|

시장보고서

상품코드

1871238

자가 치유 방수재료 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Self-healing Waterproofing Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

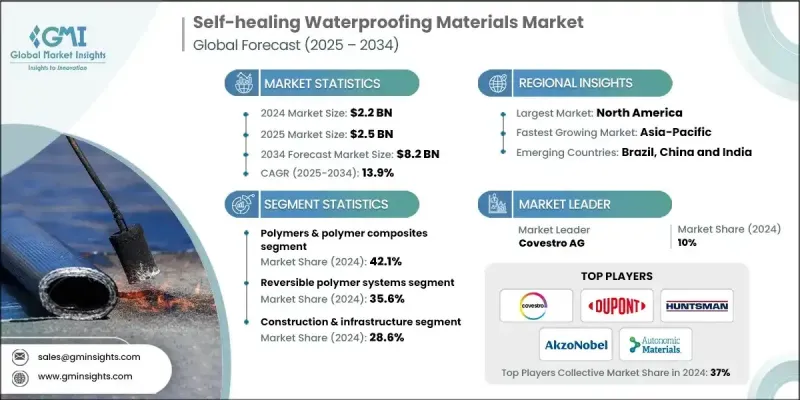

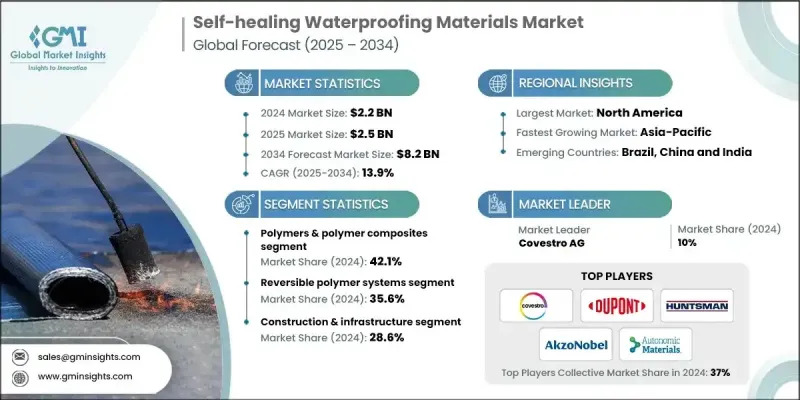

세계의 자가 치유 방수재료 시장은 2024년 22억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 13.9%로 성장해 82억 달러에 달할 것으로 예측되고 있습니다.

산업 분야에서 장기적인 내구성과 유지 보수 비용 절감에 대한 관심이 높아지는 가운데, 본 시장은 강력한 성장을 보이고 있습니다. 이러한 첨단 재료는 습기나 가혹한 환경조건에의 노출이 성능이나 수명에 영향을 미치기 쉬운 건설, 자동차, 전자기기 분야에서의 응용이 진행되고 있습니다. 건설 분야에서는 구조물의 내성을 향상시키고 라이프사이클 비용을 최소화하기 위해 자가 치유 코팅과 콘크리트를 채용하고 있습니다. 자동차 산업에서는 내구성 향상을 위해 내식성과 손상 복구 기능을 갖춘 표면 처리가 도입되고 있습니다. 마이크로캡슐화 기술, 혈관 시스템, 형상 기억 폴리머의 기술적 진보가 보다 효율적인 자가 치유 메커니즘의 진화를 추진하고 있습니다. 또한 실시간 손상 감지 및 자율적 복구 작동을 실현하는 센서 기반 시스템의 통합이 차세대 방수 솔루션의 형성에 기여하고 있습니다. 이러한 진전에도 불구하고, 특히 개발도상국에 있어서, 비용 대 효과나 확장성과 관련된 과제가 시장에 존재하고 있습니다. 그러나 지속 가능한 소재에 대한 규제면의 지원 강화와 표준화를 위한 세계적인 노력이 상업화를 촉진할 것으로 전망됩니다. 아시아태평양의 급속한 인프라 개발도 도시화와 장수명 건설자재에 대한 수요 증가를 배경으로 시장 확대에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 22억 달러 |

| 예측 금액 | 82억 달러 |

| CAGR | 13.9% |

폴리머 및 폴리머 복합재 부문은 2024년에 42.1%의 점유율을 차지했며 2034년까지 연평균 복합 성장률(CAGR) 13.6%를 보일 것으로 예측됩니다. 이점은 높은 적응성, 성숙한 제조 능력 및 여러 산업에 걸친 다양한 용도에 대한 적합성에 기인합니다. 이러한 재료는 다양한 자가 치유 메커니즘을 채택할 수 있으므로 건설, 자동차 및 전자 장비 용도에 이상적입니다. 지속가능하고 바이오 폴리머 기술의 지속적인 진보와 조사 투자 증가가 함께 세계 환경 의식이 높은 시장에 대한 수요를 강화하고 있습니다.

