|

시장보고서

상품코드

1844385

소비자 직접 의뢰(DTC) 유전자 검사 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Direct-to-Consumer Genetic Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

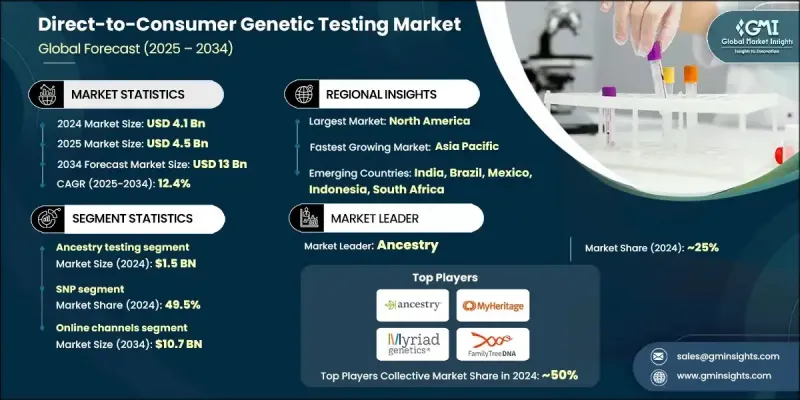

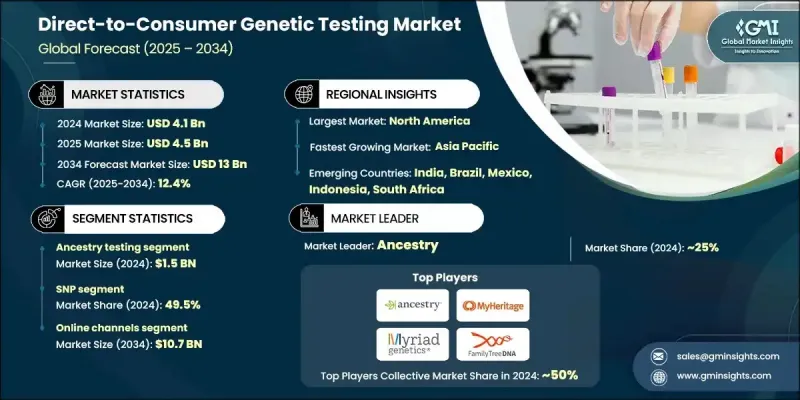

세계의 소비자 직접 의뢰(DTC) 유전자 검사 시장은 2024년 41억 달러에 달했고, CAGR 12.4%로 성장해 2034년까지 130억 달러에 이를 것으로 추정됩니다.

급성장의 배경에는 개인화된 건강과 웰빙 솔루션에 대한 소비자 수요 증가가 있습니다. 더 많은 개인, 특히 젊은 층이 자신의 건강, 가계, 라이프 스타일에 대한 더 깊은 통찰력을 요구함에 따라 가정에서의 유전 검사 수요가 가속화되고 있습니다. 이 검사는 건강 관리 중개자를 필요로 하지 않으며 간단한 타액과 뺨 면봉으로 접근 가능한 결과를 제공합니다. 소비자 직접 의뢰 유전자 검사는 예측 및 경력 검사, 약리 유전체학, 스킨케어, 영양, 가계, 형질분석 등 다양한 용도를 다루고 있습니다. 이러한 유전적 통찰력을 디지털 헬스툴과 모바일 앱에 통합하는 움직임이 활발해지고 있는 것도 주요 시장 성장 촉진요인입니다. 웨어러블 및 건강 추적 플랫폼은 유전자 데이터와 동기화되어 개인에 맞는 피트니스, 영양, 웰빙 권장 사항을 제공합니다. 이러한 유전 검사와 일상적인 건강 기술의 연계는 사용자 경험을 향상시키고 소비자에게 널리 호소하고 있습니다. 능동적인 건강 관리로의 전환은 실시간 및 재단사의 통찰력에 대한 소비자의 기대의 진화와 함께 더 넓은 인구 기반으로 시장 침투를 계속 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 41억 달러 |

