|

시장보고서

상품코드

1871084

재조합 단백질 식품 원료 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Recombinant Protein Food Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

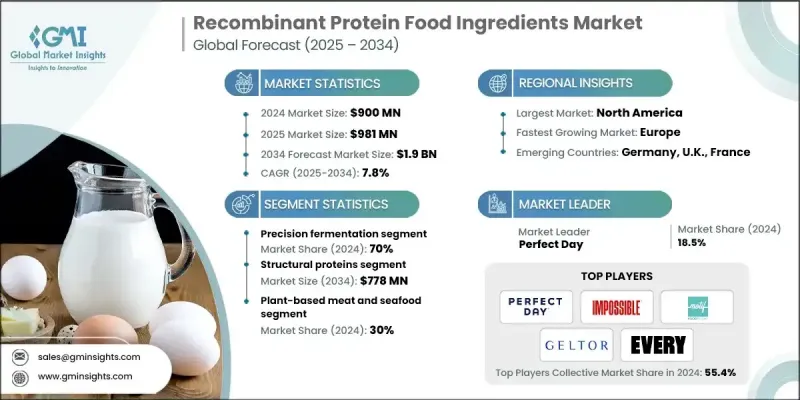

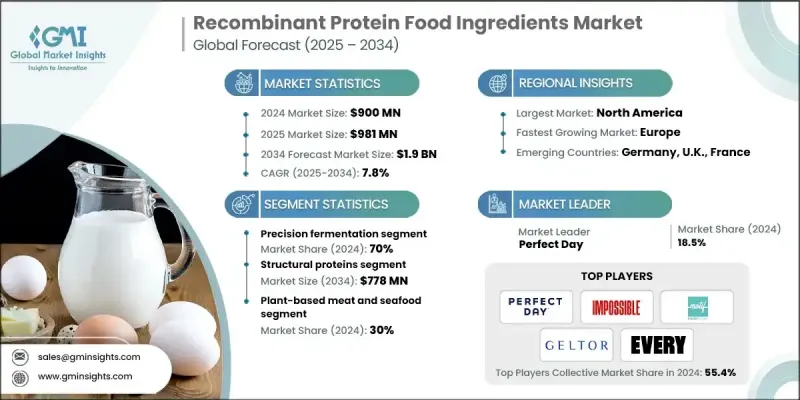

세계의 재조합 단백질 식품 원료 시장은 2024년에 9억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 7.8%를 나타내 19억 달러에 이를 것으로 예측됩니다.

생명공학의 진보와 지속가능하고 기능성 식품을 요구하는 소비자의 선호도가 식품 혁신의 정세를 바꾸고 있기 때문에 이 업계는 급속히 확대되고 있습니다. 만성 질환의 발병률 증가와 개인화된 영양에 대한 관심 증가는 시장 수요를 견인하는 주요 요인입니다. 제조업체 각사는 합성 생물학, 균주 설계, 정밀 발효 기술의 능력을 강화하고, 동물성 단백질과 동등한 식감, 영양 프로파일, 관능 특성을 재현하는 단백질의 개발을 진행하고 있습니다. 이 진전에 의해 대규모 생산이 가능해 재조합 단백질은 실험실 단계에서 유제품, 육제품, 음료 용도의 상업 원료로 변모를 이루고 있습니다. 지속가능성은 이 진화의 핵심이 되고, 생산자는 순환형 저탄소 제조 공정에 주력하고 있습니다. 가스 발효나 농업 제품별 이용 등의 신기술에 의해 탄소 강도가 저감되어, 카본 네거티브(탄소 배출량 마이너스)인 단백질 생산의 가능성이 넓어지고 있습니다. 이러한 지속 가능한 개발은 세계의 탈탄소화 및 ESG 목표와 일치하고 환경 책임을 중시하는 투자자의 관심을 모으고 있습니다. 환경을 배려한 생산방법에 대한 주목이 높아짐에 따라 소비자의 신뢰 강화와 세계적인 규제 당국의 승인 획득에도 이어지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 달러 |

| 예측 금액 | 19억 달러 |

| CAGR | 7.8% |

정밀 발효 부문은 2024년에 70%의 점유율을 차지했습니다. 이 기술은 유전자 변형 미생물을 사용하여 동물성 단백질에 매우 가까운 고순도의 균질한 단백질을 생산합니다. 확장성, 규제 준수, 비용 효율성이 높아 업계 표준이 되어 유제품, 계란, 고기 대체품의 대량 생산을 지원하고 있습니다.

