|

시장보고서

상품코드

1871172

정밀 발효 바이오리액터 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Precision Fermentation Bioreactors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

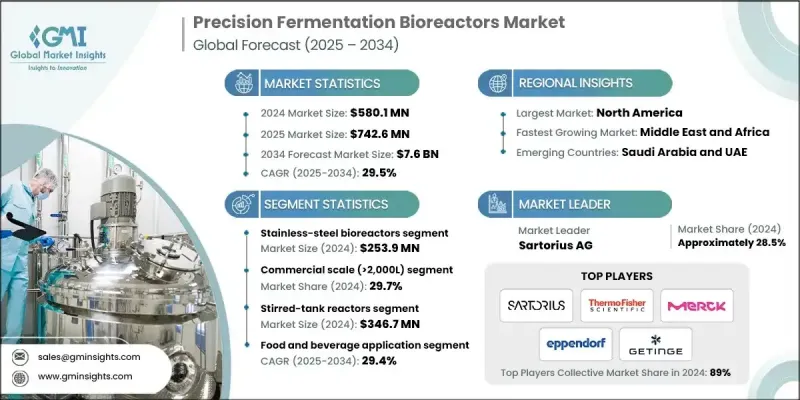

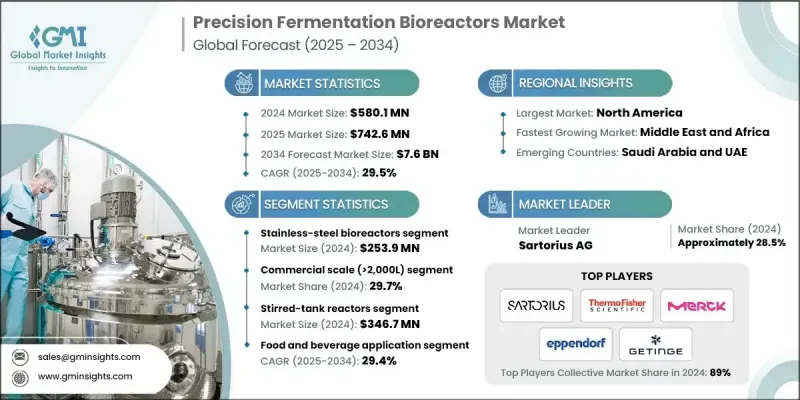

세계의 정밀 발효 바이오리액터 시장은 2024년 5억 8,010만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 29.5%로 성장하여 76억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 지속 가능하고 동물 유래가 아닌 단백질 및 효소 생산에 대한 수요 증가가 있습니다. 소비자가 식물 유래·윤리적인 대체품을 선택하는 경향이 강해지고 있는 가운데, 정밀 발효 기술은 동물에 의존하지 않고 유제품 대체품이나 단백질 분리물 등의 고부가가치 원료를 생산하는 지속 가능하고 확장성이 있는 해결책으로서 대두하고 있습니다. 환경 책임과 윤리적 조달에 대한 관심이 높아짐에 따라 식품 및 바이오테크놀러지 양 분야에서의 도입을 가속화하고 있습니다. 또한, 본 기술이 안정적인 제품 품질을 제공하고 기존 단백질 생산의 탄소 발자국을 줄일 수 있다는 점이 미래의 식품 생태계를 지원하는 중요한 기반으로서의 지위를 강화하고 있습니다. 미생물 균주의 설계 기술과 실시간 공정 모니터링의 지속적인 발전으로 발효 시스템의 정확성, 효율성 및 수율이 향상되고 업계의 급속한 성장에 유리한 조건이 갖추어지고 있습니다. 또한 기술 통합, 자동화 및 데이터 분석을 통해 기업은 파일럿 단계에서 상업 생산으로 효율적으로 규모를 확장할 수 있으며 발효 유래 원료의 대량 생산으로의 전환을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 5억 8,010만 달러 |

| 예측 금액 | 76억 달러 |

| CAGR | 29.5% |

2,000L 이상의 상업 규모 부문은 2024년에 2억 3,560만 달러로 평가되었고, 2025년부터 2034년까지 29.7%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 대용량 바이오리액터는 산업 규모의 정밀 발효에 필수적이며 일관되고 고품질의 비용 효율적인 제조 공정을 실현합니다. 상업 규모의 도입이 꾸준히 증가하고 있는 것은 업계가 조사 및 시작 단계에서 대규모로 시장 투입 가능한 생산 단계로 이행하고 있는 것을 나타내고 있습니다. 산업 규모로의 확대는 생산자가 경제적 실현 가능성과 규제 준수를 달성할 수 있다는 확신 증가를 반영하여 다양한 산업 분야에서의 보급을 뒷받침하고 있습니다.

식음료 분야는 정밀 발효에 의해 생산되는 동물 유래가 아닌 단백질, 효소, 향료에 대한 수요 증가를 배경으로 주요 응용 분야 중 하나로 계속되고 있습니다. 지속가능성에 대한 소비자의 의식의 고조와 대체단백질로의 이행이 함께 발효기술을 기반으로 한 기술의 보다 광범위한 채용을 촉진하고 있습니다. 생산자가 더 깨끗하고 지속 가능한 식품 제품을 생산하는이 방법의 장기적인 가능성을 인식함에 따라, 파일럿 규모의 실험은 빠르게 상업 생산 라인으로 발전하고 있습니다.

