|

시장보고서

상품코드

1871141

멤리스터 기반 자동차 메모리 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Memristor-Based Automotive Memory Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

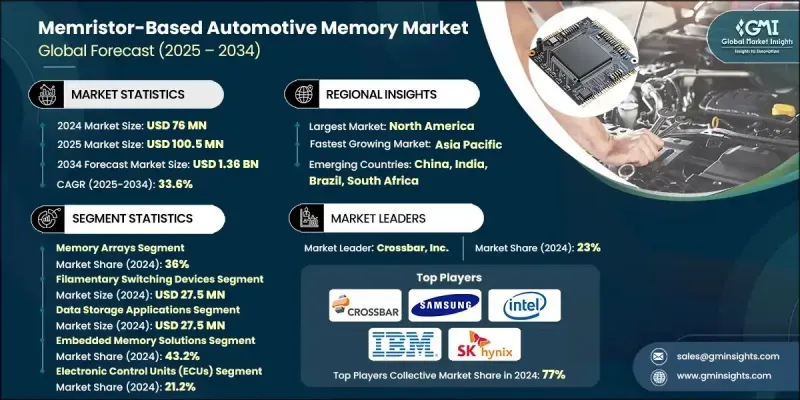

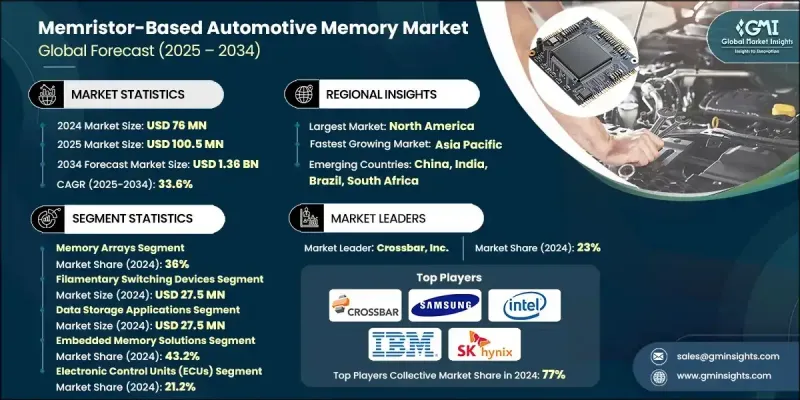

세계의 멤리스터 기반 자동차 메모리 시장은 2024년 7,600만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 33.6%로 성장해 13억 6,000만 달러에 달할 것으로 예측됩니다.

멤리스터 기술과 재료의 지속적인 진보가 자동차 메모리 상황을 재구성하고 있습니다. 혁신적인 금속 산화물과 스핀트로닉스 구조를 포함한 저항 스위칭 재료의 발전으로 성능, 내구성 및 확장성이 향상되고 멤리스터는 기존 메모리 기술보다 훨씬 우수한 성능을 발휘합니다. 새로운 제조 기술을 통해 엠리스터를 마이크로컨트롤러 및 시스템 온 칩(SoC) 아키텍처에 원활하게 통합할 수 있어 처리 속도 향상과 저지연을 실현할 수 있습니다. 아날로그 멤리스터의 연구 개발도 자동차 환경에서 실시간 AI 처리의 효율화를 촉진하고 있습니다. 이러한 혁신을 통해 엠리스터의 응용 범위는 기존의 자동차 시스템에서 고도의 자율 항행과 AI 구동 컴퓨팅으로 확대되어 차세대 자동차 메모리의 기반 기술로서 지위를 확립하고 있습니다. ADAS(첨단 운전 지원 시스템) 및 자율주행기술의 대두로 고속, 적은 전력소비, 비휘발성 메모리부품에 대한 수요가 가속화되고 있습니다. 이러한 시스템은 대량의 센서 데이터를 즉시 분석해야 하기 때문에 멤리스터의 뛰어난 속도와 저에너지 소비는 지각, 계획, 예측 시스템 최적화와 같은 실시간 의사결정 작업에 이상적입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7,600만 달러 |

