|

시장보고서

상품코드

1859014

커넥티드 헬스케어 디바이스 시장 기회와 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Connected Healthcare Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

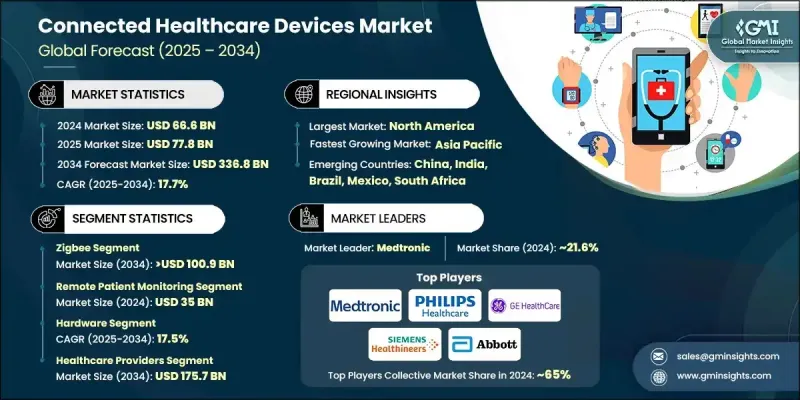

세계의 커넥티드 헬스케어 디바이스 시장은 2024년에 666억 달러로 평가되었고 CAGR 17.7%를 나타내 2034년에는 3,368억 달러에 이를 것으로 추정되고 있습니다.

고혈압, 당뇨병, 심혈관 장애와 같은 만성 건강 상태의 꾸준한 증가는이 성장의 주요 원동력 중 하나입니다. 이러한 장기적인 질병에는 지속적인 모니터링이 필요하며 ECG 패치, 포도당 모니터, 스마트 혈압 추적기 등의 연결된 의료기기는 이를 제공하기에 적합합니다. IoT, AI, 센서 기술의 발전으로 이러한 장비의 효율, 정확성 및 통합 능력이 향상되었습니다. 게다가, 원격 의료의 급속한 보급으로, 특히 임상 서비스에 대한 접근이 제한된 원격지에서 일상 관리에서 연결 장치의 역할이 확대되고 있습니다. 이러한 장비를 통해 의료 서비스 제공업체는 환자의 생체를 실시간으로 모니터링할 수 있어 결과를 개선하고 입원을 줄일 수 있습니다. 디지털 인프라의 개선과 데이터 중심의 건강 관리 제공에 대한 증가가 결합되어, 최신 케어 제공 모델에 따른 커넥티드 의료 기술에 대한 수요가 계속 증가하고 있습니다. 커넥티드 헬스케어 디바이스는 기존의 툴과 달리 디지털 네트워크상에서 환자 데이터를 안전하게 공유 및 수신할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 666억 달러 |

| 예측 금액 | 3,368억 달러 |

| CAGR | 17.7% |

Zigbee 프로토콜 분야는 2024년에 31%의 점유율을 확보했으며 2034년에는 CAGR 17.3%로 1,009억 달러에 이를 것으로 예측됩니다. Zigbee의 에너지 효율적인 설계는 웨어러블 모니터, 센서, 진단 도구와 같은 장비의 배터리 수명 연장을 지원합니다. 가정이나 클리닉에서 사용되는 저전력으로 항상 켜진 의료기기에 적합하기 때문에 특히 장기간 지속적인 추적이 필요한 환자에게 선호되는 기술입니다. 이렇게 하면 컴플라이언스 향상, 유지 보수 완화 및 원활한 모니터링이 가능합니다.

원격 환자 모니터링(RPM) 부문은 2024년 350억 달러를 창출했습니다. 바이오센서, 웨어러블, 모바일 통합의 지속적인 혁신으로 RPM을 보다 효율적이고 널리 사용할 수 있게 되었습니다. 최신 시스템은 현재 여러 바이탈 모니터링을 지원하고 클라우드 기반 플랫폼을 통해 실시간 인사이트를 제공합니다. 이러한 개발은 임상적 의사결정과 환자의 참여를 강화하고 이 분야의 호조 시장 실적을 이어가고 있습니다.

