|

시장보고서

상품코드

1858834

자동차용 그래핀 강화 부품 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Graphene-Enhanced Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

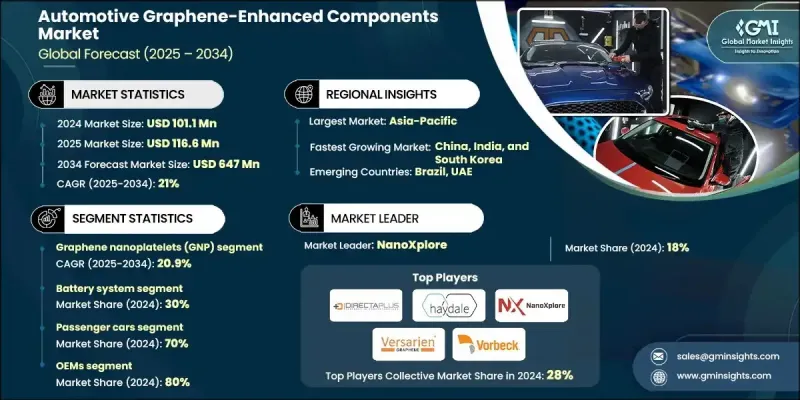

세계의 자동차용 그래핀 강화 부품 시장은 2024년에 1억 110만 달러로 평가되었고 CAGR 21%로 성장하고 2034년까지는 6억 4,700만 달러에 달할 것으로 예측되고 있습니다.

이 급성장의 배경은 강도, 경량 설계, 우수한 에너지 성능을 실현하는 재료에 대한 수요가 증가하는 데 있습니다. 그래핀의 탁월한 전도성, 열제어성, 기계적 내구성은 효율성 향상과 저출력 가스화를 목표로 하는 자동차 제조업체들에게 선호되고 있습니다. OEM과 Tier-1 공급업체들이 투자를 확대하는 가운데 업계는 실험적 활용에서 대규모 도입으로 전환하고 있습니다. 아시아태평양, 북미 및 유럽의 주요 시장에서 전동화는 그래핀을 강화한 배터리, 열 시스템, 구조 부품의 채용을 뒷받침하는 중요한 촉매가 되고 있습니다. 자동차 제조업체는 경쟁력을 높이기 위해 재료 개발 기업 및 연구 기관과의 공동 연구 개발에 적극적으로 임하고 있습니다. 경량 그래핀 강화 복합재료는 기존의 금속 부품에 서서히 대체하고 있으며, 연비 향상과 EV 주행 거리의 연장에 직접 공헌하고 있습니다. 이러한 세계 동향은 지속가능한 자동차 생산과 탄소 배출량 감소를 추진하는 엄격한 규제 목표와 일치하고 차세대 자동차 제조에서 그래핀의 장기적인 잠재력을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 1억110만 달러 |

| 예측금액 | 6억 4,700만 달러 |

| CAGR | 21% |

배터리 시스템 분야는 2024년에 30%의 점유율을 차지했습니다. 전기자동차의 보급이 진행됨에 따라 우수한 전도성과 에너지 밀도를 제공하는 그래핀 대응 배터리 솔루션에 대한 수요가 높아지고 있습니다. 이러한 진보는 초고속 충전, 배터리 수명 향상, 열 안전성 개선 등의 기능을 지원합니다. 그 결과, 이 분야에서는 성능 향상에 중점을 둔 자동차 제조업체와 공급업체의 강한 참여가 계속되고 있습니다.

그래핀 나노플레이트렛(GNP) 분야는 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 20.9%를 나타낼 것으로 예측됩니다. GNP는 합리적인 가격, 확장성, 균형 잡힌 기계적 및 열적 성능으로 활용됩니다. GNP는 구조 복합재료, 배터리 전극, 기능성 코팅 등 다양한 용도로 지지를 모으고 있습니다. 비용 효율적인 프로파일과 다기능 성능으로 대규모 자동차 통합에 적합한 옵션이 되었습니다.

미국의 자동차용 그래핀 강화 부품 시장은 2024년 2,330만 달러에 달하였고, 자동차용 그래핀 강화 부품의 주요 시장으로 부상하고 있습니다. EV 보급의 활성화와 엄격한 배출 가스 및 연비 규제가 성장을 지지하고 있습니다. 미국 제조업체는 상용차와 승용차의 두 부문에서 성능 벤치마크를 충족시키기 위해 그래핀 기반 배터리 팩, 전자 제품 및 열 시스템을 빠르게 도입하고 있습니다.