구조 단백질 부문은 2024년에 40%의 점유율을 차지했으며, 2034년까지 7억 7,800만 달러에 이를 것으로 예측됩니다. 이 단백질은 특히 식물 유래 고기, 치즈, 베이커리 제품에서 식품 배합에서 구조, 안정성 및 결합 특성을 제공하는 데 중요한 역할을합니다. 산업 파트너십은 생산 공정를 가속화하고 대체 식품 부문 전체에서 사용되는 주요 단백질 원료의 대규모 제조를 가능하게 합니다.

북미의 재조합 단백질 식품 원료 시장은 2024년 3억 7,900만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8%를 나타낼 것으로 예측됩니다. 이 지역은 견고한 생명공학 생태계, GRAS(일반적으로 안전한 것으로 인정됨) 프레임워크 하에서 FDA의 유리한 규제 경로, 벤처 캐피탈 투자 증가, 지속 가능한 단백질 대체물에 대한 소비자 의식 증가 등의 혜택을 받고 있습니다. 또한 공동 이니셔티브와 자금 조달 프로그램은 북미 전역에서 재조합 단백질 원료의 생산과 상업화를 지속적으로 강화하고 있습니다.

세계의 재조합 단백질 식품 원료 시장의 주요 기업은 DSM-Firmenich, Geltor Inc., Perfect Day Inc., The EVERY Company, Kerry Group plc, Givaudan SA, Motif FoodWorks Inc., Novozymes A/S, Chr. Hansen Holding A/S, Impossible Foods Inc. 등이 주요 기업로서 시장에서의 존재감 확대와 경쟁력 강화를 위한 전략적 시책을 추진하고 있습니다. 각 회사는 단백질 설계의 최적화, 생산 효율의 향상, 정밀 발효에 의한 확장성의 향상을 도모하기 위해 연구 개발에 다액의 투자를 실시했습니다. 식품 제조업체나 바이오테크놀러지 기업과의 전략적 제휴, 파트너십, 합작 사업은 신규 단백질의 상업화를 가속화하는 데 도움이 되고 있습니다. 또한 수요 증가에 대응하기 위해 세계 제조 능력 확대와 신규 지역 시장 진출도 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능한 단백질 대체품에 대한 소비자 수요 증가

- 정밀 발효의 스케일 업에 있어서 기술적 진보

- 규제 당국의 승인이 상업 시장 진입을 가속

- 업계의 잠재적 위험 및 과제

- 상업 규모의 높은 자본 투자 요건

- 신규 단백질 원료에 대한 소비자 수용의 장벽

- 시장 기회

- 식물성 식품 카테고리에 있어서 응용 범위의 확대

- 대체 단백질 혁신에 대한 정부 지원

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 단백질의 기능성별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국의 고려

- 전망과 기회

- 시장 예측의 요약(2025-2034년)

- 신흥 시장 기회

- 기술 로드맵과 혁신 파이프라인

- 투자 기회와 리스크 평가

- 시장 진입을 위한 전략적 제안

- 미래 시장 시나리오 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협력

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계·예측 : 생산 기술별(2021-2034년)

- 주요 동향

- 정밀 발효

- 바이오매스 발효

- 무세포 시스템

- 하이브리드 및 신흥 기술

제6장 시장추계·예측 : 단백질 기능성별(2021-2034년)

- 주요 동향

- 구조 단백질

- 카제인 및 유청 단백질

- 콜라겐 및 젤라틴

- 계란 단백질

- 기능성 효소

- 트랜스글루타미나제

- 리파아제 및 프로테아제

- 아밀라아제 및 셀룰라아제

- 감각 강화 단백질

- 헴 단백질

- 풍미 활성 펩티드

- 영양 단백질

- 락토페린 및 면역글로불린

- 생리활성 펩티드

- 단세포 단백질

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 식물성 육류 및 해산물

- 유제품 대체품 및 유사품

- 음료 및 기능성 음료

- 제빵, 제과 및 스낵

- 직접 산업 용도

제8장 시장추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Chr. Hansen Holding A/S

- DSM-Firmenich

- Geltor Inc.

- Givaudan SA

- Impossible Foods Inc.

- Kerry Group plc

- Motif FoodWorks Inc.

- Novozymes A/S

- Perfect Day Inc.

- The EVERY Company

The Global Recombinant Protein Food Ingredients Market was valued at USD 900 million in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 1.9 Billion by 2034.

