|

시장보고서

상품코드

1871244

디지털 임상 솔루션 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Digital Clinical Solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

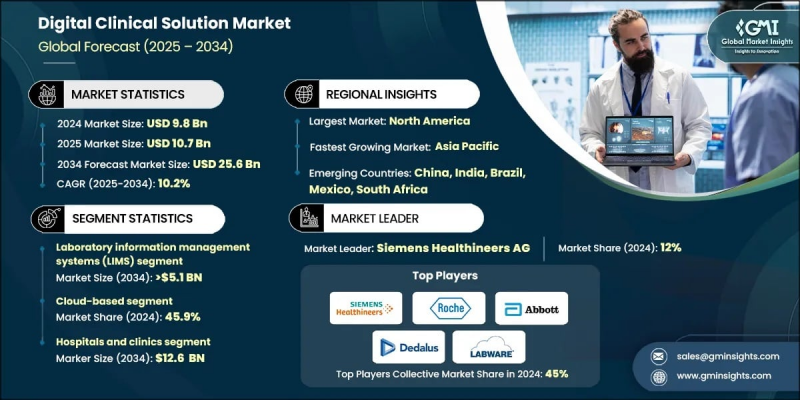

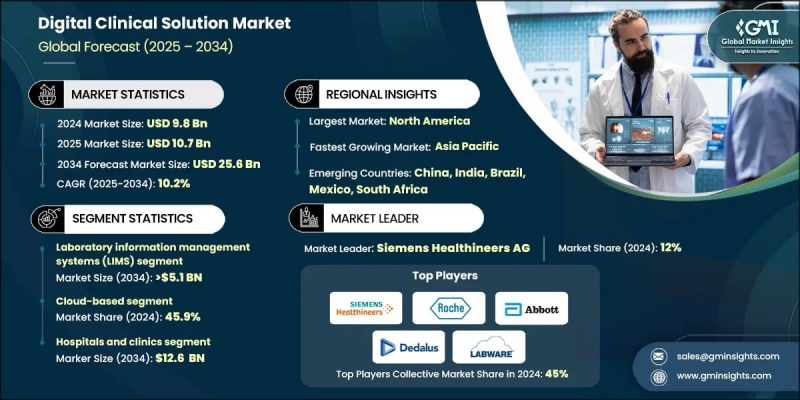

세계의 디지털 임상 솔루션 시장은 2024년 98억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 10.2%로 성장하여 256억 달러에 이를 것으로 예측됩니다.

시장의 강한 성장세는 확장성이 높고 데이터 중심 및 환자에 초점을 맞춘 의료 모델의 필요성이 증가하고 있기 때문입니다. 만성 질환 증가, 고령화, 의료 종사자의 부족 등의 과제가 증가하고 있는 가운데, 디지털 플랫폼은 세계의 의료 제공의 본연의 자세를 변화시키고 있습니다. 혁신적인 의료 기술은 협력 강화, 진단 정확성 향상 및 전체 치료 성과 개선에 기여합니다. 의료 시스템이 효율성과 가치 기반 모델로 전환하는 동안 디지털 임상 솔루션의 도입은 계속 가속화되고 있으며, 의료 기관은 환자 데이터를 관리하고 업무 프로세스를 효율화하고 운영 성능을 향상시키는 데 도움이 됩니다. 디지털 임상 솔루션은 의료 업무 간소화, 임상 프로세스 개선, 환자 결과 향상을 목적으로 하는 첨단 소프트웨어 및 기술 플랫폼을 포함합니다. 이러한 시스템은 의료기관, 검사기관, 연구 조직이 임상 데이터를 관리하고, 컴플라이언스를 확보하고, 전략적 의사결정을 위한 데이터 분석을 활용할 수 있도록 지원합니다. 전체 의료 환경에서 실시간 모니터링을 가능하게 하고 증거 기반 임상 개입을 촉진하는 데 중요한 역할을 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 98억 달러 |

| 예측 금액 | 256억 달러 |

| CAGR | 10.2% |

데이터 분석 및 보고 소프트웨어 분야는 2034년까지 연평균 복합 성장률(CAGR) 11.2%를 보일 것으로 예측됩니다. 이 확장은 임상 효율을 지원하기 위한 분석적 지식, 예측 모델링 및 성능 추적에 대한 의존도가 증가함에 기인합니다. 의료 제공업체가 데이터 중심의 성과 기반 치료에 주력함에 따라 복잡한 환자 데이터를 진단 및 치료 의사 결정을 향상시키는 실용적인 지식으로 변환하기 위해 고급 분석 도구가 필수적입니다.