북미의 커넥티드 헬스케어 디바이스 2024년 점유율은 51.4%로 디지털 헬스 기술의 세계적인 보급을 견인했습니다. 이 지역의 건강 관리 시스템은 만성 질환 관리 및 실시간 진단을 지원하는 연결된 의료 솔루션에 대한 의존도를 높이고 있습니다. 의료 IT 인프라에 대한 왕성한 투자와 모바일 헬스 툴의 인기가 높아짐에 따라 상호 운용성과 데이터 공유를 확대할 수 있어 의료 제공업체는 적시에 원격 관리를 대규모로 제공할 수 있습니다.

세계의 커넥티드 헬스케어 디바이스 시장에서 활약하는 주요 기업은 Vivify Health, Honeywell International, Medtronic, Siemens Healthineers, Dexcom, Fitbit(Google), Abbott Laboratories, Omron Corporation, Stanley Healthcare, CareCloud, Garmin, NXP Semiconductors Healthcare, AliveCor 등 입니다. 선도 기업은 지위를 확보하기 위해 광범위한 임상 요구에 대응하는 AI 대응 디바이스 및 센서 통합 디바이스의 제품 라인을 적극적으로 확대하고 있습니다. 각 회사는 연구 개발에 투자하고 배터리 수명과 안전한 데이터 전송을 강화한 가볍고 휴대가능한 사용자 친화적인 솔루션을 개발하고 있습니다. 병원, 의료기술 기업, 보험사와의 전략적 파트너십을 통해 기존 임상 워크플로우에 원활하게 통합할 수 있습니다. 각 회사는 또한 신흥 시장에 대응하고 접근성을 높이기 위해 세계 공급망을 강화하고 지역 판매망을 확립합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 웨어러블 기술의 채용 증가

- 스마트폰의 보급 확대

- m건강 앱 확대

- 개인화 건강 관리 수요 증가

- 업계의 잠재적 위험 및 과제

- 데이터 보안 및 프라이버시에 대한 우려

- 기기의 신뢰성과 정밀도

- 시장 기회

- 재택의료와 예방의료에 대한 수요 증가

- 커넥티드 디바이스와 AI, 클라우드 플랫폼, 엣지 컴퓨팅의 융합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 북미

- 기술·정세

- 현재의 기술 동향

- 신흥기술

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 제휴와 협력

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- Wi-Fi

- 블루투스 저에너지(BLE)

- 근거리 무선 통신(NFC)

- Zigbee

- 셀룰러

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 원격 환자 모니터링

- 임상 진단

- 치료

- 기타 용도

제7장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- 웨어러블 건강 기기

- 이식형 커넥티드 디바이스

- 원격 환자 모니터링 기기

- 기타 커넥티드 헬스케어 디바이스

- 소프트웨어

- 서비스

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 의료 제공자

- 병원

- 진료소

- 원격의료 플랫폼

- 지불 기관

- 보험사

- 정부 의료 프로그램

- 환자

- 기타 최종 사용

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Abbott Laboratories

- AliveCor

- Allscripts

- CareCloud

- Dexcom

- Fitbit(Google)

- Garmin

- GE Healthcare

- Honeywell International

- Koninklijke Philips

- Medtronic

- NXP Semiconductors

- Omron Corporation

- Siemens Healthineers

- Stanley Healthcare

- Vivify Health

The Global Connected Healthcare Devices Market was valued at USD 66.6 billion in 2024 and is estimated to grow at a CAGR of 17.7% to reach USD 336.8 billion by 2034.

