|

시장보고서

상품코드

1871205

항공우주 단열재용 에어로겔 복합재료 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Aerogel Composites for Aerospace Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

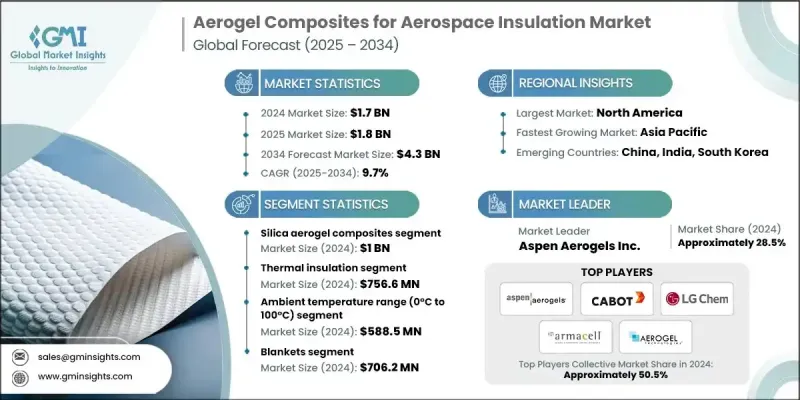

세계의 항공우주 단열재용 에어로겔 복합재료 시장은 2024년에 17억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 9.7%를 나타내 성장해 43억 달러에 이를 것으로 예상되고 있습니다.

시장 성장은 민간 항공기 및 방위 항공기 양방향으로 경량 고성능 열 방호 시스템에 항공우주 산업의 관심이 높아지고 있기 때문입니다. 에어로겔 복합재는 무게를 최소화하면서 탁월한 단열성을 제공하여 구조적 무결성을 손상시키지 않고 항공기의 연료 효율 목표 달성을 지원합니다. 뛰어난 열전도성과 극저온 환경에서 1,200℃를 넘는 고온까지 견딜 수 있는 능력을 겸비하고 있기 때문에 차세대 항공기 및 우주선 용도에 이상적인 재료가 되고 있습니다. 실리카 및 폴리머계 에어로겔 복합재료의 진보로 기계적 내구성과 가공효율이 향상되어 항공우주 분야의 열관리에 폭넓은 도입이 가능해졌습니다. 섬유 강화 에어로겔과 폴리이미드 에어로겔의 혁신으로 기존의 에어로겔에 비해 기계적 강도가 수백 배 향상하면서도 단열 성능을 유지하고 있습니다. 지속 가능한 항공, 전기 항공기, 배터리 열 관리에 대한 관심이 높아짐에 따라 채용을 더욱 촉진하고 있으며, 제조업체는 경량성과 고성능 단열성을 겸비한 재료를 요구하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 17억 달러 |

| 예측 금액 | 43억 달러 |

| CAGR | 9.7% |

실리카 에어로겔 복합재료 부문은 2024년에 10억 달러 시장 규모를 창출했고, 2025년부터 2034년에 걸쳐 CAGR 9.9%를 나타내 시장 전체의 60.2%를 차지할 것으로 예측됩니다. 실리카계 복합재료는 초저열 전도율, 구조적 안정성, 뛰어난 내화성으로 부문을 선도하고 있으며, 항공기 엔진 구획, 우주선의 열 시스템, 극저온 연료 저장에 적합합니다. 극단적인 온도 조건 하에서 입증 된 성능과 엄격한 항공우주 방화 기준에 대한 적합성은 상업, 군사 및 우주 분야에서 중요한 단열 용도의 재료로 선택되었습니다.

단열재 부문은 2024년에 7억 5,660만 달러 시장 규모를 기록했으며, 2034년까지 연평균 복합 성장률(CAGR) 10%를 나타내 45% 시장 점유율을 획득할 것으로 예측됩니다. 이 부문이 우위를 유지하는 배경에는 항공기 엔진, 우주선 시스템 및 극저온 연료 저장에서 온도 제어의 중요성이 있습니다. 에어로겔 복합재는 -200℃에서 500℃를 초과하는 극한 환경에서도 우수한 단열 성능을 유지합니다. 특히 우주용도에서 수요가 높고, 우주공간의 가혹한 온도변동에 견디면서 기기나 탑승실을 보호하는 열방호시스템이 요구되고 있습니다.