클라우드 기반 배포 모델 부문은 2024년 45.9%의 점유율을 차지했습니다. 그 보급은 유연성, 저렴하고 쉬운 도입이 가능한 의료 기술에 대한 수요에 밀려 있습니다. 클라우드 인프라를 통해 의료 기관은 비싼 물리적 시스템에 의존하지 않고 환자 정보를 안전하게 관리하고 교환할 수 있습니다. 이러한 유연성은 첨단 의료 시장과 신흥 지역을 모두 지원하고 데이터 보안과 규정 준수를 유지하면서 의료 제공업체가 디지털 기능을 확장할 수 있도록 합니다.

미국의 디지털 임상 솔루션 시장은 2024년 39억 달러에 달했습니다. 미국은 첨단 의료 인프라, 디지털 의료 기술에 대한 엄청난 투자, 디지털 전환을 추진하는 강력한 정부 이니셔티브에 힘입어 세계 시장을 선도하고 있습니다. 미국이 네트워크화된 데이터 대응 의료에 주력하고 있어 병원, 진단센터, 외래 환자 네트워크 전체에 통합 임상 솔루션의 도입이 가속화되고 있습니다.

세계의 디지털 임상 솔루션 시장을 선도하는 기업으로는 Abbott Laboratories, Beckman Coulter, Bio-Rad Laboratories, CLTech, COYALab, DataArt, Dedalus, F. Hofman La Roche, GrupoBIOS SA, GTPLAN, IL Werfen, KERN IT, LabCore SRL Pixeon, Siemens Healthineers AG, Tesi Group, Tips Salud 등을 들 수 있습니다. 디지털 임상 솔루션 분야의 주요 기업들은 그 지위를 강화하기 위해 혁신, 파트너십, 포트폴리오 확대에 주력하고 있습니다. 많은 기업들이 소프트웨어 기능의 강화, 상호 운용성의 향상, 보다 좋은 임상 성과를 가져오는 AI를 활용한 분석 제공을 목적으로 연구개발에 많은 투자를 하고 있습니다. 의료 제공업체 및 기술 기업과의 전략적 제휴는 다양한 의료 에코시스템의 통합과 맞춤화 가속화에 기여하고 있습니다. 또한 기업은 세계 사업 전개를 확대하기 위해 합병, 인수 및 제품 다양화에도 힘을 쏟고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 원격 의료 및 텔레메디신 수요 증가

- 디지털 임상 소프트웨어 솔루션의 기술적 진보

- 임상 워크플로우 관리의 필요성 증가

- 업계의 잠재적 위험 및 과제

- 높은 도입 및 유지비용

- 의료 종사자 및 숙련 전문가의 부족

- 시장 기회

- 정부 주도의 디지털 헬스 시책

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 현재의 기술 동향

- 신흥기술

- 장래 시장 동향

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 소프트웨어별, 2021-2034년

- 주요 동향

- 실험실 정보 관리 시스템(LIMS)

- 실험실 정보 시스템(LIS)

- 미들웨어 솔루션

- 실시간 데이터 감시 시스템

- 재고 관리 소프트웨어

- 전사적 자원 계획(ERP)

- 임상 의사결정 지원 시스템(CDSS)

- 전자연구노트(ELN)

- 데이터 분석 및 보고 소프트웨어

제6장 시장 추계 및 예측 : 제공 형태별, 2021-2034년

- 주요 동향

- 클라우드 기반

- On-Premise

- 하이브리드

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원 및 진료소

- 연구소

- 임상 실험실 및 진단실험실

- 연구소

- 기타 용도

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- Beckman Coulter, Inc.

- Bio-Rad Laboratories, Inc

- CLTech

- COYALab

- DataArt

- Dedalus

- F. Hoffmann-La Roche Ltd.

- GrupoBIOS SA

- GTPLAN

- IL Werfen

- KERN IT

- LabCoreSoft

- LabWare

- Matrix Sistemas

- Optilink SRL

- Pixeon

- Siemens Healthineers AG

- Tesi Group

- Tips Salud

The Global Digital Clinical Solution Market was valued at USD 9.8 Billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 25.6 Billion by 2034.