The industry is expanding rapidly as advancements in biotechnology and the growing consumer preference for sustainable and functional foods reshape the food innovation landscape. Rising incidences of chronic illnesses and the growing emphasis on personalized nutrition are key drivers fueling market demand. Manufacturers are enhancing the capabilities of synthetic biology, strain engineering, and precision fermentation to develop proteins that replicate the texture, nutritional profile, and sensory characteristics of animal-derived proteins. This progress is enabling large-scale production, transforming recombinant proteins from laboratory concepts to commercial ingredients in dairy, meat, and beverage applications. Sustainability has become central to this evolution, with producers focusing on circular and low-carbon manufacturing processes. Novel technologies such as gas fermentation and the use of agricultural byproducts are reducing carbon intensity, potentially leading to carbon-negative protein production. These sustainable developments align with global decarbonization and ESG goals, attracting investors who prioritize environmental responsibility. The growing emphasis on eco-friendly production methods also strengthens consumer trust and global regulatory approval.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $900 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 7.8% |

The precision fermentation segment held a 70% share in 2024, as this method utilizes engineered microorganisms to produce highly pure and consistent proteins that closely resemble animal proteins. This approach has become the industry standard due to its scalability, regulatory compliance, and cost-efficiency, supporting mass production for dairy, egg, and meat substitute applications.

The structural proteins segment held a 40% share in 2024 and is projected to reach USD 778 million by 2034. These proteins play a crucial role in providing structure, stability, and binding properties in food formulations, particularly within plant-based meat, cheese, and bakery applications. Industrial partnerships have accelerated the production process, enabling large-scale manufacturing of key protein ingredients used across alternative food segments.

North America Recombinant Protein Food Ingredients Market was valued at USD 379 million in 2024 and is expected to grow at a CAGR of 8% through 2034. The region benefits from a robust biotechnology ecosystem, favorable FDA regulatory pathways under the GRAS framework, increasing venture capital investments, and rising consumer awareness of sustainable protein alternatives. Additionally, collaborative initiatives and funding programs continue to strengthen the production and commercialization of recombinant protein ingredients across North America.

Leading companies in the Global Recombinant Protein Food Ingredients Market include DSM-Firmenich, Geltor Inc., Perfect Day Inc., The EVERY Company, Kerry Group plc, Givaudan SA, Motif FoodWorks Inc., Novozymes A/S, Chr. Hansen Holding A/S and Impossible Foods Inc. are Major players in the Recombinant Protein Food Ingredients Market and are employing strategic measures to expand their market presence and enhance competitiveness. Companies are heavily investing in research and development to optimize protein design, improve production efficiency, and achieve better scalability through precision fermentation. Strategic collaborations, partnerships, and joint ventures with food manufacturers and biotechnology firms are helping accelerate the commercialization of novel proteins. Firms are also expanding their global manufacturing capacities and entering new regional markets to meet rising demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Production technology

- 2.2.3 Protein functionality

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for sustainable protein alternatives

- 3.2.1.2 Technological advancements in precision fermentation scaling

- 3.2.1.3 Regulatory approvals accelerating commercial market entry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements for commercial scale

- 3.2.2.2 Consumer acceptance barriers for novel protein ingredients

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding applications in plant-based food categories

- 3.2.3.2 Government support for alternative protein innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By protein functionality

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

- 3.14 Future outlook & opportunities

- 3.15 Market forecast summary (2025-2034)

- 3.15.1 Emerging market opportunities

- 3.15.2 Technology roadmap & innovation pipeline

- 3.15.3 Investment opportunities & risk assessment

- 3.15.4 Strategic recommendations for market entry

- 3.15.5 Future market scenarios analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Production Technology, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Precision fermentation

- 5.3 Biomass fermentation

- 5.4 Cell-free systems

- 5.5 Hybrid & emerging

Chapter 6 Market Estimates and Forecast, Protein Functionality, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Structural proteins

- 6.2.1 Casein & whey proteins

- 6.2.2 Collagen & gelatin

- 6.2.3 Egg proteins

- 6.3 Functional enzymes

- 6.3.1 Transglutaminase

- 6.3.2 Lipases & proteases

- 6.3.3 Amylases & cellulases

- 6.4 Sensory enhancement proteins

- 6.4.1 Heme proteins

- 6.4.2 Flavor-active peptides

- 6.5 Nutritional proteins

- 6.5.1 Lactoferrin & immunoglobulins

- 6.5.2 Bioactive peptides

- 6.5.3 Single-cell proteins

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 Plant-based meat & seafood

- 7.3 Dairy alternatives & analogs

- 7.4 Beverages & functional drinks

- 7.5 Bakery, confectionery & snacks

- 7.6 Direct industrial applications

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Chr. Hansen Holding A/S

- 9.2 DSM-Firmenich

- 9.3 Geltor Inc.

- 9.4 Givaudan SA

- 9.5 Impossible Foods Inc.

- 9.6 Kerry Group plc

- 9.7 Motif FoodWorks Inc.

- 9.8 Novozymes A/S

- 9.9 Perfect Day Inc.

- 9.10 The EVERY Company