|

시장보고서

상품코드

1871276

대체 단백질 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Alternative Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

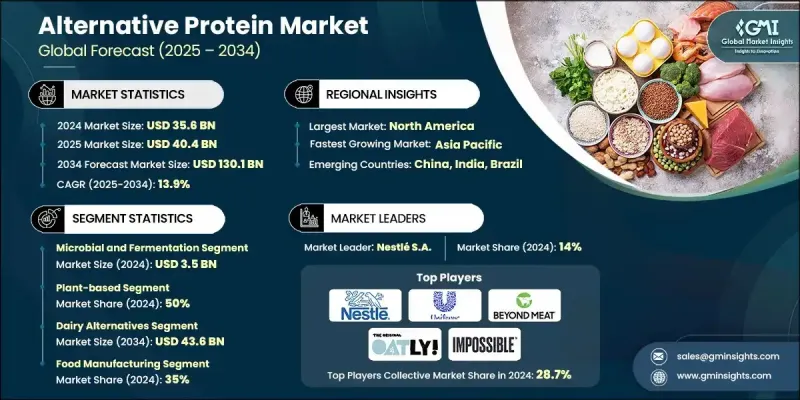

세계의 대체 단백질 시장은 2024년 356억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 13.9%로 성장하여 1,301억 달러에 이를 것으로 예측됩니다.

시장 성장은 소비자의 행동 변화, 지속가능성에 대한 요청, 지속적인 생명공학의 발전에 의해 견인되고 있습니다. 대체 단백질은 세계의 단백질 안보에 대응하면서 기존의 고기 및 유제품 산업의 환경 부하를 줄이는 미래의 식품 에코시스템에서 중요한 구성 요소로서 대두하고 있습니다. 규제면의 지원 강화, 벤처 캐피탈 투자 증가, 소매 유통망의 확충이 시장 확대를 가속화하고 있습니다. 식물성 단백질, 배양육, 발효 유래 단백질을 합치면 시장 전체의 약 85%를 차지하고 있습니다. 여러 생산 플랫폼을 결합한 하이브리드 기술의 상승으로 제품의 식감, 영양가, 저렴한 가격이 향상되었습니다. 또한 AI 지원 분자 농업 및 3D 식품 인쇄와 같은 신기술은 공정의 효율성, 확장성 및 맞춤성을 향상시키고 보다 광범위한 상업적 채택을 위한 길을 열고 있습니다. 정밀 발효 기술은 기능성을 가진 동물 유래와 동등한 단백질을 대규모로 생산함으로써 단백질 제조의 개념을 재정의하고 있습니다. 이를 통해 지속 가능한 단백질 대체품의 선택이 더욱 다양 해지고 세계 식품 공급망의 변화에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 356억 달러 |

| 예측 금액 | 1,301억 달러 |

| CAGR | 13.9% |

식물성 단백질 부문은 고기의 섬유질을 모방하는 텍스처링, 추출, 압출 기술의 큰 진보에 힘입어 2024년에 50%의 점유율을 차지했습니다. 배양 단백질 기술은 첨단 세포 배양 시스템과 통제된 성장 환경을 활용하여 가축을 사용하지 않고 실제 고기와 유사한 대안을 생산합니다. 이러한 생산 방법은 동물 농업과 관련된 윤리적 및 환경적 과제를 해결하는 확장성과 자원 효율성이 뛰어난 기술로 점점 더 잘 알려져 있습니다.

식품 제조 부문은 2024년 35%의 점유율을 차지했습니다. 제조업체 각사는 대체 단백질을 채용해 기존 제품의 리포뮬레이션이나 새로운 지속 가능한 식품의 개발을 진행하고 있습니다. 환경에 배려한 식사에의 소비자 관심이 높아지는 가운데, 식품 제조업체나 음식점은 식물성 및 세포 배양 단백질을 주류 메뉴에 도입해, 현대의 식의 기호와 세계적인 지속가능성 목표에 대한 적합을 도모하고 있습니다.

