|

시장보고서

상품코드

1959608

산업기계 부품 및 센서 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Machinery Components and Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

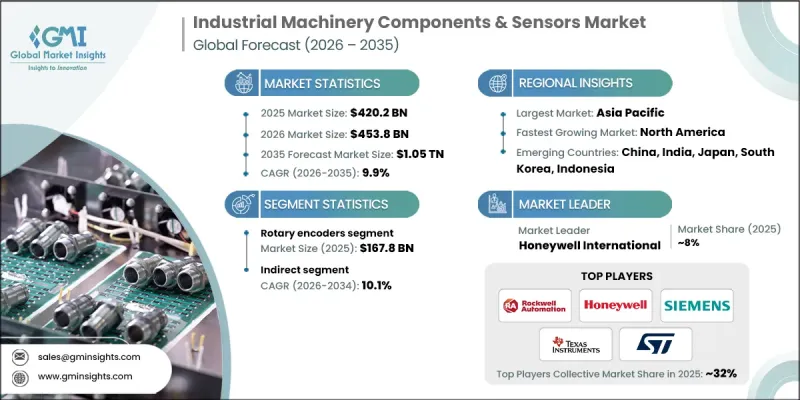

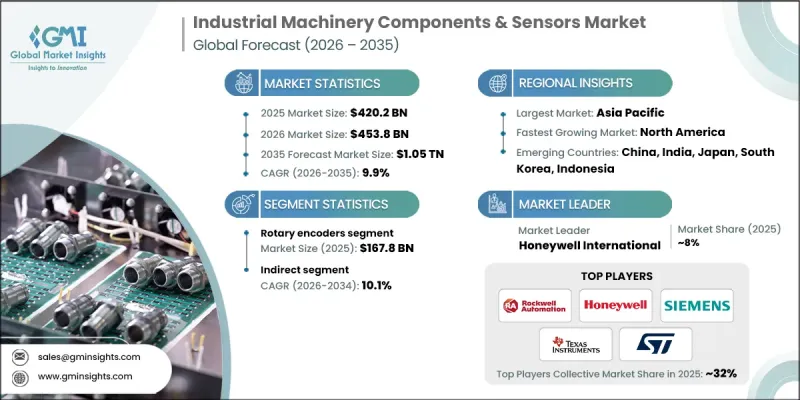

세계의 산업기계 부품 및 센서 시장은 2025년에 4,202억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.9%로 성장하여 1조 500억 달러에 이를 것으로 예측됩니다.

시장 확대는 제조 환경 전반에 걸쳐 산업 자동화 및 첨단 로봇 공학의 도입이 가속화됨에 따라 추진되고 있습니다. 생산 시설에서 더 높은 처리량, 정확성 및 운영의 일관성을 우선시함에 따라, 정확한 모션 제어와 실시간 성능 모니터링을 가능하게 하는 고성능 부품 및 지능형 감지 시스템에 대한 수요가 증가하고 있습니다. 내구성이 뛰어난 기계 부품과 견고한 센서는 자동화 집약적 환경에서 기능 중단을 방지하는 데 필수적입니다. 실시간 데이터 수집은 기계 간 협업, 프로세스 최적화, 시스템 효율성 향상을 지원합니다. 스마트 팩토리 생태계에 대한 투자 확대는 첨단 센싱 기술로 뒷받침되는 상호 연결 장비의 필요성을 더욱 강화하고 있습니다. 산업 운영자들은 인적 오류를 최소화하고 생산성을 높이기 위해 자동화에 대한 의존도를 점점 더 높이고 있습니다. 이와 함께, 예지보전 전략의 도입 확대는 고가의 다운타임이 발생하기 전에 잠재적인 장비 고장을 식별할 수 있는 상태 모니터링 센서에 대한 수요를 촉진하여 장기적인 시장 성장을 가속하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 4,202억 달러 |

