|

시장보고서

상품코드

1871186

자동차용 OTA(Over-The-Air) 하드웨어 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Over-the-Air (OTA) Update Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

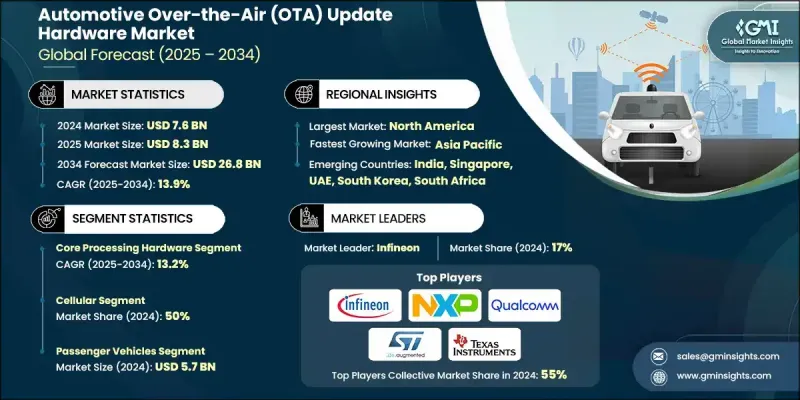

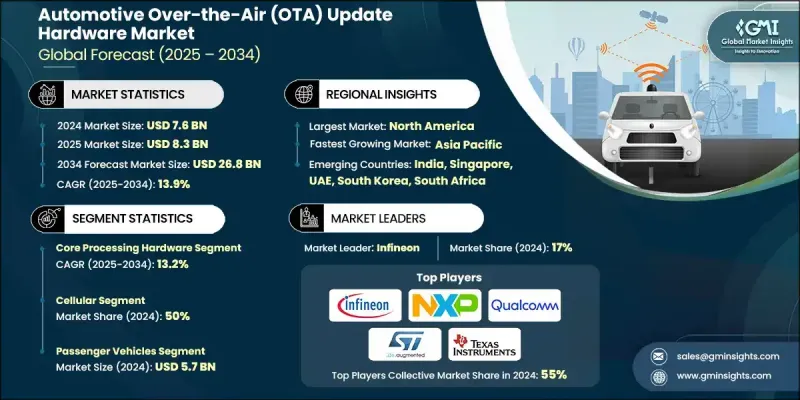

세계의 자동차용 OTA(Over-The-Air) 하드웨어 시장은 2024년 76억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 13.9%로 성장하여 268억 달러에 이를 것으로 예측됩니다.

자동차 산업은 소프트웨어 정의 차량(SDV)으로의 급속한 전환을 추진하고 있으며, 견고한 OTA 하드웨어 인프라에 대한 강한 수요를 창출하고 있습니다. 이 시장에는 코어 프로세싱 유닛, 메모리 및 스토리지 모듈, 연결 하드웨어, 보안 칩, 모니터링 및 진단 시스템과 같은 필수 구성 요소가 포함됩니다. 이러한 요소를 통해 차량 그룹에 대한 OTA 소프트웨어 업데이트, 소프트웨어 기능 활성화 및 사이버 보안 패치 적용이 가능합니다. 커넥티드 자동차 생태계의 상승, 자동차 소프트웨어의 복잡화, 끊임없는 고객 경험의 필요성으로 OTA 하드웨어의 도입이 가속화되고 있습니다. COVID-19는 원격 업데이트의 필요성과 물리적 서비스 센터에 대한 의존도 감소를 부각시켜 OTA 기능의 중요성을 강조했습니다. 제조업체가 차량 라이프사이클 관리를 강화하고 유지보수로 인한 가동 중지 시간을 줄이기 위해 OTA 하드웨어는 세계 자동차 제조업체들에게 중요한 투자 대상으로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 76억 달러 |

| 예측 금액 | 268억 달러 |

| CAGR | 13.9% |

시장에서는 5G 셀룰러 네트워크, Wi-Fi 6/6E, 위성 통신, 저전력 광역 네트워크(LPWAN) 기술 등 첨단 연결 솔루션의 통합이 급속히 진행되고 있습니다. 이러한 네트워크는 보다 빠르고 안정적인 OTA 업데이트를 제공하며 실시간 V2X(Vehicle-to-Everything)를 지원합니다. 멀티 라디오 연결 하드웨어가 장착된 차량은 신호 강도, 대역폭 요구 사항 및 운영 비용을 기반으로 네트워크를 지능적으로 전환하여 업데이트 및 진단을 위한 일관된 통신을 보장합니다.

