|

시장보고서

상품코드

1871169

3D 프린팅 의료기기 프로토타이핑 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)3D Printed Medical Device Prototyping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

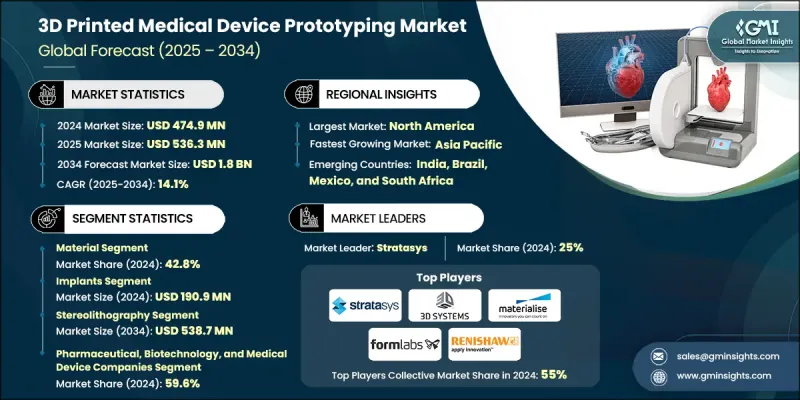

세계의 3D 프린팅 의료기기 프로토타이핑 시장은 2024년에 4억 7,490만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 14.1%를 나타낼 것으로 예측되며 18억 달러에 달할 전망입니다.

이러한 꾸준한 성장은 정형외과 및 치과 질환의 증가, 적층 제조 기술의 지속적인 발전, 의료 혁신에 대한 투자 확대, 의료 부문에서의 3D 프린팅 활용 확대 등에 기인합니다. 3D 프린팅 의료 기기 프로토타이핑은 적층 제조 기술을 활용해 의료 기기의 예비 모델을 개발하여 본격적인 생산 전에 설계 정확도, 적합성 및 기능성을 테스트하는 과정을 포함합니다. 이 프로세스는 제품 개발을 가속화하고 개별 환자에 대한 맞춤화를 지원하며 효율적인 설계 검증을 보장합니다. 특히 수술 전 계획 단계에서 유용하며, 의료진은 환자 맞춤형 프로토타입을 제작해 임플란트 정확도를 높이고 수술 시간을 단축하며 회복 결과를 개선할 수 있습니다. 신속한 반복 작업과 실시간 테스트를 가능케 하는 3D 프린팅은 의료 기기가 엄격한 성능 및 생체 적합성 기준을 충족하도록 보장하여 시장 출시를 가속화하고 정밀도 중심의 의료 혁신을 가능하게 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4억 7,490만 달러 |

| 예측 금액 | 18억 달러 |

| CAGR | 14.1% |

재료 부문은 2024년 42.8%의 점유율을 기록했으며 예측 기간 내내 우위를 유지할 것으로 전망됩니다. 재료는 프로토타입의 신뢰성, 기능성 및 안전성의 기반을 형성합니다. 첨단 금속, 플라스틱 및 생체재료 중에서 선택할 수 있는 능력은 제조업체가 의료 응용 부문에서 엄격한 생체 적합성, 내구성 및 멸균 기준을 충족할 수 있게 합니다. 이 부문은 적층 제조 부문의 혁신과 맞춤형 의료에 대한 수요 증가로 인해 지속적으로 확장되고 있습니다. 열가소성 플라스틱 및 광중합체 부문의 신흥 발전은 재료의 유연성, 정밀도 및 멸균 성능을 향상시켜 의료 프로토타이핑에서의 광범위한 사용을 더욱 뒷받침하고 있습니다.

스테레오리소그래피 부문은 2034년까지 5억 3,870만 달러 규모에 이를 것으로 예상됩니다. 이 기술은 레이저 기반 공정을 활용하여 액체 수지를 연속적인 층으로 고형화함으로써 탁월한 표면 품질과 치수 정밀도를 지닌 프로토타입을 생산합니다. 이 기술은 정밀도와 매끄러움이 중요한 복잡한 의료 부품 제작에 이상적인 선택입니다. 정교하고 매우 정확한 모델을 제공할 수 있기 때문입니다. 또한 스테레오리소그래피가 생체 적합성 재료와 호환된다는 점은 의료 프로토타이핑 부문에서 지속적인 채택을 뒷받침합니다.

