|

시장보고서

상품코드

1871087

화염방지기 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Flame Arrestors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

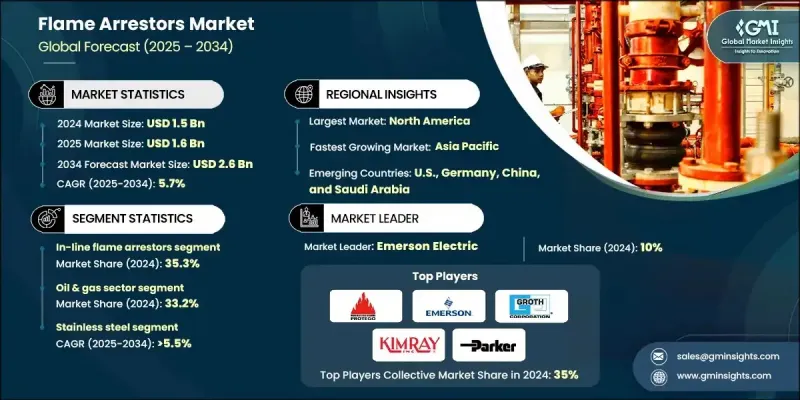

세계의 화염방지기 시장은 2024년에 15억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 5.7%를 나타낼 것으로 예측되며 26억 달러에 달할 전망입니다.

석유화학, 정유 및 저장 부문에 걸친 규제 의무 강화와 함께 산업 안전 규정 준수에 대한 강조가 증가하면서 시장이 꾸준히 확대되고 있습니다. 개발도상국에서의 연료 및 화학 저장 시설 건설 증가와 대기 배출 관련 환경 규제 강화는 비즈니스 전망을 지속적으로 형성하고 있습니다. 화염방지기는 가연성 가스 또는 증기 혼합물이 포함된 시스템에서 화염 전단을 열흡수 요소(주로 금속 메쉬 또는 다공성 재료로 구성)를 통해 소멸시켜 화염 확산을 방지하는 핵심 안전 장치입니다. 이 설계는 화염을 점화 온도 이하로 냉각시켜 연소를 효과적으로 차단합니다. 엄격한 폭발 방지 및 안전 기준에 힘입어 산업 시설 내 수소 활용 및 혼합 활동이 급증하면서 시장 성장을 주도하고 있습니다. 산업 인프라의 지속적인 발전, 증기 회수 및 배출 제어 기술의 통합, 신뢰할 수 있는 배기 솔루션에 대한 수요 증가는 제품 배포를 더욱 확대하고 있습니다. 해양 지원 운영 및 해상 연료 공급 활동의 확대와 강화된 선박 안전 요건 역시 글로벌 시장 성장세에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 26억 달러 |

| CAGR | 5.7% |

인라인 화염방지기 부문은 2024년 35.3%의 점유율을 기록했으며, 2034년까지 연평균 5.5%의 성장률을 보일 것으로 전망됩니다. 이 장치들은 상류 및 하류 방향으로의 화염 전파를 방지함으로써 산업 배관 네트워크의 공정 안전 유지에 필수적입니다. 화학, 석유화학 및 공정 제조 시설 전반에 걸친 적용 확대는 고위험 환경에서 지속적인 양방향 보호 필요성에 힘입은 것입니다. 복잡한 공정 시스템에 대한 신뢰성과 적응성은 폭발 방지 및 공정 무결성에 중점을 둔 현대 산업 운영에 없어서는 안 될 구성 요소로 자리매김하게 합니다.

석유 및 가스 부문은 2024년 33.2%의 점유율을 기록했으며, 2025-2034년 연평균 복합 성장률(CAGR) 5.5%로 성장할 것으로 예상됩니다. 이 부문의 성장은 상류, 중류, 하류 운영 전반에 걸친 지속적인 확장에 의해 주도되며, 각 단계는 신뢰할 수 있는 화염 방지 기술을 필요로 합니다. 생산, 시추 및 가공 운영 내 응용 부문는 일상적 및 비상 시나리오에서 탄화수소 증기의 점화를 방지하기 위해 화염 방지기에 의존합니다. 에너지 가치 사슬 전반에 걸친 운영 안전 및 규제 준수에 대한 지속적인 초점은 제품 수요에 영향을 미치는 핵심 요소로 남아 있습니다.