코어 프로세싱 하드웨어 부문은 35%의 점유율을 차지하고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 13.2%를 보일 것으로 예측됩니다. 이 부문에는 고성능 자동차 프로세서, 마이크로컨트롤러, 시스템 온칩(SoC) 플랫폼 및 차량 용도용으로 설계된 전용 컴퓨팅 유닛이 포함됩니다. 복잡한 소프트웨어 업데이트 관리, 사이버 보안 검증, 다양한 시스템 기능의 효율적인 조정에는 강력한 처리 능력이 필수적입니다. 한편, 셀룰러 접속은 15.1%의 연평균 복합 성장률(CAGR)로 성장해 시장의 49.4%를 차지할 것으로 예측되고 있습니다. 이는 미션 크리티컬 OTA 기능을 지원할 수 있는 신뢰할 수 있는 고대역폭 네트워크의 필요성으로 인한 것입니다. 셀룰러 기술은 캐리어 등급 신뢰성, 세계 커버리지, 중요한 업데이트를 위한 안전한 구현을 제공합니다.

아시아태평양의 자동차용 OTA(Over-The-Air) 하드웨어 시장은 2024년 41%의 점유율을 차지했으며 15.1%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 지역은 대규모 자동차 생산, 전기자동차의 급속한 보급, 커넥티드카 기술을 촉진하는 정부의 규제에 의해 혜택을 받고 있습니다. 중국의 향후 기준과 같은 규제 요건으로 인해 자동차 제조업체는 신차에 완전한 OTA 하드웨어 기능을 구현할 수밖에 없으며 OTA 하드웨어 공급업체에게 큰 기회가 탄생했습니다.

자동차용 OTA(Over-The-Air) 하드웨어 시장의 주요 기업으로는 Intel, Broadcom, Qualcomm, Infineon, NXP Semiconductors, STMicroelectronics, Texas Instruments, Panasonic, Murata Manufacturing, and Nordic Semiconductor. 등을 들 수 있습니다. 각 회사는 소프트웨어 정의 차량 수요 증가에 대응하기 위해 처리 및 연결 하드웨어의 혁신에 주력하고 있습니다. 많은 기업들이 OTA의 성능과 사이버 보안을 강화하기 위해 멀티 라디오 통신 솔루션, 보안 프로세서, 통합 시스템 온칩 설계에 대한 투자를 추진하고 있습니다. 자동차 제조업체와 Tier 1 공급업체와의 전략적 제휴는 제품 채용 촉진과 세계 전개를 가속화하고 있습니다. 특히 아시아태평양의 지역 확대는 높은 볼륨의 자동차 시장에 대한 접근과 규제 주도의 기회를 확보합니다. 각 회사는 경쟁 우위를 유지하기 위해 차세대 5G 및 위성 통신 기술의 연구 개발에도 투자하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- SoC 제공업체