가역성 고분자 시스템 부문은 2024년 35.6%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 13.7%를 보일 것으로 예측됩니다. 이러한 시스템은 기계적 성능을 크게 저하시키지 않으면서 여러 번의 수리 사이클을 거치는 특성에서 높은 평가를 받았습니다. 동적 공유 결합 및 비공유 결합을 기반으로 하는 이러한 시스템은 응력 및 손상에 노출될 때 자율적으로 구조를 복구합니다. 기존 제조 공정과의 호환성과 상업적 확장성은 건설, 전자기기, 운송 등의 분야에서 대규모 응용에 적합합니다. 복구 메커니즘의 신뢰성과 재현성은 산업 분야에서 광범위한 채용에 기여하고 있습니다.

북미의 자가 치유 방수 재료 시장은 2024년 38.2%의 점유율을 차지했습니다. 이 지역은 강력한 정부 자금, 세계 수준의 연구시설, 고급 재료의 조기 상업화 등의 이점을 가지고 있습니다. 항공우주, 방위, 인프라 분야의 고성능 용도가 수요를 견인하고 있으며, 민간 및 공적기관 양방의 혁신에 대한 대대적인 투자가 이를 지원하고 있습니다. 재료과학에 특화된 기관에 의한 연구협력과 자금제공은 북미의 주도적 입장을 더욱 강화하고 있습니다. 주요 대학, 신흥 기업, 확립된 화학 기업의 존재는 지속적인 제품 개발과 기술 진보를 촉진하고 지역 전체에서 혁신적인 자체 복구 솔루션의 안정적인 공급을 보장합니다.

세계 자가 치유 방수 재료 시장에서 주요 기업으로는 Autonomic Materials Inc., DuPont de Nemours Inc., PPG Industries Inc., Avecom N.V., Covestro AG, Critical Materials S.A., Tnemec Company Inc., Devan Chemicals NV, Akzo Nobel N.V., Huntsman Corporation, Applied Thin Films Inc., Acciona S.A., Sensor Coating Systems Ltd 등이 있습니다. 주요 기업은 자사의 지위를 강화하기 위해 기술 혁신, 제품 다양화, 지속 가능한 개발에 주력하고 있습니다. 많은 기업들이 자가 치유 시스템의 효율성, 응답성 및 비용 효율성을 향상시키기 위해 R&D 투자를 확대하고 있습니다. 제품시험과 상업화를 가속화하기 위해 연구기관이나 산업관계자와의 전략적 제휴가 구축되고 있습니다. 제조업체 각사는 세계의 지속가능성 기준을 충족하기 위해 생산능력의 확대와 환경에 배려한 배합의 개발을 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 증가하는 인프라 유지 관리 비용과 수리 빈도 저감의 필요성

- 항공우주 산업에서 경량이면서 자가 치유 기능을 갖춘 복합재료 수요 발생

- 자동차 업계에 있어서의 내상성 및 자가 치유 코팅의 추진

- 업계의 잠재적 위험 및 과제

- 높은 초기 재료 비용 및 제조의 복잡성

- 표준화된 테스트 프로토콜 및 성능 검증 부족

- 시장 기회

- 재생에너지 시스템의 신흥 응용 분야

- 의료기기와의 통합 및 생체 적합성 자가 치유 재료

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 소재 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주: 무역 통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 대한 배려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 재료 유형별, 2021-2034년

- 주요 동향

- 폴리머 및 폴리머 복합재료

- 금속 및 금속 합금

- 세라믹 및 유리 재료

- 콘크리트 및 시멘트계 재료

- 복합재료

제6장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 가역성 고분자 시스템

- 형상 기억 재료

- 마이크로캡슐화 기술

- 혈관 네트워크 시스템

- 생물재료 시스템

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 건설 및 인프라

- 자동차 및 운송

- 항공우주 및 방위

- 의료 및 바이오메디컬

- 전자기기 및 반도체

- 에너지 및 전력 시스템

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Covestro AG

- DuPont de Nemours Inc.

- Huntsman Corporation

- Akzo Nobel NV

- Autonomic Materials Inc.

- Acciona SA

- PPG Industries Inc.

- Applied Thin Films Inc.

- Avecom NV

- Critical Materials SA

- Devan Chemicals NV

- Sensor Coating Systems Ltd.

- Tnemec Company, Inc.

The Global Self-healing Waterproofing Materials Market was valued at USD 2.2 Billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 8.2 Billion by 2034.