| 예측 금액 | 13억 6,000만 달러 |

| CAGR | 33.6% |

메모리 어레이 부문은 2024년에 36%의 점유율을 차지했며, 커넥티드 자동차가 콤팩트하고 에너지 절약되고 대용량 데이터 스토리지 솔루션을 점점 더 필요로 하는 가운데 견조한 성장을 보이고 있습니다. 이러한 메모리 어레이는 현대 자동차 네트워크에서 인포테인먼트, ADAS 및 엣지 컴퓨팅 기능을 지원하는 데 필수적입니다. 제조업체는 까다로운 자동차 신뢰성 기준을 충족하면서 극단적인 온도 조건 하에서도 일관된 성능을 유지하는 확장 가능하고 내구성 있는 어레이 개발에 주력하고 있습니다.

필라멘트 스위칭 장치 부문은 2024년 2,750만 달러의 수익을 창출했습니다. 이러한 디바이스의 채용 확대는 고속 스위칭 능력, 에너지 효율, 내결함성에 의해 추진되고 있으며, 차세대 지능형 자동차 시스템에 이상적입니다. 필라멘트 스위칭 장치는 특히 실시간 계산 및 안전성을 보장해야 하는 시스템에서 중요한 차량 용도에서 보다 신속한 데이터 전송, 저지연 및 높은 신뢰성을 제공합니다. 그 확장성과 내구성은 성능과 지속가능성에 초점을 맞춘 미래의 자동차 전자 아키텍처에서 우선적인 선택이 되고 있습니다.

북미의 멤리스터 기반 자동차 메모리 시장은 2024년 34.2%의 점유율을 차지했습니다. 이 지역의 강한 존재감은 자율주행차 및 커넥티드카의 보급, 첨단 자동차 전자기기, 그리고 충실한 연구개발 인프라에 의해 지원되고 있습니다. 북미 전역에서의 성장 기회는 ADAS(첨단 운전 지원 시스템), 인포테인먼트, 자율 이동 플랫폼을 위해 설계된 메모리 기술의 혁신에 의해 촉진되고 있습니다. 유리한 정부 프로그램, 정비된 인프라, 첨단 차량 기술에 대한 소비자의 조기 수용이 결합되어, 멤리스터 기반 자동차 메모리 솔루션의 추가 확대를 위한 비옥한 환경이 갖추어지고 있습니다.

멤리스터 기반 자동차 메모리 시장에서 활동하는 주요 기업으로는 Intel Corporation, Crossbar, Inc., Fujitsu Ltd., IBM Corporation, Micron Technology, Inc., SK Hynix, Inc., Toshiba Corporation, eMemory Technology Inc., Sony Corporation, Renesas Electronics Corporation, Panasonic Holdings Corporation, Weebit Nano Ltd., Samsung Electronics Co., Ltd., Rambus Inc., Hewlett Packard Enterprise (HPE), STMicroelectronics N.V., Everspin Technologies, Inc., Knowm Inc., Western Digital Corporation 등을 들 수 있습니다. 주요 기업은 지속적인 혁신, 생산 능력 확대, 전략적 제휴를 통해 시장에서의 입지를 강화하고 있습니다. 많은 기업들이 확장성, 스위칭 속도, 내구성 향상에 초점을 맞추고, 멤리스터의 성능 강화를 위한 연구 개발에 많은 투자를 하고 있습니다. 반도체 제조업체나 자동차 제조업체와의 전략적 제휴나 파트너십에 의해 차세대 차량 시스템에의 멤리스터 기술 통합이 진행되고 있습니다. 여러 기업이 자율주행 차량 및 전기자동차에 최적화된 맞춤형 에너지 절약형 메모리 아키텍처를 개발하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 멤리스터 기술 및 재료 진보