북미 대체 단백질 시장은 2024년 142억 달러 규모에 달했고 2034년까지 연평균 복합 성장률(CAGR) 10%로 확대될 것으로 전망됩니다. 이 지역은 풍부한 연구 인프라, 강력한 투자 지원, 대체 단백질 공급원에 대한 광범위한 소비자 수용의 이점을 가지고 있습니다. 북미 시장을 견인하는 것은 미국이며, 지원적인 규제 프레임워크, 최첨단 기술 진보, 성숙한 식품 가공 산업이 성장의 원동력이 되고 있습니다. 정부기관은 식물 유래, 발효, 배양 단백질 분야의 혁신을 촉진하는 가이드라인을 도입해, 지역에서의 상업화의 확대와 제품 다양화를 뒷받침하고 있습니다.

세계 대체 단백질 시장에서 사업을 전개하는 주요 기업은 Oatly Group AB, Beyond Meat Inc., Impossible Foods Inc., Perfect Day Inc., Tyson Foods Inc., Eat Just Inc., Nestle S.A., Aleph Farms Ltd., Mosa Meat B.V., Unilever PLC, Quorn Foods, Givaudan S.A., The EVERY Company, Ingredion Incorporated, Nature's Fynd Inc., Planted Foods AG, Roquette Freres S.A., Danone S.A., Upside Foods Inc., and Wilmar International Limited 등이 있습니다. 대체 단백질 시장의 기업은 첨단 생명 공학, 파트너십 및 포트폴리오의 다양화를 활용하여 시장에서의 입지를 강화하고 있습니다. 많은 기업들이 대체 단백질의 맛, 식감, 영양 프로파일을 향상시키고 동물 유래의 선택과 경쟁할 수 있도록 연구개발에 많은 투자를 하고 있습니다. 신생 기업과 주요 식품 제조업체 간의 전략적 제휴는 혁신을 촉진하고 상업화를 가속화하고 있습니다. 기업은 발효 기술과 세포 배양 기술에 의한 생산 확대를 도모함과 동시에 하이브리드 제조 모델로 비용 최적화를 진행하고 있습니다. 소매 채널과 패스트 푸드 가게를 통한 새로운 지역 시장으로의 진출은 소비자의 가용성을 더욱 높이고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 카테고리별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고: 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 대한 배려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 원료별, 2021-2034년

- 주요 동향

- 식물 유래

- 콩 기반

- 완두콩 단백질

- 밀 글루텐 및 곡물 단백질

- 콩류(녹두, 잠두, 병아리콩)

- 신규 식물

- 미생물 및 발효

- 배양 배지

- 미생물주

- 발효 기질

- 세포 배양

- 기능성 첨가물 및 원료

- 유화제 및 안정제

- 향미료 및 조미료

- 결합 및 식감 부여

- 영양 강화

- 기타

제6장 시장 추계 및 예측 : 제조 기술별, 2021-2034년

- 주요 동향

- 식물 유래

- 배양기술

- 발효

- 하이브리드 가공

- 신흥기술

- 3D 식품 인쇄 시스템

- 신규 추출 기술

- 고급 바이오프로세싱

제7장 시장 추계 및 예측 : 제품 카테고리별, 2021-2034년

- 주요 동향

- 단백질 원료 및 중간체

- 단백질 분리물 및 농축물

- 기능성 단백질 원료

- 특수 단백질

- 고기 대체품

- 갈고리

- 덩어리 고기

- 가공육(소시지, 너겟, 파티)

- 유제품 대체품

- 우유

- 치즈

- 요구르트 및 아이스크림

- 정밀 발효유 단백질

- 해산물 대체품

- 계란 대체품

- 반려동물 식품 대체품

- 영양 보조 식품 및 단백질 파우더

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 식품제조업

- 외식산업

- 퀵 서비스

- 풀 서비스

- 시설용 푸드서비스(병원, 학교, 기업용)

- 소매/소비자용

- 식료품 소매

- 전자상거래

- 전문점 및 자연 식품점

- 기타(화장품 및 퍼스널케어, 의약품)

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Aleph Farms Ltd.

- Beyond Meat Inc.

