|

시장보고서

상품코드

1858983

뇌자도 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Magnetoencephalography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

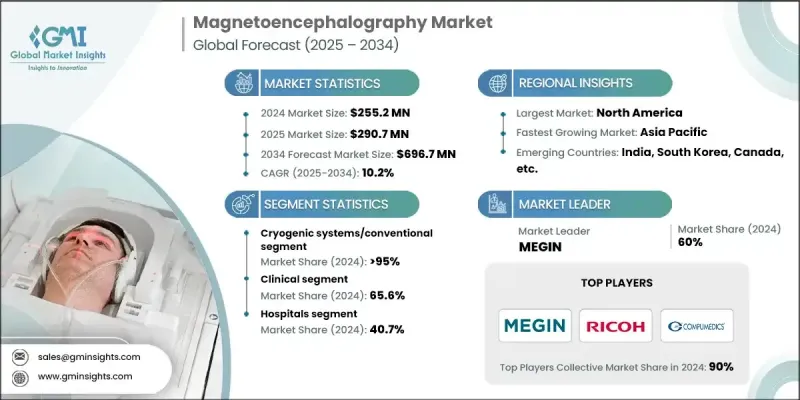

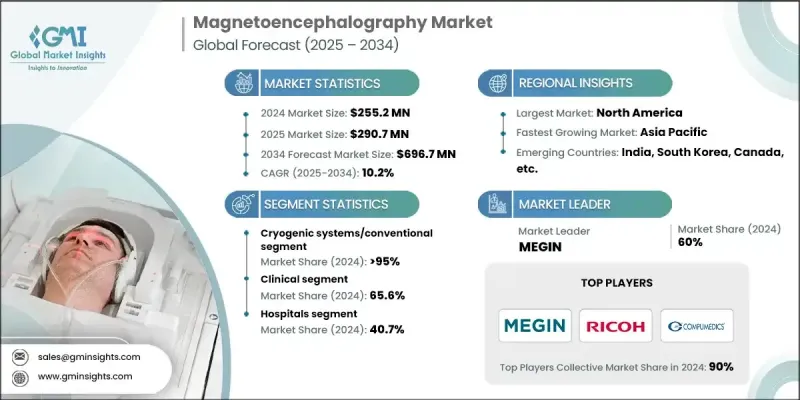

세계의 뇌자도 시장은 2024년에 2억 5,520만 달러로 평가되었고 CAGR 10.2%를 나타내 2034년에는 6억 9,670만 달러에 달할 것으로 예측되고 있습니다.

뇌자도(MEG) 수요는 신경질환 발생률 증가, 인구 고령화, 고급 진단 도구에 대한 의존도 증가로 가속화되고 있습니다. 임상기관이나 연구기관에서는 신경학적 평가의 정확성과 속도를 높이기 위해 MEG의 도입이 진행되고 있습니다. 뇌 활동을 실시간으로 추적할 수 있는 이 기술은 간질, 알츠하이머병, 파킨슨병 등의 진단 및 관리에 필수적입니다. 임상 사용 외에도 MEG 시스템은 뇌 기능 연구, 정신 의학적 평가, 신경 발달 연구 등에도 널리 적용됩니다. 기술 진보와 뇌 네트워크 연결에 대한 깊은 이해는 건강 관리 생태계 전체의 혁신과 통합을 지속적으로 촉진하고 있습니다. 특히 선진지역에서는 헬스케어 인프라가 정비되어 신경과학에 대한 대처에 대한 자금 지원이 충실하기 때문에 채용이 진행되고 있습니다. 제조업체 각사는 특히 신흥 시장에서 유통 전략의 강화와 저비용 모델을 통해 MEG 시스템에 대한 액세스 확대를 추진하고 있습니다. 개인화 치료 및 조기 진단에 대한 동향 증가는 뇌자도 시스템의 세계 장기 시장 수요를 더욱 촉진할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 2억 5,520만 달러 |

| 예측 금액 | 6억 9,670만 달러 |

| CAGR | 10.2% |

OPM 시스템 분야는 2034년까지 연평균 복합 성장률(CAGR) 24.9%를 나타내 뉴로 이미징의 혁신적인 진보로서의 지위를 확립합니다. 이 시스템은 실온에서 효율적으로 작동하는 광 펌프 자력계를 사용하여 제작되었으며 복잡한 극저온 구성 요소가 필요하지 않습니다. 컴팩트한 웨어러블 포맷으로 센서를 두피에 직접 배치할 수 있어 공간 분해능이 향상되고 자연스러운 작동 중에 데이터를 검색할 수 있습니다. OPM 기반 MEG 시스템은 유연성, 운영 비용이 낮고 실제 환경에 적응하기 때문에 소아용 및 외래 모니터링에 특히 매력적입니다. 그 확장성과 휴대성은 임상 현장과 신경과학 연구센터 모두에서 계속 지원됩니다.

