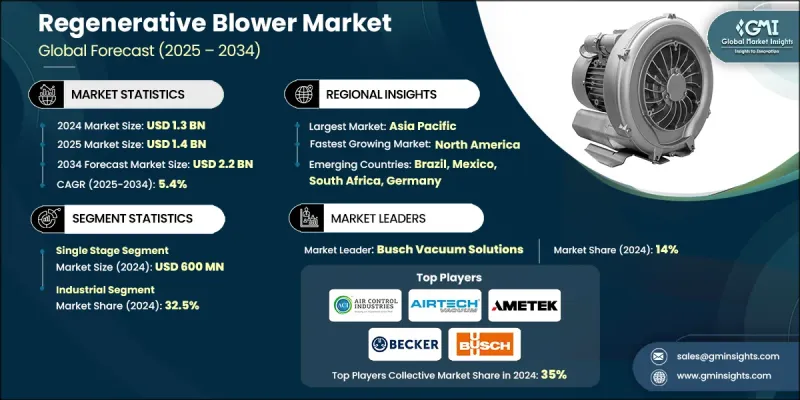

세계의 재생 송풍기 시장 규모는 2024년까지 13억 달러에 달하고, CAGR 5.4%로 성장하여 2034년까지 22억 달러에 이를 것으로 예측됩니다.

수요 증가의 주요 요인은 자동화의 급속한 발전과 다양한 분야에서 자동화 시스템의 광범위한 도입입니다. 재생 송풍기는 냉각, 자재관리, 건조, 공기 운송 등의 중요한 기능을 지원하는 역할을 하기 때문에 이러한 환경에서 중요한 구성 요소가 되고 있습니다. 오일 프리, 안정적인 공기 흐름과 낮은 유지 보수 필요성으로 고성능 산업 환경에서 높은 지지를 얻고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 13억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 5.4% |

재생 송풍기 설계 및 엔지니어링의 지속적인 혁신으로 효율성, 성능 및 다용도가 크게 향상되었습니다. 강화된 재료와 지능형 제어 시스템은 기존 분야와 신흥 분야 모두에서 응용 분야를 확대하고 있습니다. 청정 에너지 시스템, 부가제조, 고도의 공압 핸들링 등 새로운 분야에서의 응용이 채용을 더욱 촉진하고 있습니다. 이러한 시나리오에서 재생 송풍기는 정확한 공기 이동, 에너지 절약, 오염 없는 운전을 실현하여 최신 제조업 및 환경 중시 산업에 이상적입니다. 재생식 송풍기의 가치 제안은 운전 효율뿐만 아니라 지속 가능한 생산과 운전 위험의 감소에도 있습니다.

1단계 부문은 중공업 용도와 경공업 용도 모두에서 널리 사용되기 때문에 2024년에는 6억 달러를 차지하고 있습니다. 이 송풍기는 안정적인 기류가 필요한 시스템에 필수적이며 화학물질 교반, 연소 가스 공급, 분진 제거, 흡입 용도, 에어 나이프 블로우오프 등의 작업을 지원합니다. 이러한 송풍기가 널리 사용되는 이유는 최소한의 복잡성으로 높은 신뢰성을 제공할 수 있기 때문에 가동 시간을 지원하고 운영 비용을 절감할 수 있습니다.

산업 용도 부문은 2024년 32.5%의 점유율을 차지했고 중공업에서 재생식 송풍기의 중요성을 부각하고 있습니다. 이 시스템은 높은 유량과 압력 안정성이 모두 요구되는 운전을 위해 조정됩니다. 폐수 관리, 공기 수송, 폭기 등의 분야에서 일반적으로 사용되는 이러한 송풍기는 오일 프리 운전을 유지하면서 효율적인 성능을 발휘합니다.