- Danone SA

- Eat Just Inc.

- Givaudan SA

- Impossible Foods Inc.

- Ingredion Incorporated

- Mosa Meat BV

- Nature's Fynd Inc.

- Nestle SA

- Oatly Group AB

- Perfect Day Inc.

- Planted Foods AG

- Quorn Foods

- Roquette Freres SA

- The EVERY Company

- Tyson Foods Inc.

- Unilever PLC

- Upside Foods Inc.

- Wilmar International Limited

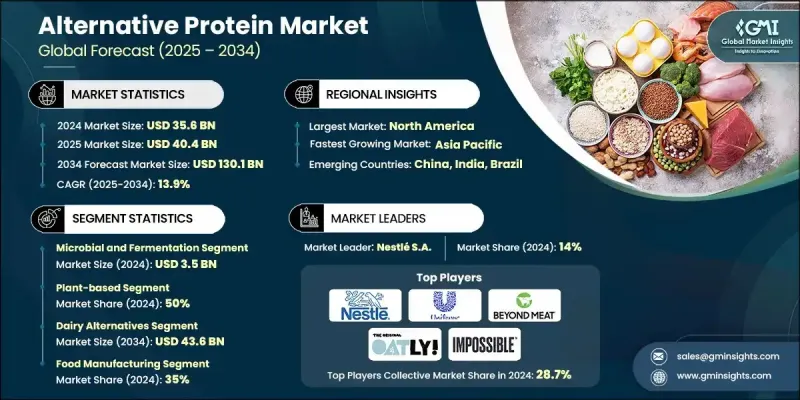

The Global Alternative Protein Market was valued at USD 35.6 billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 130.1 billion by 2034.

Market growth is driven by shifting consumer behavior, sustainability imperatives, and continuous biotechnological advancements. Alternative proteins are emerging as a crucial component of the future food ecosystem, addressing global protein security while reducing the environmental footprint of traditional meat and dairy industries. Increasing regulatory support, growing venture capital investments, and stronger retail distribution are accelerating the market's expansion. Together, plant-based proteins, cultivated meat, and fermentation-derived proteins represent approximately 85% of the overall market. The rise of hybrid technologies that combine multiple production platforms is improving product texture, nutritional quality, and affordability. In addition, emerging innovations such as AI-assisted molecular farming and 3D food printing are enhancing process efficiency, scalability, and customization, paving the way for wider commercial adoption. Precision fermentation continues to redefine protein manufacturing by producing functional, animal-identical proteins at scale, further diversifying options for sustainable protein alternatives and contributing to the ongoing transformation of the global food supply chain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.6 Billion |

| Forecast Value | $130.1 Billion |

| CAGR | 13.9% |

The plant-based proteins segment held a 50% share in 2024, supported by major progress in texturization, extraction, and extrusion technologies that mimic the fibrous texture of meat. Cultivated protein technologies utilize advanced cell culture systems and controlled growth environments to produce authentic meat analogues without the use of livestock. These production methods are increasingly recognized as scalable and resource-efficient, addressing ethical and environmental challenges associated with animal agriculture.

The food manufacturing segment held 35% share in 2024. Manufacturers are adopting alternative proteins to reformulate existing products and create new, sustainable food offerings. As consumer interest in environmentally responsible dining continues to grow, food producers and restaurants are incorporating plant and cell-based proteins into mainstream menus to align with modern dietary preferences and global sustainability goals.

North America Alternative Protein Market generated USD 14.2 billion in 2024 and will grow at a CAGR of 10% through 2034. The region benefits from robust research infrastructure, strong investment backing, and widespread consumer acceptance of alternative protein sources. The U.S. leads the North American market, driven by supportive regulatory frameworks, cutting-edge technological advancements, and a mature food processing industry. Governmental agencies have introduced guidelines that promote innovation in plant-based, fermentation, and cultivated proteins, encouraging broader commercialization and product diversity in the region.

