|

시장보고서

상품코드

1871089

자동차 사출 성형 자동화 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Injection Molding Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

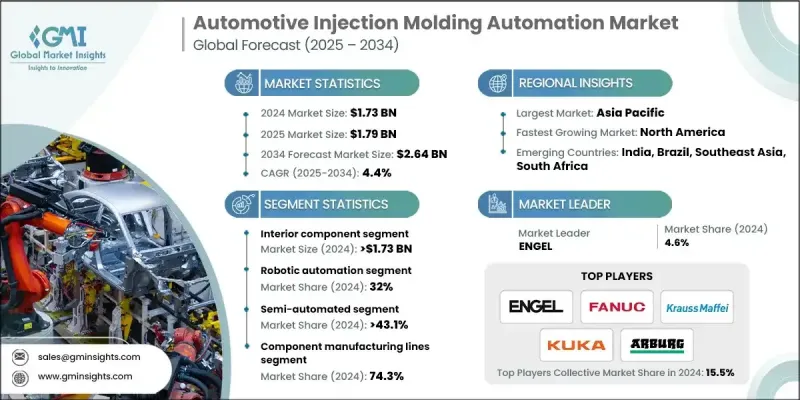

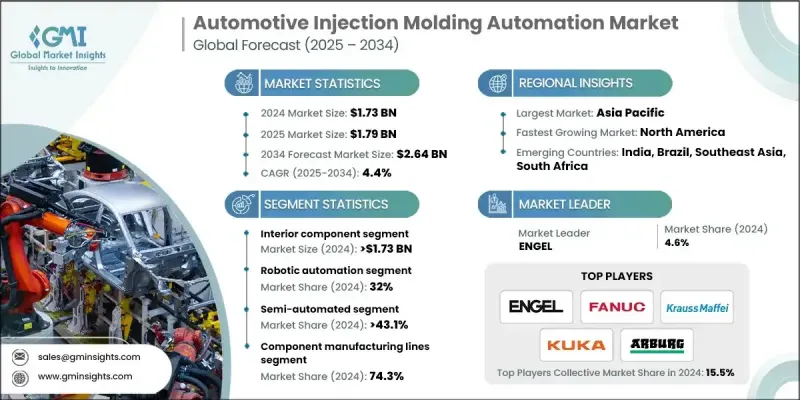

세계의 자동차 사출성형 자동화 시장은 2024년 17억 3,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 4.4%를 나타낼 것으로 예측되며 26억 4,000만 달러에 달할 전망입니다.

제조업에서 자동화 채택이 증가하는 것은 생산성 향상, 일관된 품질 유지, 인력 의존도 감소에 대한 필요성에 의해 주도되고 있습니다. 로봇 핸들링, 자동화된 품질 검사, 통합 성형 시스템은 제조업체가 결함을 최소화하고 사이클 시간을 단축하며 생산 전반에 걸쳐 효율성을 향상시키는 데 기여하고 있습니다. 이러한 추세는 전 세계 1차 공급업체 및 OEM 조립 공장에서 점점 더 뚜렷하게 나타나고 있습니다. 전기차(EV)의 성장은 경량화, 정밀도, 내열성을 갖춘 플라스틱 부품에 대한 수요를 가속화했습니다. 자동화 사출 성형은 높은 반복성과 치수 정확도를 갖춘 복잡한 부품 생산을 가능하게 합니다. 성형 작업에 AI, IoT, 머신 러닝을 통합하면 실시간 모니터링, 예측 유지보수, 공정 최적화가 가능합니다. 연결된 자동화 셀을 활용하는 스마트 팩토리는 데이터 기반 의사 결정을 촉진하고, 가동 중지 시간을 줄이며, 재료 낭비를 최소화하여 자동차 사출 성형 공정 전반에 걸친 자동화 수요를 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 17억 3,000만 달러 |