미국의 화염방지기 시장은 2024년 4억 1,700만 달러 규모를 기록했습니다. 정유, 석유화학, 발전 설비의 현대화와 함께 강화된 직업 및 화재 안전 규정 시행이 시장 성장을 뒷받침하고 있습니다. LNG 시설 및 수소 혼합 사업에 대한 투자 확대는 산업용 화염방지기 도입을 더욱 가속화하고 있습니다. 또한 기업들은 위험 기반 유지보수 프로그램과 자산 무결성 관리 전략을 점점 더 채택하면서, 구식 화염방지기를 첨단 규격 준수 시스템으로 선제적으로 교체하고 있습니다.

세계의 화염방지기 시장에서 주요 역할을 담당하는 기업은 파커 허니핀, 엘맥 테크놀로지스, 에머슨 일렉트릭, 더 프로텍트 씰 컴퍼니, 프로테고, 선플로 테크놀로지스, D-KTC 플루이드 컨트롤, L& J 테크놀로지 즈, 캐쉬코, 김레이, 위트 가세 테크닉, 에섹스 인더스트리즈, 글로스 코퍼레이션, 아마라마 엔지니어스, 피디콘 디바이스, BS& 등이 있습니다. 화염방지기 시장의 주요 기업은 시장 지위를 강화하고 경쟁력을 높이기 위해 다양한 전략을 시행하고 있습니다. 선도적 제조업체들은 진화하는 안전 기준을 충족하고 극한 산업 환경에서도 작동 가능한 고성능 방지기 개발을 위해 연구개발(R&D)에 투자하고 있습니다. 제품 포트폴리오 확대와 지리적 범위 확장을 위해 전략적 합병, 파트너십 및 협력을 추진 중입니다. 또한 제조 과정에서 첨단 소재와 자동화를 활용해 생산 효율성에 집중하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 가용성 및 조달 분석

- 제조 능력 평가

- 공급망의 회복력과 위험 요인

- 유통 네트워크 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 억제요인 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 화염방지기의 비용 구조 분석

- 새로운 기회와 동향

- 디지털화와 IoT 통합

- 투자분석과 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- Key partnerships &collaborations

- Major M&A activities

- Product innovations &launches

- Market expansion strategies

- 전략적 이니셔티브

- 경쟁 벤치마킹

- 혁신과 기술의 정세

제5장 시장 규모와 예측 : 제품별(2021-2034년)

- 주요 동향

- 인라인 화염방지기

- 엔드오브라인 화염방지기

- 폭연 방지기

- 폭발 방지기

- 기타

제6장 시장 규모와 예측 : 재료별(2021-2034년)

- 주요 동향

- 스테인리스 스틸

- 탄소강

- 알루미늄

- 기타

제7장 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 석유 및 가스

- 화학제품

- 제약

- 정유소

- 발전소

- 광업

- 폐수 처리

- 기타

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 인도네시아

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제9장 기업 프로파일

- PROTEGO

- Aager

- Amarama Engineers

- BS&B Innovations

- Cashco

- Cochin Steel

- D-KTC Fluid Control

- Elmac Technologies

- Emerson Electric

- Essex Industries

- Fidicon Devices

- Groth Corporation

- Kimray

- L&J Technologies

- Mott

- Paradox IP

- Parker Hannifin

- Sunflow Technologies

- The Protectoseal Company

- WITT-GASETECHNIK

The Global Flame Arrestors Market was valued at USD 1.5 Billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.6 Billion by 2034.

