|

시장보고서

상품코드

1858968

폐동맥 고혈압 시장 : 시장 기회 및 촉진요인, 산업 동향 분석, 예측(2025-2034년)Pulmonary Arterial Hypertension Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

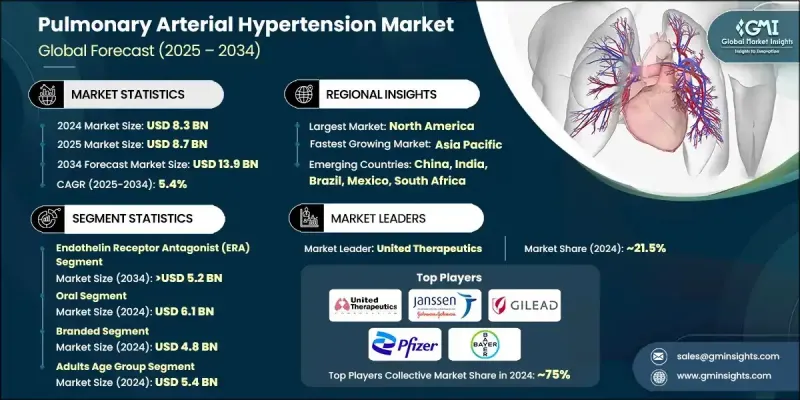

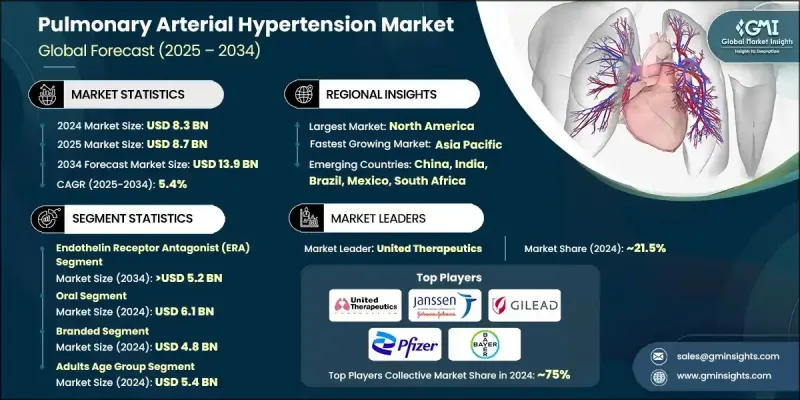

세계의 폐동맥 고혈압 시장은 2024년 83억 달러로 평가되었고, CAGR 5.4%로 성장할 전망이며, 2034년에는 139억 달러에 이를 것으로 추정됩니다.

시장 수요 증가는 세계적인 PAH 증례 수 증가, 약물 요법의 진보, FDA 및 EMA 등 규제 기관에 의한 새로운 PAH 치료법의 개발 지원에 대한 지속적인 노력에 기인하고 있습니다. 진단 기술 및 바이오마커 스크리닝 방법이 개선됨에 따라 PAH의 조기 발견이 더욱 효과적이 되어 질병 관리 개선에 기여하고 있습니다. 특히 아시아태평양, 라틴아메리카 등 신흥 지역에서 건강 관리 인프라에 대한 투자 확대도 PAH 치료에 대한 접근성 확대에 중요한 역할을 하고 있습니다. 중국, 인도, 브라질 등 국가에서는 의료제도의 개선과 정부 주도의 계발활동에 의해 치료제의 입수성이 향상되고 있습니다. 바이오시밀러가 시장에 진입함에 따라 치료비가 보다 저렴해지고 개발도상 지역에서의 접근성이 더욱 향상되고 있습니다. 제약사는 또한 전략적 합병, 인수, 파트너십을 활용하여 포트폴리오를 다양화하고 PAH 치료제 개발의 혁신을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 83억 달러 |

| 예측 금액 | 139억 달러 |

| CAGR | 5.4% |

엔도세린 수용체 길항제(ERA) 부문은 2024년에 37.3%의 점유율을 차지하였고, 2034년에는 CAGR 5.4%로 성장하여 52억 달러에 달할 것으로 예측됩니다. 보센탄, 암브리센탄, 마키텐탄 등의 ERA는 PAH의 발병에 관여하는 주요 혈관 수축 인자인 엔도세린-1을 억제합니다. 이 약물은 폐 혈관 저항을 줄이고 운동 능력을 향상시키는 데 도움이 되며 장기적인 질병 관리를 위한 일반적인 옵션이 되었습니다.

