|

시장보고서

상품코드

1871188

유연 내시경 수술 로봇 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Flexible Endoscopic Surgery Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

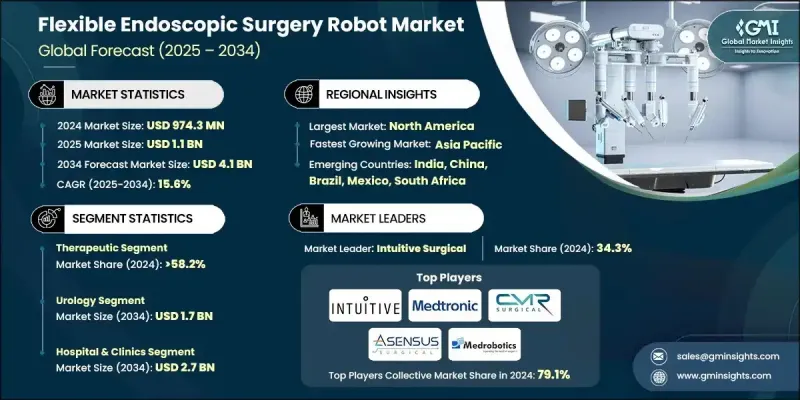

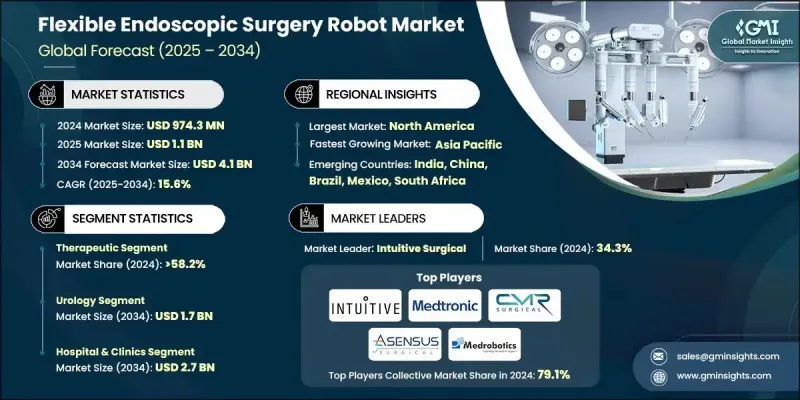

세계의 유연 내시경 수술 로봇 시장은 2024년 9억 7,430만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 15.6%로 성장해 41억 달러에 이를 것으로 예측되고 있습니다.

시장 성장은 저침습 수술 기구에 대한 수요 급증, 로봇 기술의 급속한 진보, 세계 수술 건수 증가에 의해 견인되고 있습니다. 유연 내시경 수술 로봇은 병원, 외래수술센터(ASC) 및 기타 의료 기관에 저침습 치료를 위한 고급 및 정밀 시스템을 제공함으로써 의료 상황을 변화시키고 있습니다. 이러한 로봇 솔루션은 AI, 영상 기술, 유연 로봇 메커니즘을 결합하여 진단 및 치료 기능을 모두 지원하며 수술의 정확성과 환자 회복을 향상시킵니다. AI 탑재 시스템, 고화질 시각화 기술, 향상된 유연 암 등 로보틱스의 진보로 외과의사는 복잡한 수술을 보다 정밀하고 리스크를 줄여 실시할 수 있게 되었습니다. 또한, 고령화와 만성 질환 증가에 따른 세계적인 수술 건수 증가가 제품 수요를 더욱 가속화하고 있습니다. 주요 제조업체에 의한 조사 및 혁신에 대한 지속적인 투자와 국제적인 사업 확대 노력이 함께, 의료시설에 있어서 이러한 시스템의 액세스 가능성이 높아져, 보다 광범위한 도입이 촉진되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 9억 7,430만 달러 |

| 예측 금액 | 41억 달러 |

| CAGR | 15.6% |

2024년 치료 분야는 58.2%의 점유율을 차지했습니다. 이것은 저침습 수술의 수용 확대와 로봇 제어 시스템의 정확성 향상에 기인합니다. 로봇 지원 치료 개입에 대한 선호의 고조가 이 분야를 재구성하고 있어 종양 절제나 조직 해부 등 복잡한 수술에 있어서, 시인성 향상, 뛰어난 조작성, 정밀한 네비게이션을 제공해, 외상을 최소한으로 억제하면서 환자의 회복을 가속화하고 있습니다.