| 예측 금액 | 130억 달러 |

| CAGR | 12.4% |

조상 검사 분야는 2024년 15억 달러를 창출했습니다. 소비자는 조상검사가 만족시키는 적정한 가격, 이해의 용이함, 개인적 호기심에 점점 더 매료되고 있습니다. 이러한 검사는 유산을 따라가고, 세계의 민족적 배경을 발견하고, 가족의 연결을 탐구하는 방법을 제공합니다. 이 부문을 견인하는 기업은 대규모 DNA 데이터베이스, 소비자 친화적인 플랫폼, 적극적인 마케팅 전략을 활용하여 도달범위를 확대하고 있습니다. 종합적이고 매력적인 조상에 대한 통찰력을 사용하기 쉬운 형태로 제공하는 능력으로 인해 이 부문의 인기가 크게 증가하고 있습니다.

2024년에는 단일염기 다형성(SNP) 기술이 49.5%의 점유율을 차지했습니다. 대규모 데이터 세트에서 수천 개의 유전자 변이를 확인할 수 있는 확장성과 효율성으로 인해 소비자 용도에 이상적입니다. SNP 칩은 유전 형질, 건강 소인, 조상 분석에 널리 사용됩니다. 이 기술은 신속한 처리, 검사 비용 절감, 높은 신뢰성을 제공하며, 이들은 대량의 소비자 직접 검사에서 합리적인 가격과 속도를 유지하는 데 필수적입니다. 이러한 확장성을 통해 SNP 기술은 현재 사용 가능한 많은 주요 유전자 검사 제품의 백본으로 자리매김하고 있습니다.

2024년 북미 소비자 직접 의뢰 유전자 검사 점유율은 48.6%였습니다. 이 지역은 소비자 인지도, 고급 디지털 건강 인프라 및 조기 도입 마인드 세트의 강력한 조합으로 이익을 얻고 있습니다. 개인화된 건강 도구에 대한 높은 참여, 지원 규제 프레임워크, 건강 최적화에 대한 국민의 강한 관심은 미국과 캐나다에서 DTC 검사 생태계를 더욱 강화하고 있습니다. 게다가 주요 업계 기업들의 적극적인 존재감과 유전자 검사와 디지털 웰니스 플랫폼 간의 연계 증가가 시장 성장을 가속화하고 지역 리더십을 강화하고 있습니다.

세계 소비자 직접 의뢰 유전자 검사 시장을 형성하는 주요 기업으로는 DNA Genotek, Dante Lab, The SkinDNA Company, Family Tree DNA (Gene By Gene), Easy DNA, Tempus AI, MedGenome, Helix, MyHeritage, Nutrigenomix, HomeDNA, Veritas Intercontinental, Mapmygenome, Blueprint Genetics, Fulgent Genetics, Pathway Genomics, Genova Diagnostics (GDX), DNA Complete, Myriad Genetics, Inc., Living DNA, Ancestry, Quest Diagnostics, Genesis Healthcare, and Identigene 등이 있습니다. 소비자 직접 의뢰 유전자 검사 시장의 각 회사는 다국어 플랫폼 및 현지 파트너와의 제휴를 통해 세계 프레즌스 확대에 주력하고 있습니다. 주요 기업은 실시간 건강 데이터와 유전 통찰력을 통합하여 사용하기 쉬운 모바일 앱에 투자하여 고객 참여도를 높이고 있습니다. 검사 패널을 정기적으로 업데이트하고 피부 관리 및 웰빙 유전자와 같은 틈새 검사 범주를 도입하면 기업이 새로운 계층을 개척하는 데 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유전학적 지식에 기초한 개인화된 솔루션에 대한 수요 증가