미국 정밀 발효 바이오리액터 시장은 첨단 R&D 능력, 강력한 산업 연계, 유리한 혁신 생태계에 힘입어 2024년에 큰 점유율을 차지했습니다. 이 국가의 바이오테크놀러지 및 푸드텍 산업은 실험실 배양 단백질, 유제품 대체품, 효소의 상업화를 적극적으로 추진하고 있으며, 대학과 민간 기업이 연계하여 발효 기술의 개량에 임하고 있습니다. 자동화와 디지털 공정 제어의 통합은 발효 시스템의 신뢰성, 생산성 및 일관성을 향상시킵니다.

세계 정밀 발효 바이오리액터 시장의 주요 기업으로는 Merck KGaA (MilliporeSigma), Thermo Fisher Scientific, Sartorius AG, Getinge AB, and Eppendorf AG 등이 있습니다. 정밀 발효 바이오리액터 시장에서 기업의 주요 전략은 혁신, 확장성, 전략적 협력에 중점을 둡니다. 주요 제조업체는 공정 제어, 에너지 효율, 발효 수율 향상을 위해 연구 개발에 많은 투자를 실시했습니다. 식품기술기업이나 바이오테크놀러지기업과의 전략적 제휴는 응용 분야의 확대와 시장투입의 가속에 기여하고 있습니다. 또한 실험실에서 공업 생산까지 유연한 스케일업을 가능하게 하는 모듈식 바이오리액터 설계에도 주력하고 있습니다. 자동화, AI 구동 모니터링, 디지털 트윈 기술의 통합으로 시스템의 정밀도 향상과 운영 비용 절감을 도모하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 공급망의 복잡성

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(주: 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 일회용 바이오리액터

- 스테인리스 스틸 바이오리액터

- 유리 바이오리액터

- 하이브리드 바이오리액터

- 교반기 바이오리액터

- 기타

제6장 시장 추계 및 예측 : 규모별, 2021-2034년

- 주요 동향

- 실험실 규모(50L 미만)

- 파일럿 스케일(50-2,000L)

- 상업 규모(2,000L 초과)

- 소규모 상업용(2,000-10,000L)

- 대규모 상업용(10,000L 초과)

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 교반조형 리액터

- 파동식 및 요동식 바이오리액터

- 버블 컬럼 리액터

- 기타 기술

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 식음료

- 대체 단백질

- 우유 단백질

- 고기 단백질

- 계란 단백질

- 식품 원료

- 효소

- 비타민

- 향료 및 보존료

- 기능성 식품

- 프로바이오틱스 및 프리바이오틱스

- 영양보조식품

- 대체 단백질

- 의약품

- 치료용 단백질

- 백신 및 생물학적 제형

- 의약품용 효소

- 공업 및 화학 분야

- 공업용 효소

- 특수화학제품

- 바이오연료 및 에너지

- 기타

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Sartorius AG

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Eppendorf AG

- Getinge AB

- Pall Corporation(Danaher)

- ABEC Inc.

- Applikon Biotechnology

- Solaris Biotechnology

- Pierre Guerin Technologies

- Perfect Day Inc.

- Impossible Foods Inc.

- TurtleTree Labs

- The EVERY Company

- Motif FoodWorks

- Geltor Inc.

- Clara Foods(The EVERY Company)

- Novonesis(formerly Novozymes)

- Ginkgo Bioworks

- Zymergen(Ginkgo Bioworks)

- Synthetic Biologics Inc.

- Amyris Inc.

- Formo(formerly LegenDairy Foods)

- Change Foods

- New Culture Inc.

- Remilk Ltd.

- Imagindairy Ltd.

- Shiru Inc.

- Tetra Pak

- Culture Biosciences

The Global Precision Fermentation Bioreactors Market was valued at USD 580.1 million in 2024 and is estimated to grow at a CAGR of 29.5% to reach USD 7.6 Billion by 2034.

Market expansion is propelled by the increasing preference for sustainable and animal-free production of proteins and enzymes. As consumers increasingly choose plant-based and ethical alternatives, precision fermentation has emerged as a sustainable and scalable solution for producing high-value ingredients such as dairy analogs and protein isolates without relying on animals. The growing emphasis on environmental responsibility and ethical sourcing is accelerating adoption in both food and biotechnology sectors. Furthermore, the technology's ability to deliver consistent product quality and reduce the carbon footprint of traditional protein production strengthens its position as a key enabler of the future food ecosystem. Continuous progress in microbial strain engineering and real-time process monitoring is also improving the precision, efficiency, and yield of fermentation systems, creating favorable conditions for rapid industry growth. Additionally, technological integration, automation, and data analytics are helping companies scale from pilot to commercial operations efficiently, supporting the shift toward mass production of fermentation-derived ingredients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $580.1 million |

| Forecast Value | $7.6 Billion |

| CAGR | 29.5% |

The commercial-scale segment > 2,000L was valued at USD 235.6 million in 2024 and is expected to register a CAGR of 29.7% during 2025-2034. Large-volume bioreactors have become essential for industrial-scale precision fermentation, facilitating consistent, high-quality, and cost-effective manufacturing processes. The steady rise in commercial-scale deployment demonstrates the industry's transition from research and prototype phases toward large-scale, market-ready production. The move toward industrial scalability reflects the growing confidence of producers in achieving economic feasibility and regulatory compliance, supporting widespread adoption across various industries.