- 마이크로컨트롤러(MCU) 제조업체

- 연결성 및 네트워크 모듈 공급업체

- 반도체 파운드리

- OTA 소프트웨어 플랫폼 제공업체

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 디스랩터

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 자동차 산업에서의 디지털 전환

- IoT 디바이스의 보급과 연방 사이버 보안 지령

- 엣지 AI 통합과 칩렛 아키텍처 채용

- 5G 네트워크의 전개와 강화된 접속성 인프라

- 업계의 잠재적 위험 및 과제

- 반도체 공급망의 집중화와 지정학적 리스크

- 규제의 복잡성과 복수 관할 구역에서의 컴플라이언스 과제

- 시장 기회

- 스마트 시티의 인프라 근대화

- 지방 접속 솔루션과 위성 기반 OTA 전달

- 성장 촉진요인

- 기술 동향과 혁신 생태계

- 현행 기술

- 칩렛 기반 OTA 시스템과 타기종 통합

- 3D 패키징 및 첨단 상호 연결 기술

- 지능형 업데이트를 위한 뉴로모픽 컴퓨팅 통합

- 양자 내성 보안 하드웨어 구현

- 신흥기술

- 6G 네트워크 준비 및 초저지연 업데이트

- 세계 커버리지를 위한 위성 별자리 통합

- 안전한 갱신을 위한 Li-Fi 및 광 무선 통신

- 메쉬 네트워크와 피어 투 피어 업데이트 배포

- 현행 기술

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 특허 분석

- 코스트 내역 분석

- 가격 동향

- 하드웨어 부품의 가격 변동 요인

- 총소유비용 모델

- 가치에 따른 가격 설정 전략

- 비용 최적화 기회

- 투자 및 자금조달

- 정부 투자 프로그램

- 프라이빗 에퀴티 및 벤처 캐피탈의 동향

- 기업투자와 전략적 파트너십

- 연구개발자금

- 리스크 평가 및 경감책

- 진부화 리스크와 기술 이행 관리

- 공급망의 혼란과 부품 부족 위험

- 통화 변동 및 국제 거래 위험

- 펌웨어 무결성 및 보안 부팅 구현

- 사이버 보안 및 데이터 프라이버시 고려 사항

- 신뢰 루트 구현과 하드웨어 보안 모듈

- 엔드 투 엔드 암호화와 안전한 통신 채널

- 익명화 및 가명화 기술

- ISO 27001 및 공통 기준 인증 요건

- 소비자 행동과 최종 용도에 관한 지견

- 얼리어댑터의 특성과 기술에 대한 열의

- 업데이트 통지 취향과 연락 수단

- 사고 대응과 위기 커뮤니케이션의 유효성

- 구매에 대한 영향력과 의사결정 권한의 매핑

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 확대계획과 자금조달

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 코어 프로세싱 하드웨어

- 마이크로컨트롤러(MCU) 및 시스템 온칩(SoC)

- 도메인 및 중앙 연산 유닛

- 연결성 및 통신 하드웨어

- 접속 모듈

- 텔레매틱스 제어 유닛(TCU)

- 통신 게이트웨이 및 에지 노드

- 스토리지 및 전원 하드웨어

- 비휘발성 메모리 및 스토리지 컴포넌트

- 전원 관리 및 인터페이스 하드웨어

- 보안 및 데이터 보호 하드웨어

- 진단 및 개발용 하드웨어

- 기타

- 코어 프로세싱 하드웨어

제6장 시장 추계 및 예측 : 접속 방식별, 2021-2034년

- 주요 동향

- 셀룰러

- Wi-Fi

- 위성통신

- LPWAN

- 기타

제7장 시장 추계 및 예측 : 갱신별, 2021-2034년

- 주요 동향

- 펌웨어 업데이트

- 애플리케이션 및 소프트웨어 업데이트

- 보안 패치 업데이트

- 설정 및 교정 갱신

- 기능의 잠금 해제 및 구독 기반 업데이트

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 소형 상용차

- 중형 상용차

- 대형 상용차

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Analog Devices

- Broadcom

- Infineon

- Intel

- Murata Manufacturing

- Nordic Semiconductor

- NXP Semiconductors

- Panasonic

- Qualcomm

- Rolling Wireless

- STMicroelectronics

- Texas Instruments

- 지역 기업

- Renesas Electronics

- ON Semiconductor

- Micron Technology

- Robert Bosch

- Toshiba Electronic Devices &Storage

- ROHM Semiconductor

- 신흥기업

- Microchip Technology

- Nexperia

- Wolfspeed

- Vishay Intertechnology

- Teltonika

- Queclink

The Global Automotive Over-the-Air (OTA) Update Hardware Market was valued at USD 7.6 Billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 26.8 Billion by 2034.