- 유전체 서열 분석에서 기술의 진보

- 유전성 질환에 대한 의식 증가

- 온라인 채널을 통해 DTC에 대한 액세스 확대

- 업계의 잠재적 위험 및 과제

- 개인정보 보호 및 데이터 보안

- 엄격한 규제상의 과제

- 시장 기회

- 온라인 배포 채널 확대

- 전략적 제휴와 파트너십

- 신흥 시장으로의 침투 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 미국

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 라틴아메리카

- 중동 및 아프리카

- 유전자 검사 업계에서의 투자와 자금 조달의 상황

- 기술적 상황

- 신흥기술

- 현재의 기술

- 데이터 프라이버시에 대한 우려

- 밸류체인 분석

- 환급 시나리오

- 가격 분석

- 미래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 검사 유형별, 2021-2034년

- 주요 동향

- 보균자 스크리닝

- 예측 검사

- 조상 검사

- 영양 유전체 검사

- 약리 유전체 검사

- 스킨케어 검사

- 기타 검사 유형

제6장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 마이크로어레이 기반 검사

- 단일염기 다형성(SNP) 칩

- 총유전체 서열 분석(WGS)

- 기타 기술

제7장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 온라인 채널

- 시판약(OTC)

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Ancestry

- Blueprint Genetics

- Counsyl

- Dante Lab

- DNA Complete

- DNA Genotek

- Easy DNA

- Family Tree DNA(Gene By Gene)

- Fulgent Genetics

- Genesis Healthcare

- Genova Diagnostics(GDX)

- Helix

- HomeDNA

- Identigene

- Living DNA

- Mapmygenome

- MedGenome

- MyHeritage

- Myriad Genetics, Inc.

- Nutrigenomix

- Pathway genomics

- Quest Diagnostics

- Tempus AI

- The SkinDNA Company

- Veritas Intercontinental

The Global Direct-to-Consumer Genetic Testing Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 12.4% to reach USD 13 billion by 2034.

The rapid expansion is fueled by the rising consumer demand for personalized health and wellness solutions. As more individuals, especially younger demographics, seek deeper insights into their health, ancestry, and lifestyle, the demand for at-home genetic tests is accelerating. These tests eliminate the need for a healthcare intermediary, offering accessible results via simple saliva or cheek swabs. Direct-to-Consumer Genetic Testing covers a wide range of applications, including predictive and carrier testing, pharmacogenomics, skincare, nutrition, ancestry, and trait analysis. The growing integration of these genetic insights into digital health tools and mobile apps is also a key market driver. Wearables and health tracking platforms are increasingly syncing with genetic data to deliver personalized fitness, nutrition, and wellness recommendations. This alignment of genetic testing with everyday health technology is improving user experience and widening consumer appeal. The shift toward proactive health management, along with evolving consumer expectations for real-time and tailored insights, continues to support market penetration across a broader population base.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $13 Billion |

| CAGR | 12.4% |

The ancestry testing segment generated USD 1.5 billion in 2024. Consumers are increasingly drawn to the affordability, ease of understanding, and personal curiosity that ancestry testing satisfies. These tests offer a way to trace heritage, discover global ethnic backgrounds, and explore family connections. Companies driving this segment are leveraging large-scale DNA databases, consumer-friendly platforms, and aggressive marketing strategies to expand reach. Their ability to deliver comprehensive and engaging ancestry insights in an accessible format has significantly strengthened the popularity of this segment.

In 2024, the single-nucleotide polymorphism (SNP) technology held a 49.5% share. Its scalability and efficiency in identifying thousands of genetic variants across large datasets make it ideal for consumer-facing applications. SNP chips are extensively used for analyzing genetic traits, health predispositions, and ancestry. The technology offers fast processing, reduced testing costs, and high reliability, which are critical for maintaining affordability and speed in high-volume direct-to-consumer testing. This scalability has positioned SNP technology as the backbone of many leading genetic testing products available today.