Growing emphasis on industrial safety compliance, coupled with stronger regulatory mandates across petrochemical, refining, and storage sectors, is driving steady market expansion. Increasing construction of fuel and chemical storage facilities in developing economies, along with rising environmental scrutiny related to air emissions, continues to shape the business outlook. A flame arrestor is a critical safety device that prevents the spread of flames in systems containing flammable gas or vapor mixtures by quenching the flame front through a heat-absorbing element, often composed of metal mesh or porous materials. This design cools the flame below its ignition temperature, effectively halting combustion. The surge in hydrogen utilization and blending activities within industrial facilities, driven by stringent explosion prevention and safety standards, is propelling market growth. Continuous advancements in industrial infrastructure, the integration of vapor recovery and emission control technologies, and the rising demand for reliable venting solutions are further enhancing product deployment. Expanding offshore support operations and maritime fueling activities, together with reinforced shipboard safety requirements, are also contributing to global market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.7% |

The in-line flame arrestor segment held 35.3% share in 2024 and is forecast to grow at a CAGR of 5.5% through 2034. These devices are essential for maintaining process safety in industrial piping networks by preventing flame travel in both upstream and downstream directions. Their growing application across chemical, petrochemical, and process manufacturing facilities is fueled by the need for continuous bidirectional protection in high-risk environments. Their reliability and adaptability to complex process systems make them indispensable components for modern industrial operations focused on explosion prevention and process integrity.

The oil & gas sector held a 33.2% share in 2024 and is expected to grow at a CAGR of 5.5% between 2025 and 2034. Growth in this sector is driven by ongoing expansion across upstream, midstream, and downstream operations, each requiring dependable flame prevention technologies. Applications within production, drilling, and processing operations rely on flame arrestors to safeguard facilities from the ignition of hydrocarbon vapors during routine and emergency scenarios. The continuous focus on operational safety and regulatory compliance across the energy value chain remains a key factor influencing product demand.

United States Flame Arrestors Market generated USD 417 million in 2024. Market growth in the country is supported by the modernization of refining, petrochemical, and power generation assets, accompanied by heightened enforcement of occupational and fire safety regulations. Expanding investments in LNG facilities and hydrogen blending initiatives are further accelerating the deployment of flame arrestors in industrial applications. Additionally, companies are increasingly adopting risk-based maintenance programs and asset integrity management strategies, resulting in proactive replacement of outdated flame protection equipment with advanced, compliant systems.

Prominent players operating in the Global Flame Arrestors Market include Parker Hannifin, Elmac Technologies, Emerson Electric, The Protectoseal Company, PROTEGO, Sunflow Technologies, D-KTC Fluid Control, L&J Technologies, Cashco, Kimray, WITT-GASETECHNIK, Essex Industries, Groth Corporation, Amarama Engineers, Fidicon Devices, BS&B Innovations, Cochin Steel, Paradox IP, Aager, and Mott. Key companies in the Flame Arrestors Market are implementing diverse strategies to strengthen their market position and enhance competitiveness. Leading manufacturers are investing in R&D to develop high-performance arrestors that meet evolving safety standards and can operate under extreme industrial conditions. Strategic mergers, partnerships, and collaborations are being pursued to expand product portfolios and extend geographic reach. Companies are also focusing on production efficiency using advanced materials and automation in manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Material trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of flame arrestors

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization and IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 In-line flame arrestors

- 5.3 End-of-line flame arrestors

- 5.4 Deflagration arrestors

- 5.5 Detonation arrestors

- 5.6 Others

Chapter 6 Market Size and Forecast, By Material, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Carbon steel

- 6.4 Aluminum

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Chemicals

- 7.4 Pharmaceutical

- 7.5 Refineries

- 7.6 Power plants

- 7.7 Mining

- 7.8 Wastewater treatment

- 7.9 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 PROTEGO

- 9.2 Aager

- 9.3 Amarama Engineers

- 9.4 BS&B Innovations

- 9.5 Cashco

- 9.6 Cochin Steel

- 9.7 D-KTC Fluid Control

- 9.8 Elmac Technologies

- 9.9 Emerson Electric

- 9.10 Essex Industries

- 9.11 Fidicon Devices

- 9.12 Groth Corporation

- 9.13 Kimray

- 9.14 L&J Technologies

- 9.15 Mott

- 9.16 Paradox IP

- 9.17 Parker Hannifin

- 9.18 Sunflow Technologies

- 9.19 The Protectoseal Company

- 9.20 WITT-GASETECHNIK