2024년 임상분야 점유율은 65.6%였습니다. 신경병증을 앓고 있는 환자 수 증가와 조기 진단에 대한 중점화는 이 부문의 이점에 기여합니다. MEG는 비정상적인 뇌 활동을 정확하게 식별함으로써 수술 전 매핑과 질병 관리에 중요한 역할을 합니다. 비침습적이고 고해상도의 능력은 정확한 매핑이 수술 계획과 환자 결과에 매우 중요한 간질, 종양 및 퇴행성 신경 질환의 치료에 특히 유용합니다.

북미의 뇌자도 시장은 2024년 39.5%의 점유율을 차지했습니다. 이 지역은 의학 연구의 견고한 기반, 광범위한 건강 관리 접근, 뇌 관련 질환으로 진단되는 환자 수 증가 등의 이점을 누리고 있습니다. MEG의 조기 임상 도입과 병원 진료에의 통합은 진단에의 응용 확대를 도와줍니다. 지역 정부는 신경과학 프로젝트에 자금을 제공하고 뇌 매핑 연구 이니셔티브를 지원함으로써 중요한 역할을 수행하고 있습니다. 이러한 요인들로 인해 북미는 MEG 시스템을 이용한 기술 개발과 임상 결과 모두에서 전면 러너로 자리매김하고 있습니다.

세계의 뇌자도 시장에서 활동하고 있는 주요 기업으로는 FieldLine Inc., Ricoh, Buscar Magnetics Limited, Compumedics Limited, MAG4Health, MEGIN, CTF MEG NEURO INNOVATIONS, INC. 등이 있습니다. 뇌자도 분야의 기업은 연구개발에 대한 전략적 투자와 세계 전개를 통해 시장에서의 지위를 강화하고 있습니다. 혁신은 이동성과 접근성을 향상시키는 OPM 기반 솔루션과 같은 차세대 MEG 시스템에 중점을 두고 중심을 유지하고 있습니다. 기업은 신흥 시장에서의 설치와 서비스 인프라를 개선함으로써 지리적으로 확대되고 있습니다. 연구기관과 병원과의 협력관계는 임상 검증 및 제품 채용을 가속화하는 데 도움이 됩니다. 또한 시스템 통합을 간소화하고 운영 복잡성을 줄이기 위해 노력하고 있으며, MEG를 일상적인 임상 사용에 보다 현실적으로 만들고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 신경질환의 유병률 증가

- 뇌자도 분야에서의 급속한 기술 진보

- 임상 진단 및 연구에서 애플리케이션의 성장

- 업계의 잠재적 위험 및 과제

- 대체 신경 영상 기술의 이용 가능성

- 뇌자도 시스템의 고비용

- 기회

- 휴대용 및 웨어러블 MEG 시스템

- AI 통합 및 자동 분석

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 기술 로드맵과 혁신의 전망

- SQUID 기술의 진화

- OPM 기술의 진보

- 양자센서 개발

- AI/ML 통합 스케줄

- 가격 분석, 지역별(2024년)

- fMRI와 EEG에 대한 MEG의 장점

- 파이프라인 분석

- 세계의 MEG 설치수, 지역별 및 국가별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 아시아태평양

- 중국

- 일본

- 북미

- 브랜드 분석

- 상환 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

- 주요 발전

- 합병 및 인수

- 파트너십

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 극저온 시스템/기존

- OPM 시스템

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 임상

- 간질

- 자폐증

- 치매

- 뇌졸중

- 외상성 뇌손상(TBI)

- 기타 용도

- 연구

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 영상의학 센터

- 학술 및 연구 기관

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 아시아태평양

- 중국

- 일본

- 세계 기타 지역(RoW)

제9장 기업 프로파일

- Cerca Magnetics Limited

- Compumedics Limited

- CTF MEG NEURO INNOVATIONS, INC.

- FieldLine Inc.

- MAG4Health

- MEGIN

- Ricoh

The Global Magnetoencephalography Market was valued at USD 255.2 million in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 696.7 million by 2034.

