|

시장보고서

상품코드

1858865

V2X 통신 칩 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)V2X Communication Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 V2X 통신 칩 시장 규모는 2024년에 14억 3,000만 달러로 평가되었고, CAGR 23.3%로 성장할 전망이며, 2034년에는 117억 1,000만 달러에 달할 것으로 예측되고 있습니다.

성장의 원동력이 되고 있는 것은 자동차와 인프라의 에코시스템 전체에 있어서의 커넥티드 차량 기술 통합의 고조입니다. V2X 통신 칩은 자동차, 교통 인프라, 보행자 및 휴대폰 연결을 넘어서는 네트워크 간의 직접적인 상호작용을 가능하게 하고, 교통 안전, 교통 효율, 긴급 대응, 협력 이동성을 지원하는 실시간 통신을 보장합니다. 자동차 OEM, 정부기관, 기술 공급자가 연결 드라이브와 자율주행을 향해 움직이는 가운데, 이러한 칩에 대한 수요는 증가의 길을 따라가고 있습니다. 반도체 기업은 도시와 고속도로 환경에 맞게 확장 가능하고 안전하며 저지연의 V2X 칩셋을 적극적으로 개발하고 있습니다. 자동차 제조업체, 칩 개발자 및 통신 제공업체 간의 협력으로 이러한 시스템의 전개가 가속화되고 있습니다. 지역에 따라 선호도가 다르기 때문에 대기업은 DSRC와 C-V2X를 모두 지원하는 듀얼 호환 솔루션을 개발하고 있습니다. 보급이 확대됨에 따라 업계의 초점은 V2X 기술의 대량 시장 개발을 지원하기 위해 단가 절감 및 탄력있는 공급망 구축으로 옮겨가고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도년 | 2025-2034 |

| 시장 규모 | 14억 3,000만 달러 |

| 예측 금액 | 117억 1,000만 달러 |

| CAGR | 23.3% |

자동차 간(V2V) 통신 부문은 2024년에 39%의 점유율을 차지했으며, 핵심 V2X 용도에서 매우 중요한 역할을 반영합니다. 이러한 칩은 차량 간의 직접적인 정보 교환을 용이하게 하고, 사각 감시, 충돌 회피, 차선 변경 지원 등의 기능을 실현하는 데 필수적입니다. OEM은 안전 규정을 준수하고 자율 주행 기능을 지원하기 위해 상용 차량과 승용차 모두에 V2V 통신 기능을 통합합니다. 규제기관이 자동차의 안전성에 관한 보다 높은 기준을 요구하고 있기 때문에 이 분야는 앞으로도 가속해 갈 것으로 예측됩니다.

2024년 DSRC(Dedicated Short-Range Communications) 부문은 2034년까지 연평균 복합 성장률(CAGR) 28.8%로 성장할 전망입니다. 5.9GHz 대역에서 작동하는 DSRC는 차량과 주변 인프라 간의 단거리 및 저지연 통신을 제공합니다. DSRC는 긴급 브레이크, 사고 경보, 교통 시나리오에서 차량 우선 순위 지정 등 안전하고 중요한 용도에 널리 사용됩니다. 북미와 유럽의 일부에서는 이미 초기 단계에서의 도입이 보이고, DSRC는 지역의 규제 틀에 뒷받침된 초기의 V2X 인프라 전개에 있어서 계속 중요한 역할을 하고 있습니다.

중국의 V2X 통신 칩 2024년 시장 규모는 4억 1,700만 달러로 평가되었습니다. 2024년 자동차 생산 대수는 3,130만 대, 연율 4% 증가로 급확대하고 있으며, V2X 칩의 보급을 뒷받침하고 있습니다. 스마트 교통, 자율 이동성, 디지털 인프라에 중점을 둔 정부 주도 노력은 V2X 시스템의 전개를 가속화하고 있습니다. 국가 정책, 파일럿 프로젝트, 지능형 교통 솔루션에 대한 요구가 높아지면서 이 지역의 이 나라의 주도적 지위가 강화될 전망입니다.