2024년 경구 약물 부문은 61억 달러를 매출하여 복용 편의성으로 많은 환자들에게 선호되고 있으며, 빈번한 통원 및 복잡한 의료기기의 필요성을 줄였습니다. 경구 요법은 부작용이 적고 안전성 프로파일이 우수하기 때문에 특히 다른 건강 상태를 가진 환자의 장기 사용에 적합합니다.

미국의 폐동맥 고혈압 2024년 시장 규모는 40억 달러로, 특히 노인층이나 COPD 등 다른 합병증을 가진 환자들 사이에서 유병률이 상승하고 있는 것이 배경에 있습니다. 심 초음파 검사 및 바이오마커 검사 등의 고급 진단 방법으로 조기 발견이 용이해진 것이 치료를 요구하는 환자 증가에 기여하여 PAH 치료제 수요를 촉진하고 있습니다. 미국에 본사를 둔 기업은 PAH 연구의 최전선에 있으며 치료 분야의 혁신을 추진하고 있습니다.

세계의 폐동맥 고혈압 시장에서 활약하고 있는 유명한 기업으로는 Merck KGaA, Bayer, Gilead Sciences, GlaxoSmithKline(GSK), Pfizer, Jansen Pharmaceuticals(Johnson & Johnson), United Therapeutics, Gmax Biopharm, Resverlogix, Liquidia Technologies, Gossamer Bio, Galectin Therapeutics, Novartis 등이 있습니다. 폐동맥 고혈압 시장에서의 지위를 강화하기 위해 기업은 새로운 치료법의 연구 개발을 통해 제품 포트폴리오를 확대하고 환자의 치료에 대한 접근성을 개선하는 데 주력하고 있습니다. 많은 기업들은 혁신적인 후기 자산을 얻기 위해 소규모 생명 공학 기업과의 제휴, 합병 및 인수에 투자하고 있습니다. 기업은 특히 현지 생산 시설을 설립함으로써 보다 저렴하고 이용 가능한 치료를 실현하기 위해 신흥 시장에서 전략적 지역 투자를 선호합니다. 이러한 접근법은 비용 절감뿐만 아니라 개발 도상 시장에서 가격 설정의 장벽을 낮추는 데 도움이 되는 바이오 시밀러 증가 추세에도 부합합니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- PAH 및 관련 질환의 유병률 상승

- 약물 요법의 진보

- 맞춤형 치료로의 이동 증가

- 개발 도상국의 헬스케어 인프라 개선

- 업계의 잠재적 위험 및 과제

- 높은 치료비

- 전문가 액세스 제한

- 규제 상의 과제

- 시장 기회

- 병용 요법의 이용 확대

- 유전자 치료 및 재생 의료의 융합 진행

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 북미

- 기술 및 정세

- 현재의 기술 동향

- 신흥 기술

- 향후 시장 동향

- 가격 분석

- 임상시험 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력

- 신제품 발표

- 확장 계획

제5장 시장 추계 및 예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 프로스타사이클린 및 프로스타사이클린 유사체

- 가용성 구아닐산시클라제(SGC) 자극제

- 엔도세린 수용체 길항제(ERA)

- 포스포디에스테라아제 5(PDE-5)

- 혈관확장제

- 약제 클래스별

제6장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 경구

- 정맥내 투여

- 흡입

제7장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 브랜드

- 제네릭 의약품

제8장 시장 추계 및 예측 : 연령층별(2021-2034년)

- 주요 동향

- 소아

- 성인용

- 고령자

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 전문 클리닉

- 기타 최종 사용

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Bayer

- F. Hoffmann La Roche

- GlaxoSmithKline(GSK)

- Gilead Sciences

- Gmax Biopharm

- Gossamer Bio

- Galectin Therapeutics

- Janssen Pharmaceuticals(Johnson & Johnson)

- Liquidia Technologies

- Merck KGaA

- Novartis

- Pfizer

- Resverlogix

- United Therapeutics

The Global Pulmonary Arterial Hypertension Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 13.9 billion by 2034.