The market's strong momentum is driven by the growing need for scalable, data-centric, and patient-focused healthcare models. With increasing challenges such as the rise in chronic illnesses, aging populations, and shortages in healthcare professionals, digital platforms are reshaping the delivery of care worldwide. Innovative healthcare technologies are improving coordination, diagnostic precision, and overall treatment outcomes. As healthcare systems shift toward efficiency and value-based models, the adoption of digital clinical solutions continues to accelerate, helping institutions better manage patient data, streamline workflows, and enhance operational performance. Digital clinical solutions encompass advanced software and technology platforms designed to simplify healthcare operations, improve clinical processes, and elevate patient outcomes. These systems assist healthcare facilities, laboratories, and research organizations in managing clinical data, ensuring compliance, and utilizing data analytics for strategic decision-making. They play a critical role in enabling real-time monitoring and facilitating evidence-based clinical interventions across healthcare environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.8 billion |

| Forecast Value | $25.6 billion |

| CAGR | 10.2% |

The data analytics and reporting software segment is anticipated to grow at a CAGR of 11.2% through 2034. This expansion is attributed to the growing reliance on analytical insights, predictive modeling, and performance tracking to support clinical efficiency. As healthcare providers increasingly focus on data-driven and outcome-based care, advanced analytics tools are becoming essential for transforming complex patient data into actionable insights that enhance diagnostic and therapeutic decisions.

The cloud-based deployment model segment held a 45.9% share in 2024. Its widespread adoption is fueled by the demand for flexible, affordable, and easily deployable healthcare technologies. Cloud infrastructure allows healthcare organizations to securely manage and exchange patient information without relying on costly physical systems. This flexibility supports both developed healthcare markets and emerging regions, enabling providers to expand their digital capabilities while maintaining data security and compliance.

United States Digital Clinical Solution Market reached USD 3.9 Billion in 2024. The U.S. continues to lead the global market, supported by advanced healthcare infrastructure, high investments in digital health technologies, and strong government initiatives promoting digital transformation. The nation's focus on connected, data-enabled healthcare is accelerating the implementation of integrated clinical solutions across hospitals, diagnostic centers, and outpatient networks.

Leading participants in the Global Digital Clinical Solution Market include Abbott Laboratories, Beckman Coulter Inc., Bio-Rad Laboratories Inc., CLTech, COYALab, DataArt, Dedalus, F. Hoffmann-La Roche Ltd., GrupoBIOS S.A., GTPLAN, IL Werfen, KERN IT, LabCoreSoft, LabWare, Matrix Sistemas, Optilink S.R.L., Pixeon, Siemens Healthineers AG, Tesi Group, and Tips Salud. To strengthen their position, key companies in the digital clinical solutions sector are focusing on innovation, partnerships, and portfolio expansion. Many are investing heavily in research and development to enhance software functionality, improve interoperability, and deliver AI-powered analytics for better clinical outcomes. Strategic collaborations with healthcare providers and technology firms help accelerate integration and customization across diverse healthcare ecosystems. Companies are also emphasizing mergers, acquisitions, and product diversification to expand their global footprint.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Software trends

- 2.2.3 Mode of delivery trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for remote healthcare and telemedicine

- 3.2.1.2 Technological advancements in digital clinical software solutions

- 3.2.1.3 Increasing need for clinical workflow management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Shortage of healthcare and skilled professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Government led digital health initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Software, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Laboratory information management systems (LIMS)

- 5.3 Laboratory information systems (LIS)

- 5.4 Middleware solutions

- 5.5 Real-time data monitoring systems

- 5.6 Inventory management software

- 5.7 Enterprise resource planning (ERP)

- 5.8 Clinical decision support systems (CDSS)

- 5.9 Electronic lab notebooks (ELN)

- 5.10 Data analytics and reporting software

Chapter 6 Market Estimates and Forecast, By Mode of Delivery, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premise

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Laboratories

- 7.3.1 Clinical and diagnostic laboratories

- 7.3.2 Research laboratories

- 7.4 Other End use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Beckman Coulter, Inc.

- 9.3 Bio-Rad Laboratories, Inc

- 9.4 CLTech

- 9.5 COYALab

- 9.6 DataArt

- 9.7 Dedalus

- 9.8 F. Hoffmann-La Roche Ltd.

- 9.9 GrupoBIOS S.A.

- 9.10 GTPLAN

- 9.11 IL Werfen

- 9.12 KERN IT

- 9.13 LabCoreSoft

- 9.14 LabWare

- 9.15 Matrix Sistemas

- 9.16 Optilink S.R.L.

- 9.17 Pixeon

- 9.18 Siemens Healthineers AG

- 9.19 Tesi Group

- 9.20 Tips Salud