2024년 미국 재생 송풍기 국내 산업이 자동화와 에너지 효율적인 솔루션을 채택했기 때문에 시장 점유율은 76%에 달했습니다. 배출 가스, 직장 안전, 장비 소음 수준에 대한 규제 모니터링이 강화되어 조용하고 스마트한 송풍기 기술로의 전환이 촉진됩니다. 미국 제조업체는 효율성 향상, 디지털 통합 및 고급 가변 속도 기능을 갖춘 송풍기를 제공함으로써 이 수요에 대응하고 있습니다. 이러한 개발은 스마트 제조 및 산업 공정 제어에서 고정밀 공기 흐름 시스템에 대한 요구 증가와 일치합니다.

세계 재생 송풍기 시장의 주요 기업은 Airtech Vacuum Incorporated, Goorui, The Spencer Turbine Company, FPZ SpA, Hitachi Ltd., Eurus Blowers, Becker Pump Corporation, Gardner Denver Holdings, Inc., Air Control Industries Ltd., Busch SE / Busch Vacuum Solutions, Gast Manufacturing, Inc., Atlantic Blowers, Rietschle Thomas, Ametek Inc., KNB Corporation 등이 있습니다. 재생 송풍기 시장에서 경쟁하는 기업은 세계 시장에서의 존재감을 확고하게 하기 위해 기술 혁신, 커스터마이즈, 에너지 효율에 주력하고 있습니다. 많은 사람들이 IoT 기능, 원격 진단, 고급 제어 시스템을 통합하는 스마트 송풍기 기술에 투자하고 있습니다. 전략적 파트너십과 인수는 제조업체가 공급망의 탄력성을 높이면서 제품 포트폴리오를 확대하는 데 도움이 됩니다. 각 회사는 또한 청정 에너지 및 자동화 주도의 적용에 적합한 소음이 적고 오일프리 송풍기를 개발하기 위한 연구 개발에도 힘을 쏟고 있습니다. 지역 고유의 요구에 대응하기 위해, 생산 시설의 현지화나, 요구에 맞춘 서비스의 제공이 행해지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업 자동화 수요 증가

- 에너지 효율을 촉진하는 환경 규제

- 폐수 처리 및 공조 용도의 확대

- 업계의 잠재적 위험 및 과제

- 제조 및 유지 보수 비용이 높은 비용 압력

- 대체 솔루션에 의한 기술적 대체

- 기회

- 스마트 감시 시스템과의 통합

- 신흥 시장과 인프라 개발

- 성장 촉진요인

- 성장 가능성 분석

- 미래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 단계 유형별, 2021-2034년

- 주요 동향

- 1단계

- 2단계

- 3단계

제6장 시장 추계 및 예측 : 압력 범위별, 2021-2034년

- 주요 동향

- 저압(최대 1bar)

- 중압(1-2bar)

- 고압(2bar 이상)

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 물 및 폐수

- 식음료

- 산업

- 화학약품

- 석유 및 가스

- 의학

제8장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 직접판매

- 간접판매

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제10장 기업 프로파일

- Air Control Industries Ltd.

- Airtech Vacuum Incorporated

- Atlantic Blowers

- Ametek Inc.

- Becker Pump Corporation

- Busch SE/Busch Vacuum Solutions

- Eurus Blowers

- FPZ SpA

- Gardner Denver Holdings, Inc.

- Gast Manufacturing, Inc.

- Goorui

- Hitachi Ltd.

- KNB Corporation

- Rietschle Thomas

- The Spencer Turbine Company

The Global Regenerative Blower Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 2.2 billion by 2034.

Rising demand is largely fueled by the rapid advancement of automation and the widespread implementation of automated systems across diverse sectors. Regenerative blowers have become a key component in these environments due to their role in supporting essential functions like cooling, material handling, drying, and pneumatic conveying. Their oil-free, consistent airflow and low maintenance needs make them highly favored in high-performance industrial settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.4% |

Continued innovation in regenerative blower design and engineering has significantly improved efficiency, performance, and versatility. Enhanced materials and intelligent control systems have expanded their use across both established and emerging sectors. Applications in newer fields such as clean energy systems, additive manufacturing, and advanced pneumatic handling are further driving adoption. In these scenarios, regenerative blowers provide precise air movement, energy savings, and contamination-free operation, making them ideal for modern manufacturing and environmentally focused industries. Their value proposition lies not only in operational efficiency but also in contributing to sustainable production and lower operational risks.

