|

시장보고서

상품코드

1871211

정밀진단 및 의료 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Precision Diagnostics and Medicine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

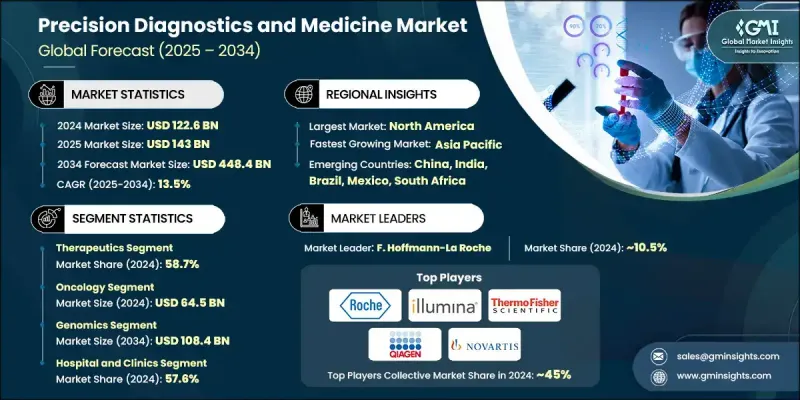

세계의 정밀진단 및 의료 시장은 2024년 1,226억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 13.5%로 성장하여 4,484억 달러에 달할 것으로 예측되고 있습니다.

정밀의료는 표준화된 치료에서 개인의 유전자 프로파일, 생활 습관, 환경 기반의 고도로 개별화된 접근 방식으로 전환함으로써 건강 관리를 변화시키고 있습니다. 이 접근법은 일반적인 프로토콜이 아닌 개별화된 전략에 초점을 맞추어 다양한 질병에서 치료 성과를 향상시키는 것을 추진하고 있습니다. 데이터 구동 진단 기술의 급속한 진보와 목표 치료에 대한 수요가 증가함에 따라 시장 발전를 계속 형성하고 있습니다. 멀티오믹스 플랫폼의 통합은 혁신을 가속화하고 임상의와 조사자에게 복잡한 생물학적 시스템에 대한 자세한 지식을 제공합니다. 정밀의료에 대한 접근이 확대되고 혁신적인 치료법의 신속한 승인을 지원하는 규제 프레임워크가 진화함에 따라 세계적인 보급이 진행될 전망입니다. 의료 제공업체와 바이오의약품 기업은 임상 통합을 지원하기 위해 협력을 강화하고 있으며, 디지털 기술과 동반자 진단은 개인화 치료 계획을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 1,226억 달러 |

| 예측 금액 | 4,484억 달러 |

| CAGR | 13.5% |

2024년, 치료제 부문은 58.7%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 13.3%를 보일 것으로 예측됩니다. 개별 환자 프로파일에 맞는 치료법의 설계에 중점을 두는 것이 이러한 성장을 뒷받침하고 있습니다. 세포 치료, 유전자 기반 솔루션, 면역 표적 약물의 진보는 특히 복잡한 질병이나 희귀질환의 치료 프로토콜을 재구성하고 있습니다. 높은 개발 비용과 높은 가격의 의약품이이 부문 전체의 가치를 계속 밀고 있습니다.

유전체학 분야는 2034년까지 1,084억 달러 규모에 달할 것으로 예측됩니다. 유전체 기술은 특정 유전자 변이가 질병의 진행과 치료 반응에 어떻게 영향을 미치는지를 이해하는데 중요한 역할을 합니다. 차세대 시퀀싱과 전체 유전체 분석과 같은 기술을 통해 치료에 효과적인 돌연변이를 정확하게 식별할 수 있게 되었습니다. 이에 따라 유전체학는 의약품 개발과 개인화 치료 전략 모두에서 그 역할을 크게 향상시켜 임상 진단 및 연구 응용에서의 중요성을 더욱 강화하고 있습니다.

북미의 정밀진단 및 의료 시장은 2024년 43.5%의 점유율을 차지했습니다. 이 지역은 견고한 헬스케어 인프라, 높은 R&D 투자, 일류 제약 및 바이오테크놀러지 기업의 존재에 지지되어 계속 주도적 입장을 유지하고 있습니다. 유리한 규제 프레임워크와 정부의 엄청난 지출은 맞춤형 의료의 혁신을 더욱 뒷받침하고 있습니다. 또한 동반진단의 광범위한 보급과 고급 유전체 검사 기술의 존재가이 지역의 견고한 시장 위치에 기여합니다.