| 예측 금액 | 1조 500억 달러 |

| CAGR | 9.9% |

로터리 엔코더 부문은 2025년 1,678억 달러 시장 규모를 기록할 것으로 예상되며, 2026년부터 2035년까지 연평균 10.2%의 성장률을 보일 것으로 예측됩니다. 로터리 엔코더는 자동화 시스템 내에서 고정밀 위치 및 속도 피드백을 제공할 수 있는 특성으로 인해 시장에서 선도적인 위치를 유지하고 있습니다. 그 정밀성은 복잡한 기계 플랫폼 전체에서 모션 제어의 효율성을 높이고 있습니다. 로봇 공학, 컴퓨터 제어 제조 장비, 자동 자재 이송 시스템의 안정적인 수요가 부문 확장을 지속적으로 뒷받침하고 있습니다. 제조업체들은 연속 사용 조건에서의 작동 신뢰성과 시스템 통합을 단순화하는 컴팩트한 구조로 인해 로터리 엔코더를 선호하고 있습니다. 디지털 처리 능력의 지속적인 향상으로 해상도 정확도와 신호 안정성이 더욱 향상되어 공장 자동화에서 장기적인 중요성이 강화되고 있습니다.

자동차 부문은 2025년 20.54%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 10.4%의 성장률을 보일 것으로 전망됩니다. 자동차 제조는 자동화에 크게 의존하고 있으며, 첨단 산업용 센서 및 정밀 기계 부품에 대한 지속적인 수요를 주도하고 있습니다. 모션 피드백 시스템은 조립 라인의 정밀도와 로봇의 동기화에 중요한 역할을 합니다. 전기자동차의 생산 확대는 첨단 센싱 기술과 고성능 제어 솔루션의 필요성을 높이고 있습니다. 자동차 생산 시설 전반에 걸친 엄격한 품질 보증 기준은 신뢰할 수 있는 모니터링 및 피드백 메커니즘의 도입을 더욱 촉진하고 있습니다.

중국의 산업기계 부품 및 센서 시장은 2025년 556억 달러에 달할 것으로 예상되며, 2026-2035년 연평균 10.4%의 성장률을 보일 것으로 전망됩니다. 견조한 제조업 생산량과 지속적인 산업 현대화 노력이 시장 확대를 뒷받침하고 있습니다. 국가 차원의 자동화 전략으로 생산 인프라에 첨단 센서 기술의 통합이 가속화되고 있습니다. 높은 기계 가동률은 장수명 설계의 내구성 부품에 대한 지속적인 수요를 창출하고 있습니다. 스마트 제조 생태계의 발달로 실시간 모니터링 시스템 도입이 증가하고 있습니다. 전기 모빌리티와 배터리 생산의 성장은 정밀 센싱 기술과 모션 제어 기술에 대한 수요를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 부품 유형별, 2022-2035년

제6장 시장 추산·예측 : 최종 이용 산업별, 2022-2035년

제7장 시장 추산·예측 : 유통 채널별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

LSH 26.03.26The Global Industrial Machinery Components & Sensors Market was valued at USD 420.2 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 1.05 trillion by 2035.

Market expansion is propelled by the accelerating adoption of industrial automation and advanced robotics across manufacturing environments. As production facilities prioritize higher throughput, precision, and operational consistency, demand is rising for high-performance components and intelligent sensing systems that enable accurate motion control and real-time performance monitoring. Durable mechanical parts and robust sensors are essential to ensure uninterrupted functionality in automation-intensive settings. Real-time data acquisition supports machine coordination, process optimization, and improved system efficiency. Growing investment in smart factory ecosystems further strengthens the need for interconnected equipment supported by advanced sensing technologies. Industrial operators increasingly rely on automation to minimize manual errors and enhance productivity. In parallel, the growing implementation of predictive maintenance strategies is fueling demand for condition monitoring sensors capable of identifying potential equipment failures before costly downtime occurs, reinforcing long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $420.2 Billion |

| Forecast Value | $1.05 Trillion |

| CAGR | 9.9% |

The rotary encoders segment generated USD 167.8 billion in 2025 and is forecast to grow at a CAGR of 10.2% between 2026 and 2035. Rotary encoders maintain strong market leadership due to their ability to deliver highly accurate position and speed feedback within automated systems. Their precision enhances motion control efficiency across complex machinery platforms. Consistent demand from robotics, computer-controlled manufacturing equipment, and automated material movement systems continues to support segment expansion. Manufacturers favor rotary encoders for their operational reliability under continuous usage conditions and their compact structure, which simplifies system integration. Ongoing improvements in digital processing capabilities are further elevating resolution accuracy and signal stability, reinforcing their long-term relevance in factory automation.