The rise in market demand is attributed to the increasing number of PAH cases worldwide, advancements in drug therapies, and ongoing efforts by regulatory agencies such as the FDA and EMA to support the development of new PAH treatments. As diagnostic technologies and biomarker screening methods improve, early detection of PAH has become more effective, contributing to better management of the disease. The growing investments in healthcare infrastructure, particularly in emerging regions like Asia-Pacific and Latin America, have also played a key role in expanding access to PAH treatments. Countries such as China, India, and Brazil are seeing enhanced availability of therapies due to improvements in healthcare systems and government-driven awareness initiatives. Biosimilars entering the market are helping to make treatments more affordable, further boosting accessibility in developing regions. Pharmaceutical companies are also leveraging strategic mergers, acquisitions, and partnerships to diversify their portfolios and accelerate innovation in PAH drug development.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $13.9 Billion |

| CAGR | 5.4% |

The endothelin receptor antagonist (ERA) segment held a 37.3% share in 2024, and it is projected to reach USD 5.2 billion by 2034, growing at a CAGR of 5.4%. ERAs, such as bosentan, ambrisentan, and macitentan, block endothelin-1, a key vasoconstrictor involved in the development of PAH. These drugs help reduce pulmonary vascular resistance and improve exercise capacity, making them a common choice for long-term disease management.

In 2024, the oral drug segment generated USD 6.1 billion, and it is preferred by many patients due to the convenience of administration, reducing the need for frequent hospital visits and complex medical equipment. Oral therapies are associated with fewer side effects and better safety profiles, which make them suitable for long-term use, especially among patients with other health conditions.

U.S. Pulmonary Arterial Hypertension Market was valued at USD 4 billion in 2024, driven by the rising prevalence of the disease, particularly among older populations and individuals with other comorbidities such as COPD. Early detection facilitated by advanced diagnostic methods, including echocardiography and biomarker testing, is contributing to a larger pool of patients seeking treatment, fueling demand for PAH therapies. U.S.-based companies are at the forefront of PAH research, driving innovation in the treatment space.

Prominent companies active in the Global Pulmonary Arterial Hypertension Market include Merck KGaA, Bayer, Gilead Sciences, GlaxoSmithKline (GSK), Pfizer, Janssen Pharmaceuticals (Johnson & Johnson), United Therapeutics, Gmax Biopharm, Resverlogix, Liquidia Technologies, Gossamer Bio, Galectin Therapeutics, and Novartis. To strengthen their position in the Pulmonary Arterial Hypertension Market, companies are focusing on expanding their product portfolios through research and development of new therapies and improving patient access to treatments. Many are investing in partnerships, mergers, and acquisitions, often with smaller biotech firms, to acquire innovative and late-stage assets. Companies are also prioritizing strategic regional investments in emerging markets to make treatments more affordable and available, especially by establishing local production facilities. This approach not only reduces costs but also aligns with the growing trend of biosimilars, which help lower pricing barriers in developing markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Route of administration trends

- 2.2.4 Type trends

- 2.2.5 Age group trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of PAH and related conditions

- 3.2.1.2 Advancement in drug therapies

- 3.2.1.3 Increasing shift toward personalized treatment

- 3.2.1.4 Improved healthcare infrastructure in developing countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Limited access to specialists

- 3.2.2.3 Regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Growing usage of combination therapy

- 3.2.3.2 Rising integration of gene therapy and regenerative medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Clinical trial analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Prostacyclin and prostacyclin analogs

- 5.3 Soluble guanylate cyclase (SGC) stimulators

- 5.4 Endothelin receptor antagonist (ERA)

- 5.5 Phosphodiesterase 5 (PDE-5)

- 5.6 Vasodilators

- 5.7 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Intravenous

- 6.4 Inhalation

Chapter 7 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generics

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pediatrics

- 8.3 Adult

- 8.4 Geriatrics

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Specialty clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Bayer

- 11.2 F. Hoffmann La Roche

- 11.3 GlaxoSmithKline (GSK)

- 11.4 Gilead Sciences

- 11.5 Gmax Biopharm

- 11.6 Gossamer Bio

- 11.7 Galectin Therapeutics

- 11.8 Janssen Pharmaceuticals (Johnson & Johnson)

- 11.9 Liquidia Technologies

- 11.10 Merck KGaA

- 11.11 Novartis

- 11.12 Pfizer

- 11.13 Resverlogix

- 11.14 United Therapeutics