정밀진단 및 의료 시장을 견인하는 주요 기업으로는 Illumina, Novartis, Cepheid (Danaher Corporation), Qiagen, Takeda Pharmaceutical Company Limited, Pfizer, F. Hoffmann-La Roche, Laboratory Corporation of America Holdings (Labcorp), Thermo Fisher Scientific, Bristol-Myers Squibb Company, GlaxoSmithKline, Agilent Technologies, Myriad Genetics, AstraZeneca, Quest Diagnostics, bioMerieux, Natera, Eli Lilly & Company, Abbott, AbbVie 등이 있습니다. 정밀진단 및 의약품 시장의 주요 기업은 사업 기반의 확대를 도모하기 위해 전략적 제휴, 파트너십, 인수에 주력하여 제품 파이프라인의 강화와 기술력의 다양화를 도모하고 있습니다. 각 회사는 진단의 정확성과 치료의 개별화를 개선하기 위해 멀티오믹스 플랫폼, AI를 활용한 데이터 분석 및 첨단 유전체 솔루션에 많은 투자를 하고 있습니다. 또한 데이터 기반 모델을 통한 임상시험의 정확성 향상과 규제 당국의 승인 가속화도 핵심 전략이 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유전체학 및 생명공학의 진보

- 만성 질환 및 유전성 질환 증가 경향

- 정부에 의한 대처와 자금 제공 증가

- 동반진단의 채용 확대

- 업계의 잠재적 위험 및 과제

- 맞춤형 치료 및 진단의 고비용

- 한정적인 상환 정책

- 복잡한 규제 경로

- 시장 기회

- 비종양학 분야로의 급속한 확대

- 신흥 시장에서의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 기술 상황

- 현재의 동향

- 신흥기술

- 파이프라인 분석

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 진단제

- 유전자 검사

- 바이오마커 기반 검사

- 특수검사

- 기타 진단 검사

- 치료제

- 억제제

- 단일클론항체

- 세포 및 유전자 치료

- 항바이러스제 및 항레트로바이러스제

- 기타 치료제

제6장 시장 추계 및 예측 : 적응증별, 2021-2034년

- 주요 동향

- 종양학

- 신경학

- 감염증

- 면역학

- 희귀질환 및 유전성 질환

- 순환기학

- 기타 적응증

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 유전체학

- 바이오인포매틱스

- 빅데이터 분석

- 바이오마커 검출

- 고처리량 스크리닝

- 기타 기술

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원 및 진료소

- 진단실험실

- 기타 최종 용도

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Agilent Technologies

- Abbott

- AbbVie

- AstraZeneca

- bioMerieux

- Bristol-Myers Squibb Company

- Cepheid(Danaher Corporation)

- Eli Lilly &Company

- F. Hoffmann-La Roche

- GlaxoSmithKline

- Illumina

- Laboratory Corporation of America Holdings(Labcorp)

- Myriad Genetics

- Novartis

- Natera

- Pfizer

- Qiagen

- Quest Diagnostics

- Takeda Pharmaceutical Company Limited

- Thermo Fisher Scientific

The Global Precision Diagnostics and Medicine Market was valued at USD 122.6 Billion in 2024 and is estimated to grow at a CAGR of 13.5% to reach USD 448.4 Billion by 2034.

Precision medicine is transforming healthcare by shifting from standardized treatments to highly tailored approaches based on an individual's genetic profile, lifestyle, and environment. This approach focuses on personalized strategies rather than generalized protocols, driving improved outcomes across various diseases. Rapid advancements in data-driven diagnostics, coupled with growing demand for targeted treatments, continue to shape the evolution of the market. Integration of multi-omics platforms is accelerating innovation, providing clinicians and researchers with detailed insights into complex biological systems. As precision therapies become more accessible and regulatory frameworks evolve to support quicker approval of innovative treatments, global adoption is poised to increase. Healthcare providers and biopharma companies are aligning efforts to support clinical integration, while digital technologies and companion diagnostics strengthen personalized treatment plans.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $122.6 Billion |

| Forecast Value | $448.4 Billion |

| CAGR | 13.5% |

In 2024, the therapeutics segment held 58.7% share and is forecasted to grow at a CAGR of 13.3% through 2034. The focus on designing therapies tailored to individual patient profiles is fueling this growth. Advances in cellular therapies, gene-based solutions, and immune-targeted drugs are reshaping treatment protocols, especially for complex or rare diseases. High development costs and premium drug pricing continue to drive value across this segment.