| 예측 금액 | 26억 4,000만 달러 |

| CAGR | 4.4% |

내장 부품 부문은 2024년에 17억 3,000만 달러 시장 규모를 기록했으며, 2025-2034년 연평균 복합 성장률(CAGR) 5%를 보일 것으로 예측됩니다. 특히 전기차(EV)와 첨단 인포테인먼트 시스템의 성장에 따라 경량화, 내구성, 정밀성을 갖춘 내장 부품에 대한 수요가 증가하고 있습니다. 자동화 생산 라인은 대시보드, 패널, 콘솔을 높은 처리량, 낮은 불량률, 일관된 품질로 공급하여 승객 편의성을 높이는 동시에 생산 비용을 절감합니다.

로봇 자동화 부문은 2024년에 32%의 점유율을 획득했습니다. 픽 앤 플레이스, 인서트 로딩, 스태킹 공정과 통합된 로봇 시스템은 효율성을 개선하고, 인적 개입을 줄이며, 반복성을 높이고, 사이클 타임을 단축합니다. 노동 비용 압박과 대량 생산 필요성으로 인해 로봇 기술 도입은 선진국과 신흥 시장 모두에서 확대되고 있습니다.

미국의 자동차 사출 성형 자동화 시장은 2024년 86.4%의 점유율을 차지했습니다. 전기차 및 하이브리드 차량으로의 전환은 배터리 하우징, 커넥터, 전자 인클로저에 대한 자동화 사용을 촉진하고 있습니다. 자동화는 반복 정밀도, 치수 정확도 및 재현성을 보장하여 OEM 및 1차 공급업체가 엄격한 품질 기준을 충족하면서 대량 부품을 효율적으로 생산할 수 있도록 합니다.

자동차 사출 성형 자동화 시장의 주요 기업으로는 KUKA, 스미토모중기계산업(SHI-Demag), ENGEL, 하이티안, ARBURG, FANUC, 클라우스 맥파이, 위트먼 배튼펠트, 닛세이 플라스틱 산업 등을 들 수 있습니다. 자동차 사출 성형 자동화 시장의 기업은 혁신, 기술 통합 및 전략적 파트너십을 활용하여 시장 입지를 강화하고 있습니다. 이들은 로봇 시스템, AI 기반 품질 관리 및 스마트 공장 솔루션을 향상시키기 위해 연구 개발에 투자합니다. OEM 및 1차 공급업체와의 협력을 통해 시장 진출을 확대하고 솔루션을 생산 라인에 직접 통합합니다. 또한 기업들은 다양한 제조 요구를 충족하고 확장 가능한 솔루션을 제공하기 위해 모듈식 자동화 시스템에 주력하고 있습니다. 디지털화와 IoT 통합은 공정 모니터링 및 예측 유지보수를 개선하여 가동 중단 시간과 운영 비용을 절감합니다. 또한 기업들은 고객 신뢰도를 높이기 위해 고객 지원, 교육 프로그램 및 애프터서비스를 강조하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 제조업체

- 시스템 통합자

- OEM

- 최종 용도

- 공급자의 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동차 제조업의 자동화 확대

- 기차(EV) 및 경량화 추세

- 인더스트리 4.0, 스마트 팩토리 도입

- 대량 생산 요구

- 품질과 안전기준 향상

- 업계의 잠재적 억제요인 및 과제

- 높은 초기 자본 투자

- 숙련된 인력 요구

- 시장 기회

- 신흥 시장에서의 성장

- 기존 라인의 자동화 개조

- 첨단 로봇공학 및 AI 통합

- 지속가능하고 에너지 효율적인 시스템에 대한 수요

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현행 기술

- 신흥기술

- 특허 분석

- 가격 동향 분석

- 컴포넌트별

- 지역별

- 코스트 내역 분석

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율화

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 장래의 동향

- 신기술 동향

- 전기자동차의 영향 분석

- 지속가능성과 재활용 기회

- Industry 4.0의 진화

- 지역별 성장의 중점 지역

- 투자 기회

- 위험 평가 및 경감책

- 총소유비용분석

- 실시 스케줄과 프로젝트 계획

- 연수 및 스킬 개발 요건

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 뉴스와 대처

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대계획과 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 내장 부품