- ADAS 및 자율주행차에 대한 수요 증가

- 에너지 효율과 열 관리에 대한 주목 증가

- 커넥티드카에서 엣지 컴퓨팅과 IoT 통합

- 업계의 잠재적 위험 및 과제

- 높은 개발 및 제조 비용

- 한정적인 표준화와 호환성 문제

- 시장 기회

- 하이브리드 메모리 아키텍처 개발

- 특정 자동차 기능을 위한 맞춤형

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 기술 상황

- 현재의 동향

- 신흥기술

- 파이프라인 분석

- 미래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 메모리 컨트롤러

- 메모리 어레이

- 뉴로모픽 프로세서

- 보안 모듈

- 기타

제6장 시장 추계 및 예측 : 기술 아키텍처별, 2021-2034년

- 주요 동향

- 필라멘터리 스위칭 디바이스

- 상변화 메모리(PCM)

- 자기 터널 접합(MTJ) 디바이스

- 강유전체 메모리 디바이스

제7장 시장 추계 및 예측 : 기능 용도별, 2021-2034년

- 주요 동향

- 데이터 스토리지 용도

- 인메모리 컴퓨팅 용도

- 보안 및 인증 용도

제8장 시장추계 및 예측 : 통합 접근법별, 2021-2034년

- 주요 동향

- 임베디드 메모리 솔루션

- 이산 메모리 컴포넌트

- 하이브리드 시스템 솔루션

제9장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 전자제어유닛(ECU)

- ADAS(첨단 운전 지원 시스템)

- 자율주행 시스템

- 인포테인먼트 시스템

- 파워트레인 제어 시스템

- 안전 시스템

- 동체 제어 시스템

- 커넥티비티 및 텔레매틱스 시스템

- 기타

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Crossbar, Inc.

- eMemory Technology Inc.

- Everspin Technologies, Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise(HPE)

- IBM Corporation

- Intel Corporation

- Knowm Inc.

- Micron Technology, Inc.

- Panasonic Holdings Corporation

- Rambus Inc.

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.

- SK Hynix, Inc.

- Sony Corporation

- STMicroelectronics NV

- Toshiba Corporation

- Weebit Nano Ltd.

- Western Digital Corporation

The Global Memristor-Based Automotive Memory Market was valued at USD 76 million in 2024 and is estimated to grow at a CAGR of 33.6% to reach USD 1.36 Billion by 2034.

Continuous advancements in memristor technologies and materials are reshaping the automotive memory landscape. Progress in resistive switching materials, including innovative metal oxides and spintronic structures, has enhanced performance, durability, and scalability, making memristors far more capable than conventional memory technologies. New manufacturing approaches allow seamless integration of memristors into microcontrollers and system-on-chip (SoC) architectures, achieving faster processing and lower latency. Research developments in analog memristors are also enabling more efficient real-time AI processing within vehicles. These innovations are expanding the applications of memristors from traditional in-vehicle systems to advanced autonomous navigation and AI-driven computing, positioning them as a cornerstone of next-generation automotive memory. The rise of Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies is accelerating demand for fast, power-efficient, and non-volatile memory components. Since these systems depend on instant analysis of large volumes of sensor data, memristors' superior speed and low energy usage are ideal for real-time decision-making tasks such as perception, planning, and predictive system optimization.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76 Million |

| Forecast Value | $1.36 Billion |

| CAGR | 33.6% |

The memory arrays segment held a 36% share in 2024 and is experiencing robust growth as connected vehicles increasingly require compact, energy-saving, and high-capacity data storage solutions. These memory arrays are essential for supporting infotainment, ADAS, and edge computing functions within modern automotive networks. Manufacturers are focusing on developing scalable and durable arrays that maintain consistent performance in extreme temperature conditions while meeting stringent automotive reliability standards.

The filamentary switching devices segment generated USD 27.5 million in 2024. Growing adoption of these devices is driven by their rapid switching capability, energy efficiency, and resilience, which make them ideal for next-generation intelligent automotive systems. Filamentary switching devices enable quicker data transmission, lower latency, and higher reliability in critical vehicle applications, particularly in systems that demand real-time computation and safety assurance. Their scalability and endurance are making them a preferred choice for future automotive electronic architectures focused on performance and sustainability.