The genomics segment is anticipated to hit USD 108.4 Billion by 2034. Genomic technologies play a critical role in understanding how specific genetic variations affect disease progression and treatment response. Techniques such as next-generation sequencing and full genome analysis allow for precise identification of actionable mutations. This has significantly elevated the role of genomics in both drug development and personalized therapeutic strategies, reinforcing its significance in clinical diagnostics and research applications.

North America Precision Diagnostics and Medicine Market held 43.5% share in 2024. The region continues to lead the way, supported by robust healthcare infrastructure, high R&D investment, and the presence of top-tier pharmaceutical and biotech companies. Favorable regulatory frameworks and substantial government spending further support innovation in personalized healthcare. Additionally, the widespread availability of companion diagnostics and the presence of sophisticated genomic testing technologies contribute to the region's strong market position.

Leading companies shaping the Precision Diagnostics and Medicine Market include Illumina, Novartis, Cepheid (Danaher Corporation), Qiagen, Takeda Pharmaceutical Company Limited, Pfizer, F. Hoffmann-La Roche, Laboratory Corporation of America Holdings (Labcorp), Thermo Fisher Scientific, Bristol-Myers Squibb Company, GlaxoSmithKline, Agilent Technologies, Myriad Genetics, AstraZeneca, Quest Diagnostics, bioMerieux, Natera, Eli Lilly & Company, Abbott, and AbbVie. To expand their footprint, key players in the Precision Diagnostics and Medicine Market are focusing on strategic collaborations, partnerships, and acquisitions to enhance their product pipelines and diversify technological capabilities. Companies are investing heavily in multi-omics platforms, AI-powered data analytics, and advanced genomic solutions to improve the accuracy of diagnostics and personalization of treatments. Enhancing clinical trial precision and speeding regulatory approvals through data-driven models are also core strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Indication trends

- 2.2.4 Technology trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in genomics and biotechnology

- 3.2.1.2 Rising prevalence of chronic and genetic diseases

- 3.2.1.3 Increasing government initiatives and funding

- 3.2.1.4 Increased adoption of companion diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of personalized therapies and diagnostics

- 3.2.2.2 Limited reimbursement policies

- 3.2.2.3 Complex regulatory pathways

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid expansion into non-oncology fields

- 3.2.3.2 Growth in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostics

- 5.2.1 Genetic tests

- 5.2.2 Biomarker-based tests

- 5.2.3 Esoteric tests

- 5.2.4 Other diagnostic tests

- 5.3 Therapeutics

- 5.3.1 Inhibitor drugs

- 5.3.2 Monoclonal antibodies

- 5.3.3 Cell and gene therapy

- 5.3.4 Antiviral and anti-retroviral drugs

- 5.3.5 Other therapeutics

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Neurology

- 6.4 Infectious diseases

- 6.5 Immunology

- 6.6 Rare and genetic disorders

- 6.7 Cardiology

- 6.8 Other indications

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Genomics

- 7.3 Bioinformatics

- 7.4 Big data analytics

- 7.5 Biomarker detection

- 7.6 High-throughput screening

- 7.7 Other technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Diagnostic laboratories

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent Technologies

- 10.2 Abbott

- 10.3 AbbVie

- 10.4 AstraZeneca

- 10.5 bioMerieux

- 10.6 Bristol-Myers Squibb Company

- 10.7 Cepheid (Danaher Corporation)

- 10.8 Eli Lilly & Company

- 10.9 F. Hoffmann-La Roche

- 10.10 GlaxoSmithKline

- 10.11 Illumina

- 10.12 Laboratory Corporation of America Holdings (Labcorp)

- 10.13 Myriad Genetics

- 10.14 Novartis

- 10.15 Natera

- 10.16 Pfizer

- 10.17 Qiagen

- 10.18 Quest Diagnostics

- 10.19 Takeda Pharmaceutical Company Limited

- 10.20 Thermo Fisher Scientific