|

시장보고서

상품코드

1871107

자동차 예지보전 센서 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Automotive Predictive Maintenance Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

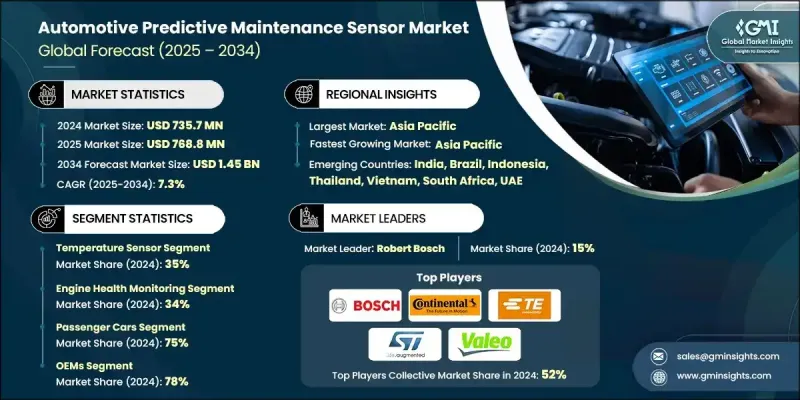

세계의 자동차 예지보전 센서 시장은 2024년 7억 3,570만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 7.3%로 확대되어 14억 5,000만 달러에 이를 것으로 예측됩니다.

시장 성장은 차량의 신뢰성, 운영 안전 및 비용 효율성에 중점을 둔 증가로 인한 것입니다. 예지보전 센서는 중요한 자동차 부품의 상태를 실시간으로 평가하고 고장 발생 전에 잠재적인 문제를 파악하는 데 중요한 역할을 합니다. 이러한 반응적 또는 정기적인 유지보수에서 예방적 전략으로의 전환은 차량의 다운타임 감소 및 운영 비용 절감에 기여합니다. 차량이 첨단 기계 및 전자 시스템을 통합함에 따라 복잡화가 진행되고 있는 가운데, 지속적인 모니터링의 필요성이 확대되고 있습니다. 정부의 안전 규제도 엄격화하고 있어, 제조업체는 첨단 진단 및 감시 시스템의 통합을 강요받고 있습니다. 또한 IoT 프레임워크에서 지원하는 커넥티드카는 데이터의 중앙 집중식 수집과 분석을 가능하게 하고, 예지보전의 정확성과 응답성을 향상시키고 있습니다. 차량 설계, 제조 및 운영 사이클 전반에 걸쳐 데이터 구동형 보전 기법의 보급 확대가 자동차 예지보전 센서 시장의 진화를 계속 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 7억 3,570만 달러 |

| 예측 금액 | 14억 5,000만 달러 |

| CAGR | 7.3% |

온도 센서 부문은 2024년에 35%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 9.14%를 보일 것으로 예측됩니다. 온도 센서는 엔진, 배터리, HVAC 장치 등과 같은 중요한 시스템을 모니터링하는 데 도움이 되기 때문에 예지보전에 가장 널리 사용되는 기술 중 하나입니다. 온도 변동은 과열 및 부품 열화를 일으킬 수 있으므로 이러한 센서는 고장의 조기 발견에 필수적입니다. 실시간 온도 데이터를 제공함으로써 유지보수 팀은 예방적인 수리 계획을 수립하여 예기치 않은 다운타임을 최소화하고 비용을 절감하며 차량의 전반적인 내구성과 신뢰성을 향상시킵니다.

엔진 건강 상태 모니터링 부문은 2024년 34%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 7.04%를 보일 것으로 예측됩니다. 엔진은 차량 성능에서 매우 비싸고 핵심적인 역할을 하기 때문에 엔진 모니터링은 예지보전에 있어 가장 중요한 응용 분야 중 하나가 되고 있습니다. 이 분야의 예측 센서는 진동, 온도, 연료 효율 등 많은 매개변수를 추적하고 고액의 손상으로 발전하기 전에 이상을 감지하는 데 도움이 됩니다. 잠재적인 엔진 고장을 예측 및 방지하는 능력은 자동차 제조업체나 플릿 운영자에게 최적의 성능과 긴 수명을 유지하는 데 큰 경쟁 우위를 가져옵니다.

아시아태평양의 자동차 예지보전 센서 시장은 2024년 44%의 점유율을 차지했으며 3억 2,370만 달러 규모에 달했습니다. 이 지역의 이점은 세계 자동차 생산량의 절반 이상을 차지하는 강력한 생산 기반에 기인합니다. 아시아태평양은 전기자동차, 커넥티드카, 자율주행 시스템의 급속한 진보를 배경으로 기술 혁신의 거점으로 계속되고 있습니다. 지역 제조업체는 실시간 센서 데이터에 따라 유지 보수 수요를 정확하게 예측하는 스마트 차량 플랫폼에 많은 투자를 하고 있습니다. 구조적 성장, 산업의 근대화 및 견조한 기술 개발은 아시아태평양 세계 시장에서 주도적 입장을 강화하고 있습니다.