세계의 V2X 통신 칩 시장에서 주요 기업으로는 Qualcomm, NXP Semiconductor, Infineon Technology, ST Microelectronics, Robert Bosch, Denso, Huawei Technology, Herman, Continental 등이 있습니다. V2X 통신 칩 시장의 각 회사는 그 존재를 확고하게 만들기 위해 몇 가지 핵심 전략에 주력하고 있습니다. 여기에는 DSRC 및 셀룰러 V2X 표준을 모두 지원하는 듀얼 모드 칩셋 개발과 같은 다양한 세계 규제 환경에 대한 대응이 포함됩니다. 또한 실시간 안전 요구 사항을 충족하고 EV 플랫폼의 배터리 수명을 연장하기 위해 초저지연, 전력 효율적인 아키텍처를 선호합니다. 자동차 제조업체 및 네트워크 제공업체와의 전략적 제휴를 통해 칩 설계를 차량 개발 일정 및 인프라 준비에 맞출 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도의 산출

- 시장 추계의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 커넥티드카 및 자율주행차의 도입 확대

- 정부가 교통안전 및 ITS 인프라 의무화

- 5G 호환성을 가지는 C-V2X에 대한 이행

- OEM과 반도체의 파트너십에 의한 확장성

- 업계의 잠재적 위험 및 과제

- 높은 통합 비용 및 테스트 비용

- DSRC 및 C-V2X 표준 간의 분단

- 시장 기회

- 스마트 시티 인프라 확대 및 5G 전개

- ADAS 및 자율주행 시스템과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 전망

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 지속가능성 및 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국

- 이용 사례 및 용도

- 베스트 시나리오

- 지역의 인프라 준비 상황

- 5G 네트워크의 보급

- 스마트 시티 개발 상황

- V2X 테스트를 위한 도로 인프라

- 벤치마크 및 KPI

- 칩의 성능 지표(레이턴시, 레인지, 신뢰성)

- 주요 기업 벤치마킹

- 업계표준 및 인증

- 시장 도입 시나리오

- 단기(1-3년) 채용 예측

- 중기(4-7년) 도입 예측

- 장기(8-10년) 도입 예측

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 통신별(2021-2034년)

- 주요 동향

- 차차간

- 차량 간 통신

- 차량 대 보행자

- 차량 간 통신

- 기타

제6장 시장 추계 및 예측 : 접속성별(2021-2034년)

- 주요 동향

- DSRC

- C-V2X

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 승용차

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 자율주행 지원

- 교통 관리

- 긴급 차량 통지

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Qualcomm

- NXP Semiconductors

- Huawei Technologies

- Infineon Technologies

- STMicroelectronics

- Continental

- Robert Bosch

- Denso Corporation

- Harman

- Intel Corporation

- 지역 기업

- Autotalks

- Commsignia

- Cohda Wireless

- Savari

- Panasonic Automotive

- 신흥 기업 및 디스랩터

- Veoneer

- Excelfore

- Visteon Corporation

- NXP Labs Startup Ventures

- KT Corporation Automotive Solutions

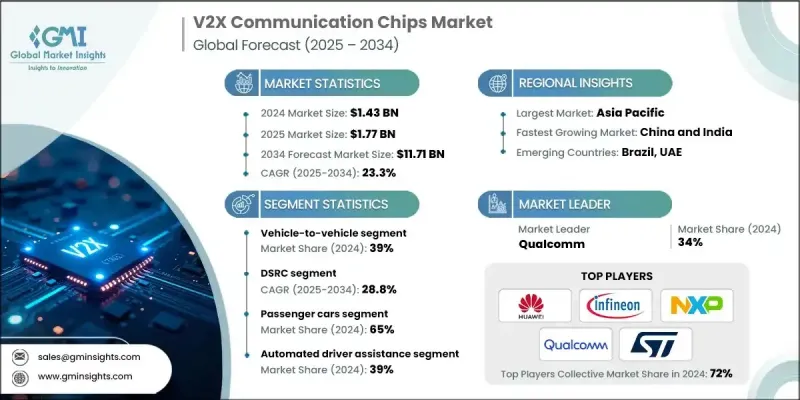

The Global V2X Communication Chips Market was valued at USD 1.43 billion in 2024 and is estimated to grow at a CAGR of 23.3% to reach USD 11.71 billion by 2034.

The growth is fueled by the rising integration of connected vehicle technologies across automotive and infrastructure ecosystems. V2X communication chips enable direct interaction between vehicles, traffic infrastructure, pedestrians, and networks beyond cellular connectivity, ensuring real-time communication that supports road safety, traffic efficiency, emergency response, and cooperative mobility. As automotive OEMs, government agencies, and tech providers move toward connected and autonomous driving, demand for these chips continues to grow. Semiconductor firms are actively developing scalable, secure, and low-latency V2X chipsets tailored for both urban and highway environments. Collaborations between automakers, chip developers, and telecom providers are accelerating the deployment of these systems. With regional preferences differing, major players are creating dual-compatible solutions supporting both DSRC and C-V2X. As adoption scales up, industry focus is shifting toward reducing unit costs and building resilient supply chains to support mass-market rollouts of V2X technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.43 Billion |

| Forecast Value | $11.71 Billion |

| CAGR | 23.3% |

The vehicle-to-vehicle (V2V) communication segment held a 39% share in 2024, reflecting its pivotal role in core V2X applications. These chips facilitate the direct exchange of information between vehicles, which is vital for enabling features like blind spot monitoring, collision avoidance, and lane-change assistance. OEMs are embedding V2V communication functions in both commercial and passenger vehicles to comply with safety regulations and support autonomous driving functionalities. As regulatory bodies push for higher standards in vehicle safety, this segment is expected to witness continued acceleration.