The automotive sector is rapidly transitioning toward software-defined vehicles (SDVs), creating strong demand for robust OTA hardware infrastructure. This market includes essential components such as core processing units, memory and storage modules, connectivity hardware, security chips, and monitoring and diagnostic systems. These elements enable OTA software updates, software feature activations, and cybersecurity patches for fleets of vehicles. The rise of connected vehicle ecosystems, increasing complexity of automotive software, and the necessity for uninterrupted customer experiences are accelerating the adoption of OTA hardware. COVID-19 emphasized the importance of OTA capabilities by highlighting the need for remote updates and minimizing reliance on physical service centers. As manufacturers aim to enhance vehicle lifecycle management and reduce maintenance downtime, OTA hardware is emerging as a critical investment for automakers globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 Billion |

| Forecast Value | $26.8 Billion |

| CAGR | 13.9% |

The market is rapidly integrating advanced connectivity solutions, including 5G cellular networks, Wi-Fi 6/6E, satellite communications, and Low Power Wide Area Network (LPWAN) technologies. These networks provide faster, more reliable OTA updates and support real-time vehicle-to-everything (V2X) communications. Vehicles equipped with multi-radio connectivity hardware can intelligently switch between networks based on signal strength, bandwidth requirements, and operational costs, ensuring consistent communication for updates and diagnostics.

The core processing hardware segment held a 35% share and is expected to grow at a CAGR of 13.2% from 2025 to 2034. This segment includes high-performance automotive processors, microcontrollers, system-on-chip (SoC) platforms, and specialized computing units designed for vehicle applications. Strong processing capability is essential to manage complex software updates, verify cybersecurity, and orchestrate various system functions efficiently. Meanwhile, cellular connectivity is projected to grow at a 15.1% CAGR and account for 49.4% of the market, driven by the need for reliable, high-bandwidth networks capable of supporting mission-critical OTA functions. Cellular technology offers carrier-grade reliability, global coverage, and secure implementation for critical updates.

Asia Pacific Automotive Over-the-Air (OTA) Update Hardware Market held a 41% share in 2024 and is expected to grow at a 15.1% CAGR. The region benefits from large-scale automotive production, rapid electric vehicle adoption, and government mandates promoting connected vehicle technologies. Regulatory requirements, such as upcoming standards in China, are compelling automakers to implement full OTA hardware capabilities in new vehicles, creating a significant opportunity for OTA hardware suppliers.

Key players in the Automotive Over-the-Air (OTA) Update Hardware Market include Intel, Broadcom, Qualcomm, Infineon, NXP Semiconductors, STMicroelectronics, Texas Instruments, Panasonic, Murata Manufacturing, and Nordic Semiconductor. Companies are focusing on innovation in processing and connectivity hardware to meet the demands of increasingly software-defined vehicles. Many are investing in multi-radio communication solutions, secure processors, and integrated system-on-chip designs to enhance OTA performance and cybersecurity. Strategic collaborations with automakers and Tier 1 suppliers are helping accelerate product adoption and global distribution. Regional expansion, especially in Asia Pacific, ensures access to high-volume automotive markets and regulatory-driven opportunities. Firms are also investing in research and development for next-generation 5G and satellite communication technologies to maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Connectivity

- 2.2.4 Update

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 SoC providers

- 3.1.1.2 Microcontroller (MCU) manufacturers

- 3.1.1.3 Connectivity & networking module suppliers

- 3.1.1.4 Semiconductor foundries

- 3.1.1.5 OTA software platform providers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Automotive industry digital transformation

- 3.2.1.2 IoT Device proliferation & federal cybersecurity mandates

- 3.2.1.3 Edge AI integration & chiplet architecture adoption

- 3.2.1.4 5G network deployment & enhanced connectivity infrastructure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Semiconductor supply chain concentration & geopolitical risks

- 3.2.2.2 Regulatory complexity & multi-jurisdictional compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Smart cities infrastructure modernization

- 3.2.3.2 Rural connectivity solutions & satellite-based OTA delivery

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Chiplet-based OTA systems & heterogeneous integration