세계의 자동차용 그래핀 강화 부품 시장을 형성하는 유력 기업으로는 Vorbeck Materials, First Graphene, Graphene Nanochem, NanoXplore, Graphenea, Directa Plus, Applied Graphene Materials(AGM), Nanotech Energy, Versarien, Haydale Graphene Industries 등이 있습니다. 자동차용 그래핀 강화 부품 시장의 지위를 확고히 하기 위해, 주요 기업은 기술 혁신, 확장성, 파트너십에 초점을 맞춘 주요 전략을 채택하고 있습니다. 많은 기업들은 배터리 효율, 열 조절, 구조 강도 등 특정 자동차 기능을 위해 맞춤화된 그래핀 배합의 개발을 선호합니다. 기업은 또한 비용과 성능의 균형을 최적화하면서 대량 생산을 지원하기 위한 고급 제조 기술에 투자하고 있습니다. 자동차 OEM, 연구 대학, 재료 공급업체와의 전략적 제휴는 제품 테스트와 상업 개발을 가속화하는 데 도움이 됩니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- EV 생산과 배터리 채용 증가

- 경량화와 연비 목표

- 고성능 일렉트로닉스의 대두

- 나노 재료 연구 개발에 대한 강력한 투자

- 업계의 잠재적 리스크 및 과제

- 그래핀 재료의 높은 생산 비용

- 한정된 대규모 공급망

- 시장 기회

- 차세대 EV용 배터리와 슈퍼커패시터

- 열 관리 시스템의 채용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 전망

- 현재의 기술 동향

- 신흥기술

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국

- 이용 사례와 응용

- 최상의 시나리오

- 비용효과 분석과 ROI 최적화

- 재료 비용과 성능의 트레이드 오프

- 제조 비용 영향 평가

- 총소유비용 모델

- 가치 엔지니어링 전략

- 지적재산과 기술 라이선싱

- 특허 정세 분석

- 기술 라이선싱 모델

- 보호 전략

- 영업의 자유도 평가

- 시장 도입과 고객 수용

- OEM의 의사결정 기준

- 소비자의 인식과 수용

- 시장 교육과 의식 향상 프로그램

- 경쟁차별화 전략

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발표

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 언더후드 컴포넌트

- 폼 커버

- 연료 레일 커버

- 펌프 커버

- 구조용 복합재료

- 배터리 시스템 부품

- 열 관리 시스템

- 전자부품

제6장 시장 추계 및 예측 : 그래핀 재료별(2021-2034년)

- 주요 동향

- 그래핀 나노 플레이트렛(GNP)

- 산화 그래핀(GO)

- 환원 그래핀 산화물(RGO)

- CVD 그래핀 필름

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓 서비스 제공업체

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Applied Graphene Materials

- Directa Plus

- First Graphene

- Graphenea

- Haydale Graphene Industries

- Nanotech Energy

- NanoXplore

- Versarien

- Vorbeck Materials

- XG Sciences

- 지역 기업

- Angstron Materials

- Black Swan Graphene

- Graphene NanoChem

- Graphene 3D Lab

- Global Graphene Group

- Nanocyl

- Skeleton Technologies

- Talga Resources

- Graphmatech

- 신흥 기업/시장파괴자

- Archer Materials

- Avancis Graphene

- Cnano Technology

- Elcora Advanced Materials

- Garmor Graphene

- Grolltex

- NanoGraphene

- Zap &Go

- 2D Carbon Tech

The Global Automotive Graphene-Enhanced Components Market was valued at USD 101.1 million in 2024 and is estimated to grow at a CAGR of 21% to reach USD 647 million by 2034.

This rapid growth is fueled by the increasing demand for materials that deliver strength, lightweight design, and superior energy performance. Graphene's exceptional conductivity, thermal regulation, and mechanical durability make it a preferred choice for automakers aiming to enhance efficiency and lower emissions. The industry is witnessing a shift from experimental usage to large-scale implementation as OEMs and Tier-1 suppliers ramp up investments. Electrification across major markets in Asia Pacific, North America, and Europe is a key catalyst, pushing the adoption of graphene-enhanced batteries, thermal systems, and structural components. Automotive manufacturers are actively engaging in R&D collaborations with material developers and research institutions to gain a competitive edge. Lightweight graphene-reinforced composites are gradually replacing traditional metal parts, directly contributing to better fuel economy and longer EV driving range. These trends align with stringent regulatory goals that promote sustainable automotive production and reduction in carbon emissions globally, reinforcing the long-term potential of graphene in next-generation vehicle manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $101.1 Million |

| Forecast Value | $647 Million |

| CAGR | 21% |

The battery system segment held a 30% share in 2024. The rising penetration of electric vehicles is fueling demand for graphene-enabled battery solutions, as they offer superior conductivity and energy density. These advancements support features such as ultra-fast charging, enhanced battery life, and improved thermal safety. As a result, the segment continues to see strong engagement from automakers and suppliers focused on performance improvement.