In 2024, the DSRC (Dedicated Short-Range Communications) segment will grow at a CAGR of 28.8% through 2034. Operating in the 5.9 GHz spectrum, DSRC provides short-range, low-latency communication between vehicles and surrounding infrastructure. It is widely used for safety-critical applications, including emergency braking, accident alerts, and vehicle prioritization in traffic scenarios. With early-stage adoption already visible in North America and certain parts of Europe, DSRC continues to play a strong role in initial V2X infrastructure deployments supported by regional regulatory frameworks.

China V2X Communication Chips Market generated USD 417 million in 2024. The country's rapid expansion in vehicle production, totaling 31.3 million units in 2024 with a 4% annual increase, is bolstering V2X chip adoption. Government-led initiatives focused on smart transportation, autonomous mobility, and digital infrastructure are accelerating the deployment of V2X systems. National policies, pilot projects, and the growing need for intelligent traffic solutions are expected to strengthen the country's leadership position in the region.

Key players in the Global V2X Communication Chips Market include Qualcomm, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Robert Bosch, Denso, Huawei Technologies, Harman, and Continental. To solidify their presence, companies in the V2X Communication Chips Market are focusing on several core strategies. These include developing dual-mode chipsets that support both DSRC and cellular V2X standards to cater to varied global regulatory environments. Leaders are also prioritizing ultra-low-latency and power-efficient architectures to meet real-time safety demands and extend battery life in EV platforms. Strategic collaborations with automakers and network providers help align chip designs with vehicle development timelines and infrastructure readiness.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Communication

- 2.2.3 Connectivity

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing deployment of connected and autonomous vehicles

- 3.2.1.2 Government mandates road safety and ITS infrastructure

- 3.2.1.3 Transition toward C-V2X with 5G compatibility

- 3.2.1.4 OEM-semiconductor partnerships for scalability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High integration and testing costs

- 3.2.2.2 Fragmentation between DSRC and C-V2X standards

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of smart city infrastructure and 5G rollout

- 3.2.3.2 Integration with ADAS and autonomous driving systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Regional Infrastructure Readiness

- 3.12.1. 5 G network penetration

- 3.12.2 Smart city development status

- 3.12.3. Road infrastructure for V2 X testing

- 3.13 Benchmarking & KPIs

- 3.13.1 Performance metrics for chips (latency, range, reliability)

- 3.13.2 Benchmarking of key players

- 3.13.3 Industry standards and certifications

- 3.14 Market Adoption Scenarios

- 3.14.1 Short-term (1-3 years) adoption forecast

- 3.14.2 Mid-term (4-7 years) adoption forecast

- 3.14.3 Long-term (8-10 years) adoption forecast

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Communication, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Vehicle-to-Vehicle

- 5.3 Vehicle-to-Infrastructure

- 5.4 Vehicle-to-Pedestrian

- 5.5 Vehicle-to-Network

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 DSRC

- 6.3 C-V2X

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.1.1 Passenger Vehicles

- 7.1.1.1 Hatchback

- 7.1.1.2 Sedan

- 7.1.1.3 SUV

- 7.1.2 Commercial Vehicles

- 7.1.2.1 Light Commercial Vehicles (LCV)

- 7.1.2.2 Medium Commercial Vehicles (MCV)

- 7.1.2.3 Heavy Commercial Vehicles (HCV)

- 7.1.1 Passenger Vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Automated Driver Assistance

- 8.3 Traffic Management

- 8.4 Emergency Vehicle Notification

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Qualcomm

- 10.1.2 NXP Semiconductors

- 10.1.3 Huawei Technologies

- 10.1.4 Infineon Technologies

- 10.1.5 STMicroelectronics

- 10.1.6 Continental

- 10.1.7 Robert Bosch

- 10.1.8 Denso Corporation

- 10.1.9 Harman

- 10.1.10 Intel Corporation

- 10.2 Regional Players

- 10.2.1 Autotalks

- 10.2.2 Commsignia

- 10.2.3 Cohda Wireless

- 10.2.4 Savari

- 10.2.5 Panasonic Automotive

- 10.3 Emerging Players / Disruptors

- 10.3.1 Veoneer

- 10.3.2 Excelfore

- 10.3.3 Visteon Corporation

- 10.3.4 NXP Labs Startup Ventures

- 10.3.5 KT Corporation Automotive Solutions