|

시장보고서

상품코드

1871098

재생 콘크리트 골재(RCA) 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Recycled Concrete Aggregate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

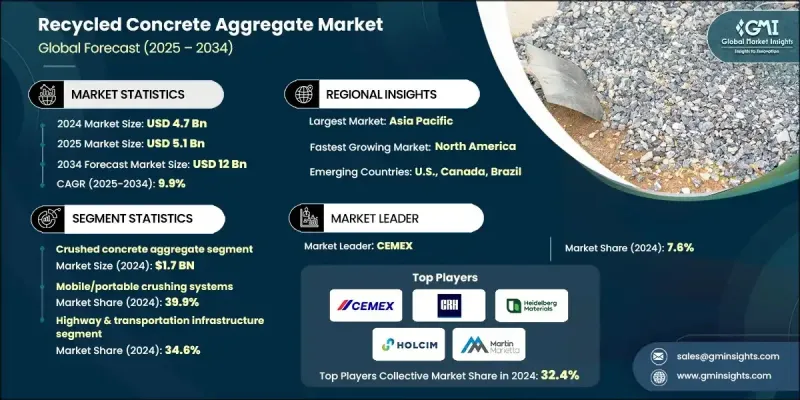

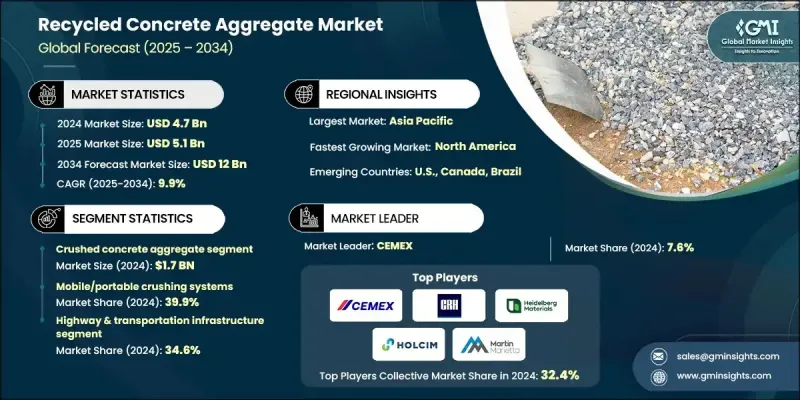

세계의 재생 콘크리트 골재 시장은 2024년에 47억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 9.9%를 나타낼 것으로 예측되며 120억 달러에 달할 전망입니다.

재생 콘크리트 골재는 철거된 콘크리트 자재를 가공하여 사용 가능한 골재 대체재로 생산되며, 이는 고갈되는 천연 자원에 대한 의존도를 낮춥니다. 많은 지역에서 천연 골재의 가용성이 급격히 감소함에 따라 정부와 산업계는 자원 보존 전략을 강화하고 있습니다. 건설 부문의 환경 파괴와 탄소 배출에 대한 우려가 커지면서 RCA와 같은 지속 가능한 대체재에 대한 수요가 가속화되고 있습니다. 현대적인 인프라 개발과 친환경 건설 방법에 대한 관심 증대가 이러한 추세의 주요 요인입니다. 또한 RCA는 원자재 비용을 최소화하고 운송 수요를 줄이며 환경 규정 준수 비용을 낮춤으로써 강력한 비용 경쟁력을 제공합니다. 아시아태평양 지역은 재활용 가능한 잔해물을 대량으로 생산하는 급속한 도시 개발 및 인프라 확장에 힘입어 현재 시장을 주도하고 있습니다. 한편 유럽은 엄격한 지속가능성 의무와 첨단 재활용 기술에 대한 투자 증가로 가장 빠른 성장을 보이고 있습니다. 이러한 지역적 역학은 건설 부문에서 순환 경제 관행으로의 글로벌 전환을 반영하며, 재활용 재료가 주거, 상업 및 공공 인프라 부문 전반에서 더욱 강력한 추진력을 얻고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 47억 달러 |