Key companies operating in the Global Alternative Protein Market include Oatly Group AB, Beyond Meat Inc., Impossible Foods Inc., Perfect Day Inc., Tyson Foods Inc., Eat Just Inc., Nestle S.A., Aleph Farms Ltd., Mosa Meat B.V., Unilever PLC, Quorn Foods, Givaudan S.A., The EVERY Company, Ingredion Incorporated, Nature's Fynd Inc., Planted Foods AG, Roquette Freres S.A., Danone S.A., Upside Foods Inc., and Wilmar International Limited. Companies in the Alternative Protein Market are leveraging advanced biotechnology, partnerships, and portfolio diversification to strengthen their market position. Many are investing heavily in R&D to enhance the taste, texture, and nutritional profiles of protein alternatives, making them competitive with animal-derived options. Strategic collaborations between startups and large food manufacturers are fostering innovation and accelerating commercialization. Firms are scaling production through fermentation and cell-based technologies while optimizing costs with hybrid manufacturing models. Expansion into new regional markets through retail channels and quick-service restaurants is further increasing consumer accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Raw Material

- 2.2.3 Production Technology

- 2.2.4 Product Category

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa (MEA)

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Raw Material, 2021-2034 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Plant based

- 5.2.1 Soy based

- 5.2.2 Pea protein

- 5.2.3 Wheat gluten & cereal protein

- 5.2.4 Legume (mung, fava, chickpea)

- 5.2.5 Novel plant

- 5.3 Microbial & fermentation

- 5.3.1 Culture media

- 5.3.2 Microorganisms strains

- 5.3.3 Fermentation substrates

- 5.4 Cell culture

- 5.5 Functional additives & ingredients

- 5.5.1 Emulsifiers & stabilizers

- 5.5.2 Flavoring & seasoning

- 5.5.3 Binding & texturing

- 5.5.4 Nutritional fortification

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Production Technology, 2021-2034 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Plant based

- 6.3 Cultivated

- 6.4 Fermentation

- 6.5 Hybrid processing

- 6.6 Emerging technologies

- 6.6.1 3D food printing systems

- 6.6.2 Novel extraction

- 6.6.3 Advanced bioprocessing

Chapter 7 Market Estimates and Forecast, By Product Category, 2021-2034 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Protein ingredients & intermediates

- 7.2.1 Protein isolates & concentrates

- 7.2.2 Functional protein ingredients

- 7.2.3 Specialty protein

- 7.3 Meat alternatives

- 7.3.1 Ground meat

- 7.3.2 Whole cut meat

- 7.3.3 Processed meat (sausages, nuggets, patties)

- 7.4 Dairy alternatives

- 7.4.1 Milk

- 7.4.2 Cheese

- 7.4.3 Yogurt & ice cream

- 7.4.4 Precision fermentation dairy proteins

- 7.5 Seafood alternatives

- 7.6 Egg alternatives

- 7.7 Pet food alternatives

- 7.8 Nutritional supplement & protein powders

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 Food manufacturing

- 8.3 Food service

- 8.3.1 Quick service

- 8.3.2 Full service

- 8.3.3 Institutional food service (hospitals, schools, corporate)

- 8.4 Retail/consumer

- 8.4.1 Grocery retail

- 8.4.2 E-commerce

- 8.4.3 Specialty/natural food stores

- 8.5 Others (cosmetics & personal care, pharmaceuticals)

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Aleph Farms Ltd.

- 10.2 Beyond Meat Inc.

- 10.3 Danone S.A.

- 10.4 Eat Just Inc.

- 10.5 Givaudan S.A.

- 10.6 Impossible Foods Inc.

- 10.7 Ingredion Incorporated

- 10.8 Mosa Meat B.V.

- 10.9 Nature's Fynd Inc.

- 10.10 Nestle S.A.

- 10.11 Oatly Group AB

- 10.12 Perfect Day Inc.

- 10.13 Planted Foods AG

- 10.14 Quorn Foods

- 10.15 Roquette Freres S.A.

- 10.16 The EVERY Company

- 10.17 Tyson Foods Inc.

- 10.18 Unilever PLC

- 10.19 Upside Foods Inc.

- 10.20 Wilmar International Limited