North America Direct-to-Consumer Genetic Testing Market held a 48.6% share in 2024. The region benefits from a strong mix of consumer awareness, advanced digital health infrastructure, and an early adoption mindset. High engagement with personalized health tools, supportive regulatory frameworks, and strong public interest in health optimization are further boosting the DTC testing ecosystem in the U.S. and Canada. In addition, the active presence of key industry players and increasing alignment between genetic testing and digital wellness platforms are accelerating market growth and strengthening regional leadership.

Some of the major players shaping the Global Direct-to-Consumer Genetic Testing Market include DNA Genotek, Dante Lab, The SkinDNA Company, Family Tree DNA (Gene By Gene), Easy DNA, Tempus AI, MedGenome, Helix, MyHeritage, Nutrigenomix, HomeDNA, Veritas Intercontinental, Mapmygenome, Blueprint Genetics, Fulgent Genetics, Pathway Genomics, Genova Diagnostics (GDX), DNA Complete, Myriad Genetics, Inc., Living DNA, Ancestry, Quest Diagnostics, Genesis Healthcare, and Identigene. Companies in the DTC genetic testing market are focusing on expanding their global presence through multilingual platforms and local partnerships. Key players are investing in user-friendly mobile apps that integrate real-time health data with genetic insights to enhance customer engagement. Regular updates to testing panels and the introduction of niche test categories, such as skincare and wellness genetics, are helping companies reach new demographics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Technology trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for personalized solutions based on genetic insights

- 3.2.1.2 Growing technology advancement in genomic sequencing

- 3.2.1.3 Increased awareness of genetic disorders

- 3.2.1.4 Expanding accessibility of DTC through online channels

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Privacy and data security

- 3.2.2.2 Stringent regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of online distribution channels

- 3.2.3.2 Strategic alliances and partnerships

- 3.2.3.3 Increasing penetration in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.4.2.1 Germany

- 3.4.2.2 UK

- 3.4.2.3 France

- 3.4.2.4 Spain

- 3.4.2.5 Italy

- 3.4.3 Asia Pacific

- 3.4.3.1 China

- 3.4.3.2 Japan

- 3.4.3.3 India

- 3.4.3.4 Australia

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Investment and funding landscape in the genetic testing industry

- 3.6 Technological landscape

- 3.6.1 Emerging technologies

- 3.6.2 Current technologies

- 3.7 Data privacy concerns

- 3.8 Value chain analysis

- 3.9 Reimbursement scenario

- 3.10 Pricing analysis

- 3.11 Future market trends

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Carrier screening

- 5.3 Predictive testing

- 5.4 Ancestry testing

- 5.5 Nutrigenomic testing

- 5.6 Pharmacogenomic testing

- 5.7 Skincare testing

- 5.8 Other test types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Microarray-based testing

- 6.3 Single-nucleotide polymorphism (SNP) chips

- 6.4 Whole genome sequencing (WGS)

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Online channels

- 7.3 Over-the-counter (OTC)

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ancestry

- 9.2 Blueprint Genetics

- 9.3 Counsyl

- 9.4 Dante Lab

- 9.5 DNA Complete

- 9.6 DNA Genotek

- 9.7 Easy DNA

- 9.8 Family Tree DNA (Gene By Gene)

- 9.9 Fulgent Genetics

- 9.10 Genesis Healthcare

- 9.11 Genova Diagnostics (GDX)

- 9.12 Helix

- 9.13 HomeDNA

- 9.14 Identigene

- 9.15 Living DNA

- 9.16 Mapmygenome

- 9.17 MedGenome

- 9.18 MyHeritage

- 9.19 Myriad Genetics, Inc.

- 9.20 Nutrigenomix

- 9.21 Pathway genomics

- 9.22 Quest Diagnostics

- 9.23 Tempus AI

- 9.24 The SkinDNA Company

- 9.25 Veritas Intercontinental