The graphene nanoplatelets (GNP) segment will grow at a CAGR of 20.9% between 2025 and 2034. GNPs are used for their affordability, scalability, and balanced mechanical and thermal performance. They are gaining traction in a broad array of applications, including structural composites, battery electrodes, and functional coatings. Their cost-effective profile and multi-functional performance make them a preferred choice for large-scale automotive integration.

United States Automotive Graphene-Enhanced Components Market reached USD 23.3 million in 2024, emerging as a key market for automotive graphene-enhanced components. Growth is supported by strong EV adoption and strict emissions and fuel efficiency regulations. American manufacturers are rapidly deploying graphene-based battery packs, electronics, and thermal systems to meet performance benchmarks in both commercial and passenger vehicle segments.

Prominent companies shaping the Global Automotive Graphene-Enhanced Components Market include Vorbeck Materials, First Graphene, Graphene Nanochem, NanoXplore, Graphenea, Directa Plus, Applied Graphene Materials (AGM), Nanotech Energy, Versarien, and Haydale Graphene Industries. To solidify their position in the Automotive Graphene-Enhanced Components Market, leading companies are adopting key strategies focused on innovation, scalability, and partnerships. Many are prioritizing the development of tailored graphene formulations for specific automotive functions such as battery efficiency, thermal regulation, and structural strength. Firms are also investing in advanced manufacturing technologies to support mass production, while optimizing the cost-performance balance. Strategic collaborations with automotive OEMs, research universities, and materials suppliers are helping accelerate product testing and commercial rollout.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Graphene material

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing EV production and battery adoption

- 3.2.1.2 Lightweighting and fuel efficiency targets

- 3.2.1.3 Rise in high-performance electronics

- 3.2.1.4 Strong investments in nanomaterials R&D

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production cost of graphene materials

- 3.2.2.2 Limited large-scale supply chain

- 3.2.3 Market opportunities

- 3.2.3.1 Next-gen EV batteries and supercapacitors

- 3.2.3.2 Adoption in thermal management systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Cost-benefit analysis & roi optimization

- 3.12.1 Material cost vs performance trade-offs

- 3.12.2 Manufacturing cost impact assessment

- 3.12.3 Total cost of ownership models

- 3.12.4 Value engineering strategies

- 3.13 Intellectual property & technology licensing

- 3.13.1 Patent landscape analysis

- 3.13.2 Technology licensing models

- 3.13.3 Protection strategies

- 3.13.4 Freedom-to-operate assessments

- 3.14 Market adoption & customer acceptance

- 3.14.1 OEM decision-making criteria

- 3.14.2 Consumer perception & acceptance

- 3.14.3 Market education & awareness programs

- 3.14.4 Competitive differentiation strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Under-hood components

- 5.2.1 Foam covers

- 5.2.2 Fuel rail covers

- 5.2.3 Pump covers

- 5.3 Structural composites

- 5.4 Battery system components

- 5.5 Thermal management systems

- 5.6 Electronic components

Chapter 6 Market Estimates & Forecast, By Graphene Material, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Graphene nanoplatelets (GNP)

- 6.3 Graphene oxide (GO)

- 6.4 Reduced graphene oxide (RGO)

- 6.5 CVD graphene films

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket & Service Providers

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Applied Graphene Materials

- 10.1.2 Directa Plus

- 10.1.3 First Graphene

- 10.1.4 Graphenea

- 10.1.5 Haydale Graphene Industries

- 10.1.6 Nanotech Energy

- 10.1.7 NanoXplore

- 10.1.8 Versarien

- 10.1.9 Vorbeck Materials

- 10.1.10 XG Sciences

- 10.2 Regional Players

- 10.2.1 Angstron Materials

- 10.2.2 Black Swan Graphene

- 10.2.3 Graphene NanoChem

- 10.2.4. Graphene 3D Lab

- 10.2.5 Global Graphene Group

- 10.2.6 Nanocyl

- 10.2.7 Skeleton Technologies

- 10.2.8 Talga Resources

- 10.2.9 Graphmatech

- 10.3 Emerging Players / Disruptors

- 10.3.1 Archer Materials

- 10.3.2 Avancis Graphene

- 10.3.3 Cnano Technology

- 10.3.4 Elcora Advanced Materials

- 10.3.5 Garmor Graphene

- 10.3.6 Grolltex

- 10.3.7 NanoGraphene

- 10.3.8 Zap & Go

- 10.3.9. 2 D Carbon Tech