- 외장 부품

- 기타

제6장 시장 추계 및 예측 : 자동화별(2021-2034년)

- 주요 동향

- 로봇 자동화

- 공정 제어 자동화

- 자재관리 자동화

- 품질 검사 자동화

- 포장 및 후공정 자동화

제7장 시장 추계 및 예측 : 자동화 레벨별(2021-2034년)

- 주요 동향

- 반자동화 시스템

- 완전 자동화 시스템

- 스마트/인더스트리 4.0 대응 시스템

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 부품 제조 라인

- 정밀 금형 및 금형 설계

- 2차 가공 및 마감

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 네덜란드

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- FANUC

- ENGEL

- KraussMaffei

- ARBURG

- Sumitomo Heavy Industries

- Husky Injection Molding Systems

- Milacron

- 지역 기업

- Star Automation

- Baumuller

- Haitian

- Moog

- Wittmann Battenfeld

- JSW Plastics Machinery

- Toyo Machinery &Metal

- Nissei Plastic Industrial

- 신흥 기업 및 혁신기업

- JR Automation

- Absolute Haitian

- Sepro

- Yizumi

- Tederic Machinery

- LK Technology

- Specialized Automation Suppliers

- ABB Robotics

- KUKA

- Universal Robots

- Staubli

- Kawasaki Robotics

- Comau

- Denso Robotics

- Epson Robots

- Omron Adept

- Yaskawa Motoman

The Global Automotive Injection Molding Automation Market was valued at USD 1.73 Billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 2.64 Billion by 2034.

The rising adoption of automation in manufacturing is driven by the need for higher productivity, consistent quality, and reduced reliance on manual labor. Robotic handling, automated quality checks, and integrated molding systems are helping manufacturers minimize defects, shorten cycle times, and enhance efficiency throughout production. This trend is increasingly evident among Tier-1 suppliers and OEM assembly plants worldwide. The growth of electric vehicles (EVs) has accelerated demand for lightweight, precise, and heat-resistant plastic components. Automated injection molding enables the production of complex components with high repeatability and dimensional accuracy. Incorporating AI, IoT, and machine learning in molding operations allows real-time monitoring, predictive maintenance, and process optimization. Smart factories leveraging connected automation cells are driving data-based decision-making, reducing downtime, and minimizing material waste, further strengthening demand for automation across automotive injection molding processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.73 Billion |

| Forecast Value | $2.64 Billion |

| CAGR | 4.4% |

The interior component segment generated USD 1.73 Billion in 2024 and is expected to grow at a CAGR of 5% from 2025 to 2034. Demand for lightweight, durable, and precise interior components is rising, especially with the growth of EVs and advanced infotainment systems. Automated production lines deliver dashboards, panels, and consoles with high throughput, low scrap rates, and consistent quality, enhancing passenger comfort while reducing production costs.

The robotic automation segment captured a 32% share in 2024. Robotic systems integrated with pick-and-place, insert loading, and stacking processes improve efficiency, reduce human intervention, enhance repeatability, and shorten cycle times. The adoption of robotics is expanding in both developed and emerging markets due to labor cost pressures and the need for high-volume production.

U.S. Automotive Injection Molding Automation Market held 86.4% share in 2024. The shift to electric and hybrid vehicles is driving the use of automation for battery housings, connectors, and electronic enclosures. Automation ensures repeated precision, dimensional accuracy, and repeatability, enabling OEMs and Tier-1 suppliers to meet stringent quality standards while efficiently producing high-volume parts.