- 3.3.1.2 3D packaging & advanced interconnect technologies

- 3.3.1.3 Neuromorphic computing integration for intelligent updates

- 3.3.1.4 Quantum-resistant security hardware implementation

- 3.3.2 Emerging technologies

- 3.3.2.1 6G network preparation & ultra-low latency updates

- 3.3.2.2 Satellite constellation integration for global coverage

- 3.3.2.3 Li-Fi & optical wireless communication for secure updates

- 3.3.2.4 Mesh networking & peer-to-peer update distribution

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Price trends

- 3.10.1 Hardware component pricing dynamics

- 3.10.2 Total cost of ownership models

- 3.10.3 Value-based pricing strategies

- 3.10.4 Cost optimization opportunities

- 3.11 Investment & Funding

- 3.11.1 Government investment programs

- 3.11.2 Private equity & venture capital trends

- 3.11.3 Corporate investment & strategic partnerships

- 3.11.4 Research & development funding

- 3.12 Risk assessment & mitigation

- 3.12.1 Obsolescence risk & technology transition management

- 3.12.2 Supply chain disruption & component shortage risks

- 3.12.3 Currency fluctuation & international transaction risks

- 3.12.4 Firmware integrity & secure boot implementation

- 3.13 Cybersecurity & data privacy considerations

- 3.13.1 Root of trust implementation & hardware security modules

- 3.13.2 End-to-end encryption & secure communication channels

- 3.13.3 Anonymization & pseudonymization techniques

- 3.13.4 ISO 27001 & common criteria certification requirements

- 3.14 Consumer behavior & End use insights

- 3.14.1 Early adopter characteristics & technology enthusiasm

- 3.14.2 Update notification preferences & communication channels

- 3.14.3 Incident response & crisis communication effectiveness

- 3.14.4 Purchasing influence & decision-making authority mapping

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.1.1 Core Processing Hardware

- 5.1.1.1 Microcontrollers (MCUs) and System-on-Chip (SoC)

- 5.1.1.2 Domain & Central Compute Units

- 5.1.2 Connectivity & Communication Hardware

- 5.1.2.1 Connectivity Modules

- 5.1.2.2 Telematics Control Units (TCU)

- 5.1.2.3 Communication Gateways & Edge Nodes

- 5.1.3 Storage & Power Hardware

- 5.1.3.1 Non-volatile Memory & Storage Components

- 5.1.3.2 Power Management & Interface Hardware

- 5.1.4 Security & Data Protection Hardware

- 5.1.5 Diagnostic & Development Hardware

- 5.1.6 Others

- 5.1.1 Core Processing Hardware

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Cellular

- 6.3 Wi-Fi

- 6.4 Satellite

- 6.5 LPWAN

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Update, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Firmware Updates

- 7.3 Application / Software Updates

- 7.4 Security Patch Updates

- 7.5 Configuration & Calibration Updates

- 7.6 Feature Unlocks / Subscription-Based Updates

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger Vehicle

- 8.2.1 Sedan

- 8.2.2 Hatchback

- 8.2.3 SUV

- 8.3 Commercial Vehicle

- 8.3.1 Light commercial vehicle

- 8.3.2 Medium commercial vehicle

- 8.3.3 Heavy commercial vehicle

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Analog Devices

- 10.1.2 Broadcom

- 10.1.3 Infineon

- 10.1.4 Intel

- 10.1.5 Murata Manufacturing

- 10.1.6 Nordic Semiconductor

- 10.1.7 NXP Semiconductors

- 10.1.8 Panasonic

- 10.1.9 Qualcomm

- 10.1.10 Rolling Wireless

- 10.1.11 STMicroelectronics

- 10.1.12 Texas Instruments

- 10.2 Regional players

- 10.2.1 Renesas Electronics

- 10.2.2 ON Semiconductor

- 10.2.3 Micron Technology

- 10.2.4 Robert Bosch

- 10.2.5 Toshiba Electronic Devices & Storage

- 10.2.6 ROHM Semiconductor

- 10.3 Emerging players

- 10.3.1 Microchip Technology

- 10.3.2 Nexperia

- 10.3.3 Wolfspeed

- 10.3.4 Vishay Intertechnology

- 10.3.5 Teltonika

- 10.3.6 Queclink