비뇨기과 응용 분야는 2024년에 41.3%의 점유율을 차지했으며, 2034년까지 17억 달러에 이를 것으로 예측됩니다. 이 분야 시장 성장은 비뇨기 질환의 유병률 증가와 수술 정밀도 향상, 외상 경감, 입원 기간 단축을 실현하는 로봇 지원 수술의 보급 확대에 의해 추진되고 있습니다. 유연 로봇 암과 AI 가이드 네비게이션 시스템 등의 기술적 진보는 복잡한 비뇨기과 수술의 정확성을 대폭 향상시켜 시장의 급속한 확대에 기여하고 있습니다.

북미의 유연 내시경 수술 로봇 시장은 Medtronic, Intuitive Surgical, Johnson & Johnson 등 주요 기업의 존재에 힘입어 2024년 35.5%의 점유율을 차지했습니다. 이 지역의 이점은 저침습 수술 기반의 견고함, 유리한 상환 제도 및 로봇 지원 시스템에 대한 FDA의 적극적인 지원으로 더욱 강화되었습니다. 소화기 및 대장 질환의 높은 이환율 외에도 기술 교육과 외과 의사 교육에 대한 지속적인 주력이 결합되어 병원 및 수술센터에서 유연 로봇 플랫폼의 신속한 도입을 촉진하고 있습니다.

세계 유연 내시경 수술 로봇 시장에서 주요 기업으로는 Intuitive Surgical, Medtronic, Johnson & Johnson, CMR Surgical, Asensus Surgical, Medrobotics, Endo Tools Therapeutics, Endotics, GI View 등이 있습니다. 유연 내시경 수술 로봇 시장의 주요 기업은 자사의 지위를 강화하기 위해 혁신 추진과 세계 전개 확대를 목적으로 한 전략적 노력을 조합하여 채용하고 있습니다. 각 회사는 AI 기반의 정밀 툴과 고급 영상 처리 기능을 갖춘 차세대 로봇 플랫폼의 도입을 위해 연구 개발에 많은 투자를 실시했습니다. 기술 통합의 강화와 임상 응용 범위의 확대를 목적으로 한 협업 파트너십과 전략적 제휴도 형성되고 있습니다. 또한 규제 당국의 승인 취득과 종합적인 교육 프로그램의 개발에도 주력하여 외과의사에 의한 도입률의 향상을 도모하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 저침습 수술에 대한 수요 증가

- 로봇 기술의 진보

- 만성 질환 증가 경향

- 인공지능(AI)의 통합

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자비용

- 한정적인 상환 정책

- 시장 기회

- 일회용 로봇 시스템 개발

- AI 및 머신러닝 진보

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 가격 분석 2024

- 기술 상황

- 현재의 기술 동향

- 고급 화상 진단과 3D 시각화 시스템의 통합에 의한 외과적 정밀도의 향상

- 좁은 해부학적 영역에서의 조작성을 향상시키기 위한 로봇 암 소형화와 유연성 향상

- 실시간 촉각 피드백과 직관적인 제어 인터페이스에 의한 외과의 콘솔의 인체 공학적 설계 강화

- 신흥기술

- 정밀 유도 외과적 개입을 위한 AI 지원 네비게이션과 자율 운동 제어

- 클라우드 접속형 로봇 시스템에 의한 원격 수술 지원 및 데이터 분석 실현

- 증강현실(AR)과 가상현실(VR)의 통합에 의한 수술계획, 트레이닝, 수술중 가시화

- 현재의 기술 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

- AI, 화상 진단, 로봇 내비게이션의 통합

- 소형화와 시스템 유연 향상

- 디지털 수술 생태계와의 통합

- 촉각 피드백과 자율 지원 기술의 진보

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신 서비스 유형 제공 개시

- 확대 계획

제5장 시장 추계 및 예측 : 카테고리별, 2021-2034년

- 주요 동향

- 치료 분야

- 진단

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 비뇨기과

- 호흡기

- 소화기

- 기타 용도

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원 및 진료소

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Asensus Surgical

- CMR Surgical

- Endo Tools Therapeutics

- Endotics

- GI View

- Intuitive Surgical

- Johnson & Johnson

- Medrobotics

- Medtronic

The Global Flexible Endoscopic Surgery Robot Market was valued at USD 974.3 million in 2024 and is estimated to grow at a CAGR of 15.6% to reach USD 4.1 Billion by 2034.