Key players in the Automotive Injection Molding Automation Market include KUKA, Sumitomo (SHI-Demag), ENGEL, Haitian, ARBURG, FANUC, KraussMaffei, Wittmann Battenfeld, and Nissei Plastic Industrial. Companies in the Automotive Injection Molding Automation Market are leveraging innovation, technological integration, and strategic partnerships to strengthen their market position. They invest in R&D to enhance robotic systems, AI-driven quality controls, and smart factory solutions. Collaborations with OEMs and Tier-1 suppliers help expand reach and integrate solutions directly into production lines. Firms are also focusing on modular automation systems to cater to diverse manufacturing needs and offer scalable solutions. Digitalization and IoT integration improve process monitoring and predictive maintenance, reducing downtime and operational costs. Additionally, companies emphasize customer support, training programs, and after-sales services to enhance client trust.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component

- 2.2.2 Automation

- 2.2.3 Level of automation

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 System integrators

- 3.1.1.4 OEM

- 3.1.1.5 End use

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation in automotive manufacturing

- 3.2.1.2 EV and lightweighting trend

- 3.2.1.3 Industry 4.0 / smart factory adoption

- 3.2.1.4 High-volume production needs

- 3.2.1.5 Increasing quality and safety standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Skilled workforce requirement

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging markets

- 3.2.3.2 Retrofitting existing lines with automation

- 3.2.3.3 Advanced robotics and AI integration

- 3.2.3.4 Demand for sustainable and energy-efficient systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable Practices

- 3.11.2 Waste Reduction Strategies

- 3.11.3 Energy Efficiency in Production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon Footprint Considerations

- 3.12 Future trends

- 3.12.1 Emerging Technology Trends

- 3.12.2 Electric Vehicle Impact Analysis

- 3.12.3 Sustainability & Recycling Opportunities

- 3.12.4 Industry 4.0 Evolution

- 3.12.5 Regional Growth Hotspots

- 3.12.6 Investment Opportunities

- 3.12.7 Risk Assessment & Mitigation

- 3.13 Total Cost of Ownership Analysis

- 3.14 Implementation Timeline & Project Planning

- 3.15 Training & Skill Development Requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Interior Components

- 5.3 Exterior Components

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Automation, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Robotic automation

- 6.3 Process control automation

- 6.4 Material handling automation

- 6.5 Quality inspection automation

- 6.6 Packaging & Post-Processing Automation

Chapter 7 Market Estimates & Forecast, By Level of Automation, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Semi-Automated systems

- 7.3 Fully Automated systems

- 7.4 Smart/Industry 4.0-Enabled Systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Component Manufacturing Lines

- 8.3 Precision Tooling & Mold Engineering

- 8.4 Secondary Production & Finishing

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 FANUC

- 10.1.2 ENGEL

- 10.1.3 KraussMaffei

- 10.1.4 ARBURG

- 10.1.5 Sumitomo Heavy Industries

- 10.1.6 Husky Injection Molding Systems

- 10.1.7 Milacron

- 10.2 Regional Players

- 10.2.1 Star Automation

- 10.2.2 Baumuller

- 10.2.3 Haitian

- 10.2.4 Moog

- 10.2.5 Wittmann Battenfeld

- 10.2.6 JSW Plastics Machinery

- 10.2.7 Toyo Machinery & Metal

- 10.2.8 Nissei Plastic Industrial

- 10.3 Emerging Players and Disruptors

- 10.3.1 JR Automation

- 10.3.2 Absolute Haitian

- 10.3.3 Sepro

- 10.3.4 Yizumi

- 10.3.5 Tederic Machinery

- 10.3.6 LK Technology

- 10.4 Specialized Automation Suppliers

- 10.4.1 ABB Robotics

- 10.4.2 KUKA

- 10.4.3 Universal Robots

- 10.4.4 Staubli

- 10.4.5 Kawasaki Robotics

- 10.4.6 Comau

- 10.4.7 Denso Robotics

- 10.4.8 Epson Robots

- 10.4.9 Omron Adept

- 10.4.10 Yaskawa Motoman