자동차 예지보전 센서 시장의 주요 기업으로는 Hella, Robert Bosch, STMicroelectronics, Valeo, Infineon Technologies, TE Connectivity, Continental, Sensata Technologies, Murata 등을 들 수 있습니다. 자동차 예지보전 센서 시장에서의 지위를 강화하기 위해 주요 기업은 몇 가지 전략적 조치를 채택하고 있습니다. 많은 기업들이 커넥티드카와 전기자동차 수요에 부응하기 위해 고정밀도, 내구성, 통합 능력을 갖춘 첨단 센서 기술 개발에 주력하고 있습니다. 예측 분석 및 데이터 처리 혁신을 지원하기 위해 R&D 투자는 여전히 우선순위입니다. 자동차 제조업체 및 기술 공급자와의 전략적 제휴 및 협력 관계는 스마트 유지 보수 시스템의 도입 가속에 기여하고 있습니다. 또한 지역 수요 증가에 대응하기 위해 생산 능력 확충과 세계 공급망 최적화도 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 규정 준수 요건(ISO 26262, UNECE 규정)

- 플릿 이용률 최적화 요건

- 전기자동차 도입 가속화

- ADAS(첨단 운전 지원 시스템)의 통합

- 보수 업무에서의 비용 삭감 압력

- 업계의 잠재적 위험 및 과제

- 높은 초기 도입

- 데이터 프라이버시 및 보안에 대한 우려 사항

- 시장 기회

- 소프트웨어 정의 차량 아키텍처 도입

- 5G 및 고급 접속성 도입

- 자율주행 차량 개발

- 순환형 경제와 지속가능성 이니셔티브

- 성장 촉진요인

- 성장 가능성 분석

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 코스트 내역 분석

- 기술 상황

- 현재의 기술 동향

- 신흥기술

- 규제 상황

- 가격 동향

- 지역별

- 센서별

- ROI 및 비즈니스 케이스 분석

- 총소유비용(TCO) 프레임워크

- 도입 비용 구조

- 정량화된 편익 평가

- 투자 및 자금 조달 동향 분석

- 도입 로드맵의 틀

- 단계적 전개 전략

- 통합의 복잡성 분석

- 변경 관리 요건

- 성공 요인의 특정

- 성능 벤치마킹 프레임워크

- KPI의 정의와 측정

- 업계 모범 사례 분석

- 비교 성능 지표

- 지속적인 개선 모델

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 공동 사업

- 신규 용도 출시

- 확대계획과 자금조달

제5장 시장 추계 및 예측 : 센서별, 2021-2034년

- 주요 동향

- 진동 센서

- 온도 센서

- 압력 센서

- 습도 센서

- 음향 센서

- 기타

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 엔진 상태 모니터링

- 변속기 및 기어 박스 모니터링

- 배터리 및 전기 시스템 모니터링

- 타이어 및 휠 모니터링

- 냉각 시스템 모니터링

- 기타

제7장 시장 추계 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용 판매 채널

- 경형 상용차 판매 채널(LCV)

- 중형 상용차 판매 채널(MCV)

- 대형 상용차 판매 채널(HCV)

제8장 시장 추계 및 예측 : 판매 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 필리핀

- 태국

- 한국

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Aptiv

- Continental

- Denso

- Infineon Technologies

- NXP Semiconductors

- Robert Bosch

- TE Connectivity

- ZF Friedrichshafen

- Murata

- 지역 기업

- Allegro MicroSystems

- KEYENCE

- Magna International

- Melexis

- NIRA Dynamics

- Sensata Technologies

- Siemens

- Valeo

- 신흥기업/디스럽터

- Augury Systems

- C3.ai

- Delphi Technologies

- Predii

- Presenso Analytics

- Revvo Technologies

- Samsara

- Tactile Mobility

- Uptake Technologies

The Global Automotive Predictive Maintenance Sensor Market was valued at USD 735.7 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 1.45 Billion by 2034.

Market growth is driven by the growing emphasis on vehicle reliability, operational safety, and cost efficiency. Predictive maintenance sensors play a vital role in assessing the condition of critical automotive components in real time, identifying potential issues before failures occur. This shift from reactive or scheduled maintenance to proactive strategies is helping reduce vehicle downtime and lower operational costs. As vehicles become increasingly complex, incorporating advanced mechanical and electronic systems, the need for continuous monitoring is expanding. Government safety regulations are also getting stricter, pushing manufacturers to integrate advanced diagnostic and monitoring systems. Furthermore, connected vehicles supported by IoT frameworks enable centralized data gathering and analysis, improving the precision and responsiveness of predictive maintenance. The broader adoption of data-driven maintenance practices across vehicle design, manufacturing, and operation cycles continues to shape the evolution of the automotive predictive maintenance sensor market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $735.7 million |

| Forecast Value | $1.45 billion |

| CAGR | 7.3% |

The temperature sensor category held a 35% share in 2024 and is expected to grow at a CAGR of 9.14% through 2034. Temperature sensors are among the most widely used technologies in predictive maintenance, as they help monitor essential systems such as engines, batteries, and HVAC units. Variations in temperature can lead to overheating or component degradation, making these sensors crucial for early fault detection. By delivering real-time temperature data, these sensors allow maintenance teams to schedule repairs proactively, minimizing unplanned downtime, reducing expenses, and enhancing the overall durability and reliability of vehicles.