북미의 항공우주 단열재용 에어로겔 복합재료 시장은 2024년 42%의 점유율을 차지했습니다. 이 지역의 주도적 지위는 주요 항공우주 제조업체의 존재, 선진적인 연구기관, 방위 및 항공우주프로그램에 대한 정부에 의한 다액의 투자에 기인하고 있습니다. 미국은 강력한 항공우주 생태계를 가지고 있으며, 기업은 항공기와 우주선 설계에 에어로겔 복합재를 적극적으로 통합하고 있습니다. 정부 자금에 의한 우주 탐사 이니셔티브와 방어 프로그램도 북미에서 에어로겔 기반 단열 솔루션의 기술 개발과 응용을 가속화하고 있습니다.

세계의 항공우주 단열재용 에어로겔 복합재료 시장에서 주요 기업은 FLEXcon, LG Chem, Armacel International, Blueshift Materials, Aspen Aerogels, Inc., Active Aerogels, Aerogel Technologies LLC, EAS Fiberglass Co., Ltd., Jucos Refractory, WH Thermal Energy Tec. Aerogel Holding AB, Guangdong Alison Technology, Wedge India 등을 들 수 있습니다. 항공우주 단열재용 에어로겔 복합재료 시장의 기업은 존재감과 시장 포지션을 강화하기 위해 몇 가지 전략적 접근법을 채택하고 있습니다. 에어로겔 복합재의 재료강도, 열효율, 제조성을 향상시키기 위해 연구개발에 많은 투자를 하고 있습니다. 항공우주 OEM 및 방위 계약업체와의 전략적 제휴는 장기 계약의 확보와 상업, 군사, 우주 용도의 채용 확대에 기여하고 있습니다. 또한 각 회사는 진화하는 성능 요건에 대응하기 위해 폴리머 강화 복합재나 섬유 강화 복합재에 의한 제품 포트폴리오의 다양화에도 주력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 공급망의 복잡성

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 실리카 에어로겔 복합재료

- 탄소 에어로겔 복합재료

- 하이브리드 에어로겔 복합재료

- 폴리머 에어로겔 복합재료

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 단열

- 방음

- 방화

- 진동 감쇠

제7장 시장 추계·예측 : 온도 범위별(2021-2034년)

- 주요 동향

- 극저온(-200℃--100℃)

- 저온(-100℃-0℃)

- 상온(0°C-100°C)

- 고온(100℃-500℃)

- 극고온(500°C 초과)

제8장 시장 추계·예측 : 형태별(2021-2034년)

- 주요 동향

- 담요

- 패널

- 코팅

- 맞춤형 형상

제9장 시장 추계·예측 : 제조 공정별(2021-2034년)

- 주요 동향

- 초임계 건조

- 상압 건조

- 동결 건조

- 졸-겔 공정

제10장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 상업용 항공기

- 군용 항공기

- 우주선

- 전기 항공기

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제12장 기업 프로파일

- Aspen Aerogels, Inc.

- Cabot Corporation

- LG Chem

- Armacell International

- Aerogel Technologies LLC

- Blueshift Materials

- Svenska Aerogel Holding AB

- Active Aerogels

- Green Earth Aerogel Technologies

- FLEXcon

- EAS Fiberglass Co., Ltd.

- Guangdong Alison Technology

- Jucos Refractory

- WH Thermal Energy Technology

- Wedge India

The Global Aerogel Composites for Aerospace Insulation Market was valued at USD 1.7 Billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 4.3 Billion by 2034.

Market growth is driven by the aerospace industry's growing focus on lightweight, high-performance thermal protection systems for both commercial and defense aircraft. Aerogel composites offer exceptional thermal insulation while minimizing weight, helping aircraft meet fuel efficiency targets without compromising structural integrity. Their superior thermal conductivity, combined with the ability to endure extreme temperatures ranging from cryogenic conditions to above 1,200°C, makes them ideal for next-generation aircraft and spacecraft applications. Advances in silica and polymer-based aerogel composites have enhanced mechanical durability and processing efficiency, enabling broader implementation in aerospace thermal management. Innovations in fiber-reinforced and polyimide aerogels are improving mechanical strength by hundreds of times over conventional aerogels while retaining thermal performance. Increasing emphasis on sustainable aviation, electric aircraft, and battery thermal management is further propelling adoption, as manufacturers seek materials that combine lightweight properties with high-performance insulation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 billion |