Market growth is driven by the surging need for minimally invasive surgical tools, rapid advancements in robotic technology, and the growing number of surgical procedures worldwide. Flexible endoscopic surgery robots are transforming the healthcare landscape by offering hospitals, ambulatory centers, and other medical institutions advanced, precision-driven systems for minimally invasive treatments. These robotic solutions combine AI, imaging, and flexible robotic mechanisms to support both diagnostic and therapeutic functions, enhancing surgical precision and patient recovery. Progress in robotics, such as AI-enabled systems, high-definition visualization, and improved flexible arms, allows surgeons to perform complex interventions with higher accuracy and reduced risks. Additionally, the rise in global surgical procedures, spurred by an aging population and an increasing burden of chronic diseases, is further accelerating product demand. Continued investments in research and innovation, coupled with international expansion efforts by key manufacturers, are increasing accessibility and encouraging broader adoption of these systems in healthcare facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $974.3 Million |

| Forecast Value | $4.1 Billion |

| CAGR | 15.6% |

In 2024, the therapeutic segment held a 58.2% share attributed to the rising acceptance of minimally invasive surgeries and enhanced precision in robotic control systems. The growing preference for robotic-assisted therapeutic interventions is reshaping the segment, offering improved visualization, superior dexterity, and refined navigation for intricate operations such as tumor excisions and tissue dissections with minimal trauma and faster patient recovery.

The urology application segment held a 41.3% share in 2024 and is projected to reach USD 1.7 Billion by 2034. Market growth in this domain is propelled by the increasing prevalence of urological disorders and the widespread integration of robotic-assisted surgeries that enhance surgical accuracy, reduce trauma, and shorten hospital stays. Technological advancements, including flexible robotic arms and AI-guided navigation systems, are significantly boosting precision in complex urological procedures and contributing to the market's rapid expansion.

North America Flexible Endoscopic Surgery Robot Market held 35.5% share in 2024, supported by the presence of leading industry participants such as Medtronic, Intuitive Surgical, and Johnson & Johnson. The region's dominance is further supported by a strong base of minimally invasive surgical procedures, favorable reimbursement frameworks, and active FDA support for robotic-assisted systems. The high prevalence of gastrointestinal and colorectal diseases, alongside the continuous focus on technological education and surgeon training, is fostering the swift adoption of flexible robotic platforms across hospitals and surgical centers.

Prominent companies active in the Global Flexible Endoscopic Surgery Robot Market include Intuitive Surgical, Medtronic, Johnson & Johnson, CMR Surgical, Asensus Surgical, Medrobotics, Endo Tools Therapeutics, Endotics, and GI View. To strengthen their position, key players in the Flexible Endoscopic Surgery Robot Market are adopting a mix of strategic initiatives aimed at driving innovation and expanding global reach. Companies are heavily investing in R&D to introduce next-generation robotic platforms equipped with AI-based precision tools and advanced imaging capabilities. Collaborative partnerships and strategic alliances are being formed to enhance technology integration and expand clinical applications. Firms are also focusing on obtaining regulatory approvals and developing comprehensive training programs to increase adoption rates among surgeons.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Category trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing preference for minimally invasive procedures

- 3.2.1.2 Advancements in robotic technology

- 3.2.1.3 Rising prevalence of chronic diseases

- 3.2.1.4 Integration of artificial intelligence (AI)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Limited reimbursement policies

- 3.2.3 Market opportunities

- 3.2.3.1 Development of single-use robotic systems

- 3.2.3.2 Advancements in AI and machine learning

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Pricing analysis, 2024

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.1.1 Integration of advanced imaging and 3D visualization systems for enhanced surgical precision

- 3.6.1.2 Miniaturization and increased flexibility of robotic arms for improved maneuverability in confined anatomical regions

- 3.6.1.3 Enhanced surgeon-console ergonomics with real-time haptic feedback and intuitive control interfaces

- 3.6.2 Emerging technologies

- 3.6.2.1 AI-assisted navigation and autonomous motion control for precision-guided surgical interventions

- 3.6.2.2 Cloud-connected robotic systems enabling remote surgery assistance and data analytics

- 3.6.2.3 Integration of augmented reality (AR) and virtual reality (VR) for surgical planning, training, and intraoperative visualization

- 3.6.1 Current technological trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.10.1 Integration of AI, imaging, and robotic navigation

- 3.10.2 Miniaturization and enhanced system flexibility

- 3.10.3 Integration with digital surgical ecosystems

- 3.10.4 Advancements in haptic feedback and autonomous assistance

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Category, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutic

- 5.3 Diagnostic

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Urology

- 6.3 Respiratory applications

- 6.4 Gastrointestinal applications

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital & clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Asensus Surgical

- 9.2 CMR Surgical

- 9.3 Endo Tools Therapeutics

- 9.4 Endotics

- 9.5 GI View

- 9.6 Intuitive Surgical

- 9.7 Johnson & Johnson

- 9.8 Medrobotics

- 9.9 Medtronic