| 예측 금액 | 120억 달러 |

| CAGR | 9.9% |

분쇄 콘크리트 골재 부문은 2024년 17억 달러의 매출을 기록했습니다. 이 재료는 1차 및 2차 분쇄 공정을 통해 다양한 입자 크기로 생산되며, 기초층 및 배수층부터 신규 콘크리트 생산에 이르기까지 다양한 용도로 사용됩니다. 시설들은 특정 프로젝트 요구사항에 맞춰 입도 분포 수준을 미세 조정함으로써 생산량을 최적화하고, 더 큰 다용성과 적용 적합성을 보장하고 있습니다.

2024년 기준, 이동식 및 휴대용 분쇄 시스템 부문은 39.9%의 점유율을 차지했습니다. 이 부문은 철거 현장에서 직접 재료를 처리할 수 있는 능력 덕분에 계속해서 우위를 점하고 있습니다. 현장 처리의 매력은 비용 효율성, 환경적 영향 감소, 간소화된 물류에 있으며, 이로 인해 다양한 프로젝트에서 이동식 시스템이 선호되는 솔루션이 되고 있습니다. 이러한 장비의 이동성은 재활용 작업이 프로젝트 일정과 자재 수요에 더 민첩하고 신속하게 대응할 수 있게 합니다.

북미의 재생 콘크리트 골재(RCA) 시장은 2025-2034년 연평균 9.7%의 성장률을 보일 것으로 전망됩니다. 지역별 성장은 지속 가능한 건설 관행의 확산과 폐기물 감축을 목표로 한 규제 체계 강화에 힘입고 있습니다. 건설 및 철거 잔해 재사용을 장려하는 정부 정책은 첨단 재활용 인프라 투자 촉진으로 이어지고 있습니다. 가공 기술의 지속적인 혁신으로 RCA의 성능, 품질 및 신뢰성이 향상되어 도로 건설, 프리캐스트 부품, 지지 구조물 등 구조적 용도로의 활용이 가능해졌습니다.

세계의 재생 콘크리트 골재 시장에서 사업을 전개하고 있는 주요 기업으로는 터맥 그룹, 상하이 제니스 미네랄사, 세멕스, 하이델베르크 머티리얼스, 시카사, 러블 마스터, CRH Plc, 마틴 마리에타 머티리얼스, 홀심, CDE 그룹 등이 있습니다. 재생 콘크리트 골재 시장의 기업들은 입지를 강화하기 위해 생산 능력 확대, 혁신, 전략적 파트너십에 초점을 맞춘 목표 지향적 전략을 추진하고 있습니다. 많은 기업들이 유연성 향상과 가공 비용 절감을 위해 이동식 분쇄 기술에 투자하고 있습니다. 연구 개발 노력은 골재 품질과 성능 개선을 통해 고사양 건설 부문에서의 활용을 확대하는 데 집중되고 있습니다. 건설사, 지방자치단체, 폐기물 관리 기관과의 협력을 통해 자재 공급망을 효율화하고 처리량을 증대시키고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 천연 골재 고갈과 자원 보전 의무

- 인프라 현대화와 지속 가능한 건설 성장

- 천연 자원 채굴에 대한 비용 우위

- 업계의 잠재적 억제요인 및 과제

- 품질의 편차와 성능의 안정성 과제

- 가공 설비에 대한 투자 및 운용 비용

- 시장 기회

- 고성능 콘크리트의 응용 개발

- 첨단 분리 기술 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드 참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 조골재 재생 콘크리트 골재

- 세골재 재생 콘크리트 골재

- 분쇄 콘크리트 골재

- 재생 콘크리트 재료

- 기타

제6장 시장 추계 및 예측 : 처리 방법별(2021-2034년)