The demand for magnetoencephalography (MEG) is accelerating due to rising incidences of neurological disorders, an aging population, and increased reliance on advanced diagnostic tools. Clinical and research institutions are increasingly adopting MEG to enhance the precision and speed of neurological assessments. The technology's ability to deliver real-time tracking of brain activity is proving vital in the diagnosis and management of conditions like epilepsy, Alzheimer's disease, and Parkinson's disease. In addition to clinical use, MEG systems are seeing broader application in brain function research, psychiatric evaluation, and neurodevelopmental studies. Technological progress and a deeper understanding of brain network connectivity continue to drive innovation and integration across healthcare ecosystems. Strong adoption is especially noted in developed regions due to improved healthcare infrastructure and supportive funding for neuroscience initiatives. Manufacturers are working on expanding access to MEG systems through enhanced distribution strategies and lower-cost models, particularly in emerging markets. The rising trend toward personalized treatment and early-stage diagnosis is further expected to fuel long-term market demand for magnetoencephalography systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $255.2 Million |

| Forecast Value | $696.7 Million |

| CAGR | 10.2% |

The OPM systems segment will grow at a CAGR of 24.9% through 2034, establishing itself as a transformative advancement in neuroimaging. These systems are built using optically pumped magnetometers, which operate efficiently at room temperature, eliminating the need for complex cryogenic components. Their compact, wearable format allows sensors to be positioned directly on the scalp, enhancing spatial resolution and enabling data capture during natural movements. The flexibility, lower operational costs, and real-world adaptability of OPM-based MEG systems have made them especially attractive for pediatric use and ambulatory monitoring. Their scalability and portability continue to gain traction across both clinical settings and neuroscience research centers.

In 2024, the clinical segment held a 65.6% share. The growing patient base suffering from neurological disorders, combined with increasing emphasis on early-stage diagnostics, is contributing to the segment's dominance. MEG plays a key role in presurgical mapping and disease management by precisely localizing abnormal brain activity. Its non-invasive and high-resolution capability makes it particularly useful in treating epilepsy, tumors, and degenerative neurological diseases, where accurate mapping is crucial for surgical planning and patient outcomes.

North America Magnetoencephalography Market held 39.5% share in 2024. The region benefits from a strong foundation in medical research, widespread healthcare access, and increasing patient numbers diagnosed with brain-related conditions. Early clinical adoption and integration of MEG into hospital practices have helped expand its application in diagnostics. Regional governments have also played a significant role by funding neuroscience projects and supporting brain mapping research initiatives. These factors have positioned North America as a frontrunner in both technology deployment and clinical outcomes using MEG systems.

Key companies active in the Global Magnetoencephalography Market include FieldLine Inc., Ricoh, Cerca Magnetics Limited, Compumedics Limited, MAG4Health, MEGIN, and CTF MEG NEURO INNOVATIONS, INC. Companies in the magnetoencephalography space are strengthening their market positions through strategic investments in R&D and global expansion. Innovation remains central, with a focus on next-generation MEG systems like OPM-based solutions that enhance mobility and accessibility. Firms are expanding geographically by targeting installations in emerging markets and improving service infrastructure. Collaborations with research institutions and hospitals are helping accelerate clinical validation and product adoption. Additionally, efforts are being made to simplify system integration and reduce operational complexity, making MEG more viable for routine clinical use.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological disorders

- 3.2.1.2 Rapid technology advancements in the field of magnetoencephalography

- 3.2.1.3 Growing applications in clinical diagnosis and research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative neuroimaging technologies

- 3.2.2.2 High cost of magnetoencephalography systems

- 3.2.3 Opportunities

- 3.2.3.1 Portable & wearable MEG systems

- 3.2.3.2 AI integration & automated analysis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology roadmap & innovation landscape

- 3.5.1 SQUID technology evolution

- 3.5.2 OPM technology advancement

- 3.5.3 Quantum sensor development

- 3.5.4 AI/ML integration timeline

- 3.6 Pricing analysis, by region, 2024

- 3.7 Advantages of MEG over fMRI and EEG

- 3.8 Pipeline analysis

- 3.9 Worldwide MEG installations, by region and country

- 3.9.1 North America

- 3.9.1.1 U.S.

- 3.9.1.2 Canada

- 3.9.2 Europe

- 3.9.2.1 Germany

- 3.9.2.2 UK

- 3.9.2.3 France

- 3.9.3 Asia Pacific

- 3.9.3.1 China

- 3.9.3.2 Japan

- 3.9.1 North America

- 3.10 Brand analysis

- 3.11 Reimbursement scenario

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Future market trends

- 3.15 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Cryogenic systems/Conventional

- 5.3 OPM systems

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical

- 6.2.1 Epilepsy

- 6.2.2 Autism

- 6.2.3 Dementia

- 6.2.4 Stroke

- 6.2.5 Traumatic brain injury (TBI)

- 6.2.6 Other applications

- 6.3 Research

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Imaging centres

- 7.4 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.5 Rest of the world (RoW)

Chapter 9 Company Profiles

- 9.1 Cerca Magnetics Limited

- 9.2 Compumedics Limited

- 9.3 CTF MEG NEURO INNOVATIONS, INC.

- 9.4 FieldLine Inc.

- 9.5 MAG4Health

- 9.6 MEGIN

- 9.7 Ricoh