North America Memristor-Based Automotive Memory Market held a 34.2% share in 2024. The region's strong presence is supported by widespread adoption of autonomous and connected vehicles, advanced automotive electronics, and extensive R&D infrastructure. Growth opportunities across North America are being fueled by innovation in memory technologies designed for ADAS, infotainment, and autonomous mobility platforms. Favorable government programs, developed infrastructure, and early consumer acceptance of advanced vehicle technologies are creating a fertile environment for further expansion of memristor-based automotive memory solutions.

Major companies active in the Memristor-Based Automotive Memory Market include Intel Corporation, Crossbar, Inc., Fujitsu Ltd., IBM Corporation, Micron Technology, Inc., SK Hynix, Inc., Toshiba Corporation, eMemory Technology Inc., Sony Corporation, Renesas Electronics Corporation, Panasonic Holdings Corporation, Weebit Nano Ltd., Samsung Electronics Co., Ltd., Rambus Inc., Hewlett Packard Enterprise (HPE), STMicroelectronics N.V., Everspin Technologies, Inc., Knowm Inc., and Western Digital Corporation. Leading participants in the Memristor-Based Automotive Memory Market are strengthening their market position through continuous technological innovation, capacity expansion, and strategic collaboration. Many companies are investing heavily in R&D to enhance memristor performance, focusing on improving scalability, switching speed, and endurance. Strategic alliances and partnerships with semiconductor manufacturers and automotive OEMs are helping them integrate memristor technology into next-generation vehicle systems. Several players are developing customized, energy-efficient memory architectures optimized for autonomous and electric vehicles.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vector trends

- 2.2.3 Delivery method trends

- 2.2.4 Gene type trends

- 2.2.5 Indication trends

- 2.2.6 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in memristor technology and materials

- 3.2.1.2 Growing demand for ADAS and autonomous vehicles

- 3.2.1.3 Rising focus on energy efficiency and thermal management

- 3.2.1.4 Integration of edge computing and IoT in connected vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and manufacturing costs

- 3.2.2.2 Limited standardization and compatibility issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of hybrid memory architectures

- 3.2.3.2 Customization for specific automotive functions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Memory controllers

- 5.3 Memory arrays

- 5.4 Neuromorphic processors

- 5.5 Security modules

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology Architecture, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Filamentary switching devices

- 6.3 Phase Change Memory (PCM)

- 6.4 Magnetic Tunnel Junction (MTJ) devices

- 6.5 Ferroelectric memory devices

Chapter 7 Market Estimates and Forecast, By Functional Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Data storage applications

- 7.3 In-memory computing applications

- 7.4 Security and authentication applications

Chapter 8 Market Estimates and Forecast, By Integration Approach, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Embedded memory solutions

- 8.3 Discrete memory components

- 8.4 Hybrid system solutions

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Electronic Control Units (ECUs)

- 9.3 Advanced Driver Assistance Systems (ADAS)

- 9.4 Autonomous driving systems

- 9.5 Infotainment systems

- 9.6 Powertrain control systems

- 9.7 Safety systems

- 9.8 Body control systems

- 9.9 Connectivity/telematics systems

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Crossbar, Inc.

- 11.2 eMemory Technology Inc.

- 11.3 Everspin Technologies, Inc.

- 11.4 Fujitsu Ltd.

- 11.5 Hewlett Packard Enterprise (HPE)

- 11.6 IBM Corporation

- 11.7 Intel Corporation

- 11.8 Knowm Inc.

- 11.9 Micron Technology, Inc.

- 11.10 Panasonic Holdings Corporation

- 11.11 Rambus Inc.

- 11.12 Renesas Electronics Corporation

- 11.13 Samsung Electronics Co., Ltd.

- 11.14 SK Hynix, Inc.

- 11.15 Sony Corporation

- 11.16 STMicroelectronics N.V.

- 11.17 Toshiba Corporation

- 11.18 Weebit Nano Ltd.

- 11.19 Western Digital Corporation