- 주요 동향

- 이동식/휴대용 분쇄 시스템

- 고정식 분쇄 플랜트

- 조식 분쇄 기술

- 고급 분리 기술

- 기타

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 고속도로 및 교통 인프라

- 포장 기반층/하부 기반층

- 교량 건설 및 보수 용도

- 공항 활주로 및 유도로 건설

- 항만 및 해양 인프라 개발

- 철도 밸러스트 및 궤도 부설 용도

- 레디믹스 콘크리트 제조

- 구조용 콘크리트

- 비구조용 콘크리트

- 프리캐스트 콘크리트 부재의 제조

- 건축용 콘크리트 및 장식용도

- 매스 콘크리트 및 기초 용도

- 아스팔트 콘크리트 제조

- 핫믹스 아스팔트(HMA) 제조

- 웜믹스 아스팔트(WMA)의 응용

- 콜드믹스 아스팔트 및 보수재

- 아스팔트 기층 포장 공사

- 표면 처리 및 칩 씰 시공

- 건설 및 해체 재활용

- 일반 충진 및 백필

- 부지 개발 및 평탄화

- 유틸리티 트렌치 백필 및 지하 시공

- 조경 및 부지 정비

- 가설 도로 공사

- 프리캐스트 콘크리트 제조

- 프리캐스트 건축 부재(패널, 보, 기둥)

- 인프라용 프리캐스트(배수로, 파이프, 배리어)

- 건축용 프리캐스트 및 외관 부재

- 프리스트레스트 콘크리트 응용

- 콘크리트 블록 및 벽돌

- 콘크리트 벽돌(CMU)의 제조

- 포장석 및 인터로킹 포장재

- 옹벽 블록

- 건축용 벽돌 및 장식 블록

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- CDE Group

- CEMEX

- CRH Plc

- Heidelberg Materials

- Holcim

- Martin Marietta Materials

- RUBBLE MASTER

- Shanghai Zenith Mineral Co.,Ltd.

- Sika AG

- Tarmac Group

The Global Recycled Concrete Aggregate Market was valued at USD 4.7 Billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 12 Billion by 2034.

Recycled concrete aggregate is derived by processing demolished concrete materials into usable aggregate substitutes, reducing reliance on dwindling natural resources. As the availability of natural aggregates declines rapidly in many regions, governments and industries are strengthening resource conservation strategies. Growing concern over environmental degradation and carbon emissions in construction is accelerating the demand for sustainable alternatives like RCA. Modern infrastructure development and increased focus on eco-friendly construction methods are key contributors to this trend. Additionally, RCA provides a compelling cost advantage minimizing raw material expenses, cutting down transportation needs, and lowering environmental compliance costs. The Asia-Pacific region is currently leading the market, fueled by rapid urban development and infrastructure expansion that produces high volumes of recyclable debris. Meanwhile, Europe is seeing the fastest growth, driven by strict sustainability mandates and increased investment in cutting-edge recycling technologies. These regional dynamics reflect a global shift toward circular economy practices in construction, with recycled materials gaining stronger traction across residential, commercial, and public infrastructure sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $12 Billion |

| CAGR | 9.9% |

The crushed concrete aggregate segment generated USD 1.7 Billion in 2024. This material is produced in various particle sizes through primary and secondary crushing processes, serving multiple applications ranging from base layers and drainage to use in new concrete production. Facilities are optimizing output by fine-tuning gradation levels to align with specific project requirements, ensuring greater versatility and application relevance.

In 2024, the mobile and portable crushing systems segment accounted for a 39.9% share. This segment continues to dominate due to its ability to process materials directly at the demolition site. The appeal of on-site processing lies in its cost efficiency, reduced environmental footprint, and streamlined logistics, which make mobile systems the preferred solution across diverse projects. The mobility of these units also allows recycling operations to be more agile and responsive to project timelines and material needs.