The market is experiencing strong growth as industries increasingly focus on long-term durability and reduced maintenance costs. These advanced materials are gaining traction in construction, automotive, and electronics applications, where exposure to moisture and harsh environmental conditions often affects performance and lifespan. In the construction sector, self-healing coatings and concretes are being incorporated to improve structural resilience and minimize lifecycle expenses. The automotive industry is adopting corrosion-resistant and damage-repairing surfaces to enhance durability. Technological progress in microencapsulation, vascular systems, and shape-memory polymers is driving the evolution of more efficient self-repair mechanisms. In addition, the integration of sensor-based systems for real-time damage detection and autonomous healing activation is shaping the next generation of waterproofing solutions. Despite these advancements, the market faces challenges related to cost-effectiveness and scalability, especially in developing economies. However, growing regulatory support for sustainable materials and global efforts toward standardization are expected to foster commercialization. Rapid infrastructure development across the Asia-Pacific region further contributes to market expansion, driven by urbanization and the rising need for long-lasting construction materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $8.2 Billion |

| CAGR | 13.9% |

The polymers and polymer composites segment held a 42.1% share in 2024 and is projected to grow at a CAGR of 13.6% through 2034. Their dominance is attributed to high adaptability, mature manufacturing capabilities, and suitability for diverse applications across multiple industries. These materials can employ a range of self-healing mechanisms, making them ideal for construction, automotive, and electronic applications. Continuous advancements in sustainable and bio-based polymer technologies, combined with growing research investments, are reinforcing their demand in environmentally conscious markets worldwide.

The reversible polymer systems segment held 35.6% share in 2024 and is expected to grow at a CAGR of 13.7% during 2025-2034. These systems are favored for their ability to undergo multiple healing cycles without significant loss in mechanical performance. Based on dynamic covalent and non-covalent bonding, they can autonomously restore their structure when exposed to stress or damage. Their compatibility with existing manufacturing processes and commercial scalability make them highly suitable for large-scale applications in sectors such as construction, electronics, and transportation. The reliability and repeatability of their healing mechanisms contribute to their widespread industrial adoption.

North America Self-healing Waterproofing Materials Market held 38.2% share in 2024. The region benefits from strong government funding, world-class research facilities, and early commercialization of advanced materials. High-performance applications in aerospace, defense, and infrastructure are driving demand, supported by significant investments in innovation from both private and public institutions. Research collaborations and funding from agencies dedicated to material science continue to strengthen North America's leadership position. The presence of major universities, startups, and established chemical companies fuels continuous product development and technological advancement, ensuring a steady supply of innovative self-healing solutions across the region.

Key companies active in the Global Self-healing Waterproofing Materials Market include Autonomic Materials Inc., DuPont de Nemours Inc., PPG Industries Inc., Avecom N.V., Covestro AG, Critical Materials S.A., Tnemec Company Inc., Devan Chemicals NV, Akzo Nobel N.V., Huntsman Corporation, Applied Thin Films Inc., Acciona S.A., and Sensor Coating Systems Ltd. To strengthen their position, leading companies are focusing on technological innovation, product diversification, and sustainable development. Many are increasing R&D investments to improve the efficiency, responsiveness, and cost-effectiveness of self-healing systems. Strategic partnerships with research organizations and industrial players are being established to accelerate product testing and commercialization. Manufacturers are expanding production capacities and developing eco-friendly formulations to meet global sustainability standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Technology type

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing infrastructure maintenance costs & repair frequency reduction needs

- 3.2.1.2 Aerospace industry demands lightweight, self-repairing composites

- 3.2.1.3 Automotive industry push for scratch-resistant & self-healing coatings

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial material costs & manufacturing complexity

- 3.2.2.2 Limited standardized testing protocols & performance validation

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in renewable energy systems

- 3.2.3.2 Medical device integration & biocompatible self-healing materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only )

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo tons)

- 5.1 Key trends

- 5.2 Polymers & polymer composites

- 5.3 Metals & metal alloys

- 5.4 Ceramics & glass materials

- 5.5 Concrete & cementitious materials

- 5.6 Composite materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo tons)

- 6.1 Key trends

- 6.2 Reversible polymer systems

- 6.3 Shape memory materials

- 6.4 Microencapsulation technologies

- 6.5 Vascular network systems

- 6.6 Biological material systems

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo tons)

- 7.1 Key trends

- 7.2 Construction & infrastructure

- 7.3 Automotive & transportation

- 7.4 Aerospace & defense

- 7.5 Healthcare & biomedical

- 7.6 Electronics & semiconductors

- 7.7 Energy & power systems

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Covestro AG

- 9.2 DuPont de Nemours Inc.

- 9.3 Huntsman Corporation

- 9.4 Akzo Nobel N.V.

- 9.5 Autonomic Materials Inc.

- 9.6 Acciona S.A.

- 9.7 PPG Industries Inc.

- 9.8 Applied Thin Films Inc.

- 9.9 Avecom N.V.

- 9.10 Critical Materials S.A.

- 9.11 Devan Chemicals NV

- 9.12 Sensor Coating Systems Ltd.

- 9.13 Tnemec Company, Inc.