The automotive segment held 20.54% share in 2025 and is projected to grow at a CAGR of 10.4% through 2035. Vehicle manufacturing relies heavily on automation, driving sustained demand for advanced industrial sensors and precision mechanical components. Motion feedback systems play a vital role in assembly line accuracy and robotic synchronization. The expanding production of electric vehicles is increasing the requirement for advanced sensing technologies and high-performance control solutions. Stringent quality assurance standards across automotive production facilities are further encouraging the adoption of reliable monitoring and feedback mechanisms.

China Industrial Machinery Components & Sensors Market reached USD 55.6 billion in 2025 and is anticipated to grow at a CAGR of 10.4% from 2026 to 2035. Strong manufacturing output and continuous industrial modernization efforts are supporting market expansion. National automation strategies are accelerating the integration of advanced sensor technologies within production infrastructure. High machinery utilization rates create ongoing demand for durable components engineered for long operational life. The development of smart manufacturing ecosystems is increasing the deployment of real-time monitoring systems. Growth in electric mobility and battery production is further strengthening demand for precision sensing and motion control technologies.

Key companies operating in the Global Industrial Machinery Components & Sensors Market include Siemens, Honeywell International, Rockwell Automation, Robert Bosch, Amphenol Corporation, SICK AG, STMicroelectronics, Texas Instruments Incorporated, Denso Corporation, Pepperl+Fuchs, KELLER AG, Merit Sensor Systems, First Sensor, and di-soric GmbH & Co. KG. Companies in the industrial machinery components & sensors market are reinforcing their competitive position through continuous innovation, strategic acquisitions, and expansion of smart automation portfolios. Many industry leaders are investing in advanced sensing technologies, AI-enabled analytics, and IoT-integrated platforms to support predictive maintenance and real-time monitoring. Partnerships with manufacturing OEMs and robotics providers enable deeper system integration and long-term supply agreements. Firms are also strengthening global distribution networks and enhancing customization capabilities to address sector-specific requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component Type

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of industrial automation and robotics adoption

- 3.2.1.2 Rising deployment of predictive maintenance solutions

- 3.2.1.3 Implementation of Industry 4.0 and smart manufacturing frameworks

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High integration and installation costs

- 3.2.2.2 Interoperability issues with legacy machinery

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of smart factories and connected ecosystems

- 3.2.3.2 Development of cybersecurity-enabled sensor networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Component Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Rotary encoders

- 5.3 Process control sensors

- 5.4 Circuit protection devices

- 5.5 Power and Signal Components

- 5.6 Interface and Control Components

Chapter 6 Market Estimates & Forecast, By End-Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automotive Industry

- 6.3 Electronics and Semiconductor

- 6.4 Food and Beverage

- 6.5 Pharmaceutical and Biotechnology

- 6.6 Energy and Utilities

- 6.7 Aerospace and Defense

- 6.8 Chemical and Process Industries

- 6.9 Mining and Metals

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Amphenol Corporation

- 9.2 Denso Corporation

- 9.3 di-soric GmbH & Co. KG

- 9.4 First Sensor

- 9.5 Honeywell International

- 9.6 KELLER AG

- 9.7 Merit Sensor Systems

- 9.8 Pepperl+Fuchs

- 9.9 Robert Bosch

- 9.10 Rockwell Automation

- 9.11 SICK AG

- 9.12 Siemens

- 9.13 STMicroelectronics

- 9.14 Texas Instruments Incorporated