North America Recycled Concrete Aggregate Market is projected to grow at a CAGR of 9.7% between 2025 and 2034. Regional growth is being driven by stronger adoption of sustainable construction practices and reinforced regulatory frameworks aimed at waste reduction. Government initiatives promoting the reuse of construction and demolition debris are pushing investment in advanced recycling infrastructure. Continued innovations in processing technology have improved the performance, quality, and reliability of RCA, enabling its use in structural applications such as road construction, precast components, and supporting frameworks.

Key players operating in the Global Recycled Concrete Aggregate Market include Tarmac Group, SHANGHAI ZENITH MINERAL CO., LTD., CEMEX, Heidelberg Materials, Sika AG, RUBBLE MASTER, CRH Plc, Martin Marietta Materials, Holcim, and CDE Group. To strengthen their position, companies in the Recycled Concrete Aggregate Market are pursuing targeted strategies focused on capacity expansion, innovation, and strategic partnerships. Many are investing in mobile crushing technologies to enhance flexibility and reduce processing costs. R&D efforts are being directed toward improving aggregate quality and performance to expand its use in high-specification construction. Collaborations with construction firms, municipalities, and waste management entities are helping streamline material supply chains and boost volume throughput.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Processing method trends

- 2.2.3 End Use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Natural aggregate depletion & resource conservation mandates

- 3.2.1.2 Infrastructure modernization & sustainable construction growth

- 3.2.1.3 Cost advantages against natural extraction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Quality variability & performance consistency challenges

- 3.2.2.2 Processing equipment investment & operational costs

- 3.2.3 Market opportunities

- 3.2.3.1 High-performance concrete applications development

- 3.2.3.2 Advanced separation technology integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Coarse recycled concrete aggregate

- 5.3 Fine recycled concrete aggregate

- 5.4 Crushed concrete aggregate

- 5.5 Reclaimed concrete material

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Processing Method, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Mobile/portable crushing systems

- 6.3 Stationary crushing plants

- 6.4 Jaw crushing technology

- 6.5 Advanced separation technologies

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Highway & transportation infrastructure

- 7.2.1 Pavement base/subbase

- 7.2.2 Bridge construction & repair applications

- 7.2.3 Airport runway & taxiway construction

- 7.2.4 Port & marine infrastructure development

- 7.2.5 Railway ballast & track bed applications

- 7.3 Ready-mix concrete production

- 7.3.1 Structural concrete

- 7.3.2 Non-structural concrete

- 7.3.3 Precast concrete element production

- 7.3.4 Architectural concrete & decorative applications

- 7.3.5 Mass concrete & foundation applications

- 7.4 Asphalt concrete production

- 7.4.1 Hot mix asphalt (HMA) production

- 7.4.2 Warm mix asphalt (WMA) applications

- 7.4.3 Cold mix asphalt & patching materials

- 7.4.4 Asphalt base course construction

- 7.4.5 Surface treatment & chip seal applications

- 7.5 Construction & demolition recycling

- 7.5.1 General fill & backfill

- 7.5.2 Site development & grading

- 7.5.3 Utility trench backfill & underground construction

- 7.5.4 Landscaping & site preparation

- 7.5.5 Temporary road construction

- 7.6 Precast concrete manufacturing

- 7.6.1 Precast building elements (Panels, beams, columns)

- 7.6.2 Infrastructure precast (Culverts, pipes, barriers)

- 7.6.3 Architectural precast & facade elements

- 7.6.4 Prestressed concrete applications

- 7.7 Concrete block & masonry

- 7.7.1 Concrete masonry units (CMU) production

- 7.7.2 Paving stones & interlocking pavers

- 7.7.3 Retaining wall blocks

- 7.7.4 Architectural masonry & decorative blocks

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 CDE Group

- 9.2 CEMEX

- 9.3 CRH Plc

- 9.4 Heidelberg Materials

- 9.5 Holcim

- 9.6 Martin Marietta Materials

- 9.7 RUBBLE MASTER

- 9.8 Shanghai Zenith Mineral Co.,Ltd.

- 9.9 Sika AG

- 9.10 Tarmac Group