The food & beverage sector remains one of the leading application areas, driven by increasing demand for animal-free proteins, enzymes, and flavoring agents produced through precision fermentation. Rising consumer awareness regarding sustainability, combined with a shift toward alternative proteins, has encouraged broader adoption of fermentation-based technologies. Pilot-scale experiments are rapidly evolving into commercial production lines as producers recognize the long-term potential of this method for creating cleaner, more sustainable food products.

United States Precision Fermentation Bioreactors Market held a significant share in 2024, supported by advanced R&D capabilities, strong industrial collaboration, and a favorable innovation ecosystem. The country's biotechnology and food-tech industries are actively advancing the commercialization of lab-cultured proteins, dairy substitutes, and enzymes, with universities and private firms collaborating to refine fermentation technologies. The integration of automation and digital process control is improving the reliability, productivity, and consistency of fermentation systems.

Leading players operating in the Global Precision Fermentation Bioreactors Market include Merck KGaA (MilliporeSigma), Thermo Fisher Scientific, Sartorius AG, Getinge AB, and Eppendorf AG. Key strategies adopted by companies in the Precision Fermentation Bioreactors Market focus on innovation, scalability, and strategic collaboration. Major manufacturers are investing heavily in R&D to enhance process control, energy efficiency, and fermentation yield. Strategic partnerships with food-tech and biotech firms are helping expand application areas and accelerate market commercialization. Companies are also emphasizing modular bioreactor designs that allow flexible scaling from laboratory to industrial production. Integration of automation, AI-driven monitoring, and digital twin technologies is improving system precision and reducing operational costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Scale

- 2.2.4 Technology

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021- 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Single-use bioreactors

- 5.3 Stainless steel bioreactors

- 5.4 Glass bioreactors

- 5.5 Hybrid bioreactors

- 5.6 Stirred-tank bioreactors

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Scale, 2021- 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Laboratory scale (<50L)

- 6.3 Pilot scale (50L - 2,000L)

- 6.4 Commercial scale (>2,000L)

- 6.4.1 Small commercial (2,000L - 10,000L)

- 6.4.2 Large commercial (>10,000L)

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million, , Units)

- 7.1 Key trends

- 7.2 Stirred-tank reactors

- 7.3 Wave/rocking bioreactors

- 7.4 Bubble column reactors

- 7.5 Other technologies

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million, , Units)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.2.1 Alternative proteins

- 8.2.1.1 Dairy proteins

- 8.2.1.2 Meat proteins

- 8.2.1.3 Egg proteins

- 8.2.2 Food ingredients

- 8.2.2.1 Enzymes

- 8.2.2.2 Vitamins

- 8.2.2.3 Flavors and preservatives

- 8.2.3 Functional foods

- 8.2.3.1 Probiotics and prebiotics

- 8.2.3.2 Nutritional supplements

- 8.2.1 Alternative proteins

- 8.3 Pharmaceutical

- 8.3.1 Therapeutic proteins

- 8.3.2 Vaccines and biologics

- 8.3.3 Pharmaceutical enzymes

- 8.4 Industrial and chemical

- 8.4.1 Industrial enzymes

- 8.4.2 Specialty chemicals

- 8.4.3 Biofuels and energy

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Sartorius AG

- 10.2 Thermo Fisher Scientific Inc.

- 10.3 Merck KGaA

- 10.4 Eppendorf AG

- 10.5 Getinge AB

- 10.6 Pall Corporation (Danaher)

- 10.7 ABEC Inc.

- 10.8 Applikon Biotechnology

- 10.9 Solaris Biotechnology

- 10.10 Pierre Guerin Technologies

- 10.11 Perfect Day Inc.

- 10.12 Impossible Foods Inc.

- 10.13 TurtleTree Labs

- 10.14 The EVERY Company

- 10.15 Motif FoodWorks

- 10.16 Geltor Inc.

- 10.17 Clara Foods (The EVERY Company)

- 10.18 Novonesis (formerly Novozymes)

- 10.19 Ginkgo Bioworks

- 10.20 Zymergen (Ginkgo Bioworks)

- 10.21 Synthetic Biologics Inc.

- 10.22 Amyris Inc.

- 10.23 Formo (formerly LegenDairy Foods)

- 10.24 Change Foods

- 10.25 New Culture Inc.

- 10.26 Remilk Ltd.

- 10.27 Imagindairy Ltd.

- 10.28 Shiru Inc.

- 10.29 Tetra Pak

- 10.30 Culture Biosciences