미국의 3D 프린팅 의료기기 프로토타이핑 시장은 2024년 1억 7,720만 달러로 평가되었습니다. 이 나라의 성장은 성인 인구의 상당한 비율에 영향을 미치는 정형외과 및 치과 질환의 발병률 상승에 의해 뒷받침됩니다. 의료기관과 의료기기 제조업체가 제품 개발 워크플로우에 3D 프린팅를 통합하는 동안, 미국은 혁신과 생산의 주요 기지로 남아 있습니다. 선진적인 제조 능력, 견고한 규제 인프라, 증가하는 의료 부문의 연구 개발 투자가 융합됨으로써 의료기기 프로토타이핑에 있어서 미국의 리더십이 확고해지고 있습니다.

세계의 3D 프린팅 의료기기 프로토타이핑 시장의 정세를 주도하는 주요 기업으로는 레니쇼, 3D 시스템즈, 프로트라보, 스트라타시스, 머티리얼라이즈, 엔비전 TEC, 파라곤 메디컬, 솔리드 웍스, 엠파이어 그룹 USA, 폼랩, 오가노보 홀딩스, 아캄, 인벤테크 등 3D 프린팅 의료기기 프로토 타이핑 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 여러 전략을 실시했습니다. 재료 성능과 프린팅 정밀도 향상을 위해 연구 개발에 많은 투자를 실시했습니다. 의료기관이나 연구기관과의 전략적 제휴는 임상 검증의 확대와 채용의 가속에 공헌하고 있습니다. 많은 기업들이 증가하는 수요에 대응하기 위해 세계 생산 능력과 유통 네트워크의 확대에 주력하고 있습니다. 합병, 인수, 파트너십을 활용하여 선진기술의 통합과 제품 포트폴리오의 확충을 도모하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 정형외과 및 치과 질환의 높은 유병률

- 3D 프린팅 기술의 지속적인 발전

- 의료 혁신 및 디지털 제조 부문 투자 증가

- 3D 프린팅 의료기기의 확대 적용

- 업계의 잠재적 억제요인 및 과제

- 엄격한 규제 준수 요건

- 원자재 비용 상승

- 시장 기회

- 3D 프린팅과 의료 영상 및 CAD 소프트웨어의 통합

- 생체흡수성 및 환자 맞춤형 임플란트 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 발전

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 상환 시나리오

- 가격 분석(2024년)

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 기기

- 3D 프린터

- 3D 바이오프린터

- 소프트웨어

- 재료

- 플라스틱

- 포토폴리머

- 열가소성 플라스틱

- 금속 및 합금

- 티타늄

- 스테인리스 스틸

- 코발트-크롬

- 생체 재료

- 세라믹

- 기타 재료

- 플라스틱

- 서비스

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 보철물

- 임플란트

- 두개악안면 임플란트

- 치과 임플란트

- 정형외과 임플란트

- 외과용 가이드

- 조직 공학 제품

- 웨어러블 의료기기

- 기타 용도

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 스테레오리소그래피

- 융합 적층 모델링

- 전자빔 용융

- 레이저 소결

- 바인더 제팅

- 디지털 광처리

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원 및 의료 기관

- 제약, 생명공학 및 의료기기 기업

- 기타 최종 용도

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 3D Systems

- Arcam

- COSA

- Empire Group USA

- Envision TEC

- EOS

- Formlabs

- Inventex Medical

- Materialise

- Organovo Holdings

- Paragon Medical

- Proto Labs

- Renishaw

- SolidWorks

- Stratasys

The Global 3D Printed Medical Device Prototyping Market was valued at USD 474.9 million in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 1.8 Billion by 2034.

The consistent growth is attributed to the increasing number of orthopedic and dental conditions, ongoing advancements in additive manufacturing, rising investments in healthcare innovation, and the expanding use of 3D printing in medical applications. 3D printed medical device prototyping involves developing preliminary models of medical instruments using additive manufacturing to test design accuracy, fit, and functionality prior to full-scale production. This process accelerates product development, supports customization for individual patients, and ensures efficient design validation. It is especially beneficial in pre-surgical planning, where clinicians can create patient-specific prototypes that improve implant accuracy, shorten surgical durations, and enhance recovery outcomes. By enabling rapid iteration and real-time testing, 3D printing ensures medical devices meet rigorous performance and biocompatibility standards, allowing faster market readiness and precision-driven innovation in healthcare.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $474.9 Million |

| Forecast Value | $1.8 Billion |

| CAGR | 14.1% |

The material segment held a 42.8% share in 2024 and is projected to remain dominant throughout the forecast period. Materials form the foundation of prototype reliability, functionality, and safety. The ability to select from advanced metals, plastics, and biomaterials enables manufacturers to meet strict biocompatibility, durability, and sterilization standards in medical applications. This segment continues to expand due to breakthroughs in additive manufacturing and the growing demand for personalized healthcare. Emerging developments in thermoplastics and photopolymers are enhancing material flexibility, precision, and sterilization performance, further supporting their extensive use in medical prototyping.