The single-stage segment accounted for USD 600 million in 2024 owing to its extensive use in both heavy-duty and light industrial applications. These blowers are essential in systems where consistent airflow is required, supporting tasks like chemical agitation, combustion air delivery, dust removal, suction applications, and air knife blow-offs. Their widespread use is attributed to their ability to deliver high reliability with minimal complexity, which supports uptime and lowers operational costs.

The industrial application segment held a 32.5% share in 2024, highlighting the importance of regenerative blowers in heavy industries. These systems are tailored for operations that demand both high flow rates and pressure stability. Commonly used in sectors such as wastewater management, pneumatic transport, and aeration, these blowers provide efficient performance while maintaining oil-free operation, which is critical for environments where product or process contamination must be avoided.

United States Regenerative Blower Market held a 76% share in 2024 as domestic industries embraced automation and energy-efficient solutions. Increased regulatory scrutiny around emissions, workplace safety, and equipment noise levels has encouraged the shift toward quieter, smarter blower technologies. U.S. manufacturers are addressing this demand by delivering blowers with enhanced efficiency, digital integration, and advanced variable speed capabilities. These developments align with the growing need for precision airflow systems in smart manufacturing and industrial process control.

Key players in the Global Regenerative Blower Market include Airtech Vacuum Incorporated, Goorui, The Spencer Turbine Company, FPZ SpA, Hitachi Ltd., Eurus Blowers, Becker Pump Corporation, Gardner Denver Holdings, Inc., Air Control Industries Ltd., Busch SE / Busch Vacuum Solutions, Gast Manufacturing, Inc., Atlantic Blowers, Rietschle Thomas, Ametek Inc., and KNB Corporation. Companies competing in the Regenerative Blower Market are focusing on innovation, customization, and energy efficiency to solidify their presence across global markets. Many are investing in smart blower technologies that integrate IoT features, remote diagnostics, and advanced control systems. Strategic partnerships and acquisitions are helping manufacturers expand product portfolios while improving supply chain resilience. Firms are also emphasizing R&D to develop noise-reduced, oil-free blowers suitable for clean energy and automation-driven applications. Localization of production facilities and tailored service offerings are being used to address region-specific needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type trends

- 2.2.3 Method trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for industrial automation

- 3.2.1.2 Environmental regulations promoting energy efficiency

- 3.2.1.3 Expansion of wastewater treatment and air handling applications

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Cost pressure due to high manufacturing and maintenance

- 3.2.2.2 Technological displacement by alternative solutions

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart monitoring systems

- 3.2.3.2 Emerging markets and infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Stage Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Single staged

- 5.3 Two-staged

- 5.4 Three-staged

Chapter 6 Market Estimates and Forecast, By Pressure Range, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low pressure (up to 1 bar)

- 6.3 Medium pressure (1 to 2 bar)

- 6.4 High pressure (more than 2 bar)

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Water and wastewater

- 7.3 Food & beverage

- 7.4 Industrial

- 7.5 Chemical

- 7.6 Oil & gas

- 7.7 Medical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Air Control Industries Ltd.

- 10.2 Airtech Vacuum Incorporated

- 10.3 Atlantic Blowers

- 10.4 Ametek Inc.

- 10.5 Becker Pump Corporation

- 10.6 Busch SE / Busch Vacuum Solutions

- 10.7 Eurus Blowers

- 10.8 FPZ SpA

- 10.9 Gardner Denver Holdings, Inc.

- 10.10 Gast Manufacturing, Inc.

- 10.11 Goorui

- 10.12 Hitachi Ltd.

- 10.13 KNB Corporation

- 10.14 Rietschle Thomas

- 10.15 The Spencer Turbine Company