The steady rise in chronic health conditions such as hypertension, diabetes, and cardiovascular disorders is one of the primary drivers behind this growth. These long-term diseases demand ongoing monitoring, which connected medical devices like ECG patches, glucose monitors, and smart blood pressure trackers are uniquely suited to provide. The advancement of IoT, AI, and sensor technologies has enhanced these devices' efficiency, accuracy, and integration capabilities. Additionally, the rapid adoption of telehealth has expanded the role of connected devices in routine care, particularly in remote regions where access to clinical services is limited. These devices allow healthcare providers to monitor patient vitals in real time, improving outcomes and reducing hospitalizations. The combination of improved digital infrastructure and the growing push toward data-centric healthcare delivery continues to fuel demand for connected medical technologies that align with modern care delivery models. Connected healthcare devices, unlike traditional tools, can share and receive patient data securely over digital networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $66.6 Billion |

| Forecast Value | $336.8 Billion |

| CAGR | 17.7% |

The Zigbee protocol segment secured a 31% share in 2024 and is forecasted to reach USD 100.9 billion by 2034, with a CAGR of 17.3%. Zigbee's energy-efficient design supports longer battery life for devices like wearable monitors, sensors, and diagnostic tools. Its suitability for low-power, always-on medical devices used in homes and clinics makes it a preferred technology, especially for patients requiring continuous tracking over extended periods. This enables better compliance, reduced maintenance, and seamless monitoring.

The remote patient monitoring (RPM) segment generated USD 35 billion in 2024. Continuous innovation in biosensors, wearables, and mobile integration has made RPM more efficient and widely accessible. Modern systems now support multi-vital monitoring and provide real-time insights through cloud-based platforms. These developments enhance clinical decision-making and patient involvement, which continues to drive the segment's strong market performance.

North America Connected Healthcare Devices Market accounted for a 51.4% share in 2024, leading global adoption of digital health technologies. The region's healthcare system increasingly depends on connected medical solutions to support chronic disease management and real-time diagnostics. Strong investment in health IT infrastructure and the growing popularity of mobile health tools enable greater interoperability and data sharing, allowing providers to offer timely, remote care at scale.

Key companies active in the Global Connected Healthcare Devices Market include Vivify Health, Honeywell International, Medtronic, Siemens Healthineers, Dexcom, Fitbit (Google), Abbott Laboratories, Omron Corporation, Stanley Healthcare, CareCloud, Garmin, NXP Semiconductors, Allscripts, Koninklijke Philips, GE Healthcare, and AliveCor. To secure their positions, leading companies are actively expanding their product lines with AI-enabled and sensor-integrated devices to address a wide range of clinical needs. Firms are investing in R&D to create lightweight, portable, and user-friendly solutions with enhanced battery life and secure data transmission. Strategic partnerships with hospitals, health tech firms, and insurers allow seamless integration into existing clinical workflows. Companies are also enhancing their global supply chains and establishing regional distribution networks to serve emerging markets and increase accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 Component trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of wearable technology

- 3.2.1.2 Increased smartphone penetration

- 3.2.1.3 Expansion of mHealth apps

- 3.2.1.4 Growing demand for personalized healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy concerns

- 3.2.2.2 Reliability and accuracy of devices

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for home-based and preventive care

- 3.2.3.2 Convergence of connected devices with AI, cloud platforms, and edge computing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wi-Fi

- 5.3 Bluetooth Low Energy (BLE)

- 5.4 Near-field Communication (NFC)

- 5.5 Zigbee

- 5.6 Cellular

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Remote patient monitoring

- 6.3 Clinical diagnostics

- 6.4 Therapeutics

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hardware

- 7.2.1 Wearable health device

- 7.2.2 Implantable connected devices

- 7.2.3 Remote patient monitoring devices

- 7.2.4 Other connected healthcare devices

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Healthcare providers

- 8.2.1 Hospitals

- 8.2.2 Clinics

- 8.2.3 Telehealth platforms

- 8.3 Payers

- 8.3.1 Insurance companies

- 8.3.2 Government health programs

- 8.4 Patients

- 8.5 Other End uses

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 AliveCor

- 10.3 Allscripts

- 10.4 CareCloud

- 10.5 Dexcom

- 10.6 Fitbit (Google)

- 10.7 Garmin

- 10.8 GE Healthcare

- 10.9 Honeywell International

- 10.10 Koninklijke Philips

- 10.11 Medtronic

- 10.12 NXP Semiconductors

- 10.13 Omron Corporation

- 10.14 Siemens Healthineers

- 10.15 Stanley Healthcare

- 10.16 Vivify Health