The stereolithography segment is expected to reach USD 538.7 million by 2034. This technique utilizes a laser-based process that solidifies liquid resin in successive layers, producing prototypes with exceptional surface quality and dimensional precision. The technology's ability to deliver intricate and highly accurate models makes it an ideal choice for creating complex medical components where precision and smoothness are crucial. Furthermore, the compatibility of stereolithography with biocompatible materials reinforces its continued adoption in healthcare prototyping applications.

United States 3D Printed Medical Device Prototyping Market was valued at USD 177.2 million in 2024. The country's growth is fueled by the rising occurrence of orthopedic and dental conditions affecting a significant portion of the adult population. With healthcare organizations and device manufacturers integrating 3D printing into product development workflows, the U.S. remains a key hub for innovation and production. The convergence of advanced manufacturing capabilities, strong regulatory infrastructure, and increasing healthcare R&D investment solidifies the nation's leadership in medical device prototyping.

Prominent companies shaping the Global 3D Printed Medical Device Prototyping Market landscape include Renishaw, 3D Systems, Proto Labs, Stratasys, Materialise, Envision TEC, Paragon Medical, SolidWorks, Empire Group USA, Formlabs, Organovo Holdings, Arcam, Inventex Medical, COSA, and EOS. Leading companies in the 3D Printed Medical Device Prototyping Market are implementing multiple strategies to strengthen their market position. They are investing heavily in research and development to enhance material performance and printing precision. Strategic collaborations with healthcare institutions and research organizations are helping expand clinical validation and accelerate adoption. Many firms are focusing on expanding their global production capacities and distribution networks to meet rising demand. Mergers, acquisitions, and partnerships are being leveraged to integrate advanced technologies and broaden product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trend

- 2.2.4 Technology trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High prevalence of orthopedic and dental disorders

- 3.2.1.2 Continuous technological advancement in 3D printing technologies

- 3.2.1.3 Rising investment in healthcare innovation and digital manufacturing

- 3.2.1.4 Growing application of 3D printed medical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance requirements

- 3.2.2.2 High cost of raw materials

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of 3D printing with medical imaging and CAD software

- 3.2.3.2 Development of bioresorbable and patient-specific implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Equipment

- 5.2.1 3D printer

- 5.2.2 3D bioprinter

- 5.3 Software

- 5.4 Materials

- 5.4.1 Plastic

- 5.4.1.1 Photopolymers

- 5.4.1.2 Thermoplastics

- 5.4.2 Metals and alloys

- 5.4.2.1 Titanium

- 5.4.2.2 Stainless steel

- 5.4.2.3 Cobalt-chromium

- 5.4.3 Biomaterials

- 5.4.4 Ceramic

- 5.4.5 Other materials

- 5.4.1 Plastic

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Applications, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Prosthetics

- 6.3 Implants

- 6.3.1 Craniomaxillofacial implants

- 6.3.2 Dental implants

- 6.3.3 Orthopedic implants

- 6.4 Surgical guides

- 6.5 Tissue engineered products

- 6.6 Wearable medical devices

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stereolithography

- 7.3 Fused deposition modeling

- 7.4 Electron beam melting

- 7.5 Laser sintering

- 7.6 Binder jetting

- 7.7 Digital light processing

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and healthcare institutions

- 8.3 Pharmaceutical, biotechnology, and medical device companies

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3D Systems

- 10.2 Arcam

- 10.3 COSA

- 10.4 Empire Group USA

- 10.5 Envision TEC

- 10.6 EOS

- 10.7 Formlabs

- 10.8 Inventex Medical

- 10.9 Materialise

- 10.10 Organovo Holdings

- 10.11 Paragon Medical

- 10.12 Proto Labs

- 10.13 Renishaw

- 10.14 SolidWorks

- 10.15 Stratasys

(주말 및 공휴일 제외)