| Forecast Value | $4.3 billion |

| CAGR | 9.7% |

The silica aerogel composites segment generated USD 1 Billion in 2024 and is projected to grow at a CAGR of 9.9% from 2025 to 2034, accounting for 60.2% of the market. Silica-based composites lead the segment due to their ultra-low thermal conductivity, structural stability, and excellent fire resistance, making them suitable for aircraft engine compartments, spacecraft thermal systems, and cryogenic fuel storage. Their proven performance in extreme temperature conditions and compliance with stringent aerospace fire standards have positioned them as the material of choice for critical thermal insulation applications across commercial, military, and space sectors.

The thermal insulation segment was valued at USD 756.6 million in 2024 and is expected to grow at a CAGR of 10% through 2034, capturing a 45% market share. This segment dominates due to the essential role of temperature control in aircraft engines, spacecraft systems, and cryogenic fuel containment. Aerogel composites excel in maintaining thermal performance across extreme environments, from -200°C to over 500°C. The demand is particularly high for space applications, where thermal protection systems must withstand the harsh temperature fluctuations of outer space while safeguarding equipment and crew compartments.

North America Aerogel Composites for Aerospace Insulation Market accounted for a 42% share in 2024. The region's leadership stems from the presence of major aerospace manufacturers, advanced research institutions, and substantial government investment in defense and aerospace programs. The U.S. benefits from a strong aerospace ecosystem, with companies actively integrating aerogel composites into aircraft and spacecraft designs. Government-funded space exploration initiatives and defense programs are also accelerating technological development and the application of aerogel-based thermal solutions in North America.

Leading players in the Global Aerogel Composites for Aerospace Insulation Market include FLEXcon, LG Chem, Armacell International, Blueshift Materials, Aspen Aerogels, Inc., Active Aerogels, Aerogel Technologies LLC, EAS Fiberglass Co., Ltd., Jucos Refractory, WH Thermal Energy Technology, Green Earth Aerogel Technologies, Svenska Aerogel Holding AB, Guangdong Alison Technology, and Wedge India. Companies in the Aerogel Composites for Aerospace Insulation Market are employing several strategic approaches to strengthen their presence and market position. They are investing heavily in R&D to enhance the material strength, thermal efficiency, and manufacturability of aerogel composites. Strategic partnerships with aerospace OEMs and defense contractors help secure long-term contracts and expand adoption in commercial, military, and space applications. Firms are also focusing on diversifying their product portfolio with polymer- and fiber-reinforced composites to meet evolving performance requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Application

- 2.2.3 Temperature range

- 2.2.4 Form

- 2.2.5 Manufacturing process

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Silica aerogel composites

- 5.3 Carbon aerogel composites

- 5.4 Hybrid aerogel composites

- 5.5 Polymer aerogel composites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Thermal insulation

- 6.3 Acoustic insulation

- 6.4 Fire protection

- 6.5 Vibration damping

Chapter 7 Market Estimates and Forecast, By Temperature Range, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Cryogenic (-200°C to -100°C)

- 7.3 Low temperature (-100°C to 0°C)

- 7.4 Ambient (0°C to 100°C)

- 7.5 High temperature (100°C to 500°C)

- 7.6 Extreme temperature (>500°C)

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Blankets

- 8.3 Panels

- 8.4 Coatings

- 8.5 Custom shapes

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Supercritical drying

- 9.3 Ambient pressure drying

- 9.4 Freeze drying

- 9.5 Sol-gel processing

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 Commercial aircraft

- 10.3 Military aircraft

- 10.4 Spacecraft

- 10.5 Electric aircraft

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East & Africa

Chapter 12 Company Profiles

- 12.1 Aspen Aerogels, Inc.

- 12.2 Cabot Corporation

- 12.3 LG Chem

- 12.4 Armacell International

- 12.5 Aerogel Technologies LLC

- 12.6 Blueshift Materials

- 12.7 Svenska Aerogel Holding AB

- 12.8 Active Aerogels

- 12.9 Green Earth Aerogel Technologies

- 12.10 FLEXcon

- 12.11 EAS Fiberglass Co., Ltd.

- 12.12 Guangdong Alison Technology

- 12.13 Jucos Refractory

- 12.14 WH Thermal Energy Technology

- 12.15 Wedge India