The engine health monitoring segment held a 34% share in 2024 and is forecast to grow at a CAGR of 7.04% between 2025 and 2034. Engine monitoring remains one of the most critical applications within predictive maintenance due to the engine's high value and central role in vehicle performance. Predictive sensors in this segment track numerous parameters such as vibration, temperature, and fuel efficiency, helping detect irregularities before they escalate into costly damage. The ability to predict and prevent potential engine failures provides automakers and fleet operators with a significant competitive edge in maintaining optimal performance and longevity.

Asia Pacific Automotive Predictive Maintenance Sensor Market held a 44% share and generated USD 323.7 million in 2024. The region's dominance can be attributed to its strong automotive production base, accounting for over half of global vehicle output. Asia Pacific continues to be a hub for technological advancement, with rapid progress in electric, connected, and autonomous vehicle systems. Manufacturers in the region are heavily investing in smart vehicle platforms that rely on real-time sensor data to predict maintenance needs accurately. Structural growth, industrial modernization, and robust technological development are reinforcing Asia Pacific's leadership in the global market.

Prominent players in the Automotive Predictive Maintenance Sensor Market include Hella, Robert Bosch, STMicroelectronics, Valeo, Infineon Technologies, TE Connectivity, Continental, Sensata Technologies, and Murata. To strengthen their position in the automotive predictive maintenance sensor market, leading companies are adopting several strategic measures. Many are focusing on developing advanced sensor technologies with higher accuracy, durability, and integration capability to meet the demands of connected and electric vehicles. Investments in research and development remain a priority to support innovation in predictive analytics and data processing. Strategic collaborations and partnerships with automakers and technology providers are helping accelerate the deployment of smart maintenance systems. In addition, companies are expanding production capacities and optimizing their global supply chains to meet growing regional demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Sensor

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory compliance requirements (ISO 26262, UNECE regulations)

- 3.2.1.2 Fleet utilization optimization demands

- 3.2.1.3 Electric vehicle adoption acceleration

- 3.2.1.4 Advanced driver assistance system integration

- 3.2.1.5 Cost reduction pressures in maintenance operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Software-defined vehicle architecture adoption

- 3.2.3.2 5G and advanced connectivity deployment

- 3.2.3.3 Autonomous vehicle development

- 3.2.3.4 Circular economy and sustainability initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By sensor

- 3.11 ROI and business case analysis

- 3.11.1 Total cost of ownership framework

- 3.11.2 Implementation cost structure

- 3.11.3 Quantified benefits assessment

- 3.12 Investment & funding trends analysis

- 3.13 Implementation roadmap framework

- 3.13.1 Phased deployment strategies

- 3.13.2 Integration complexity analysis

- 3.13.3 Change management requirements

- 3.13.4 Success factor identification

- 3.14 Performance benchmarking framework

- 3.14.1 KPI definition and measurement

- 3.14.2 Industry best practice analysis

- 3.14.3 Comparative performance metrics

- 3.14.4 Continuous improvement models

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New application launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Sensor, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Vibration sensor

- 5.3 Temperature sensor

- 5.4 Pressure sensor

- 5.5 Humidity sensor

- 5.6 Acoustic sensor

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Engine health monitoring

- 6.3 Transmission & gearbox monitoring

- 6.4 Battery & electrical system monitoring

- 6.5 Tire & wheel monitoring

- 6.6 Cooling system monitoring

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial sales channels

- 7.3.1 Light commercial sales channels (LCV)

- 7.3.2 Medium commercial sales channels (MCV)

- 7.3.3 Heavy commercial sales channels (HCV)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aptiv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 Infineon Technologies

- 10.1.5 NXP Semiconductors

- 10.1.6 Robert Bosch

- 10.1.7 TE Connectivity

- 10.1.8 ZF Friedrichshafen

- 10.1.9 Murata

- 10.2 Regional Players

- 10.2.1 Allegro MicroSystems

- 10.2.2 KEYENCE

- 10.2.3 Magna International

- 10.2.4 Melexis

- 10.2.5 NIRA Dynamics

- 10.2.6 Sensata Technologies

- 10.2.7 Siemens

- 10.2.8 Valeo

- 10.3 Emerging Players / Disruptors

- 10.3.1 Augury Systems

- 10.3.2 C3.ai

- 10.3.3 Delphi Technologies

- 10.3.4 Predii

- 10.3.5 Presenso Analytics

- 10.3.6 Revvo Technologies

- 10.3.7 Samsara

- 10.3.8 Tactile Mobility

- 10.3.9 Uptake Technologies