|

시장보고서

상품코드

1871278

진단 분야 인공지능(AI) 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Artificial Intelligence In Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

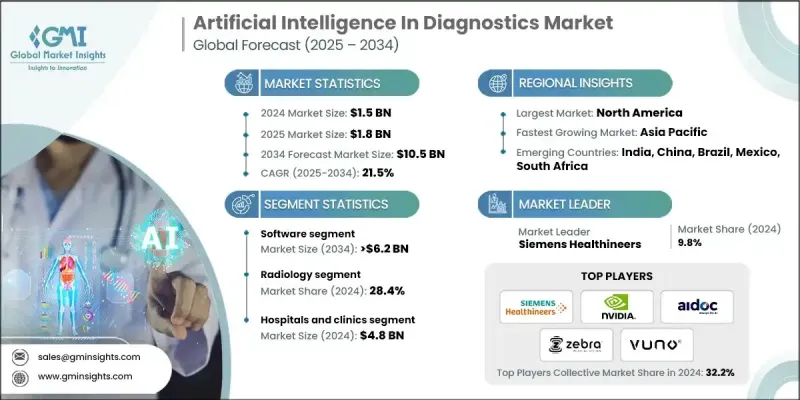

세계 진단 분야 인공지능(AI) 시장은 2024년에 15억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 21.5%로 성장해 105억 달러에 달할 것으로 예측되고 있습니다.

이 시장은 질병의 조기 발견에 대한 수요 증가, 의료 영상 진단에 대한 AI 통합, 정밀 진단, 규제 준수의 촉진 등 요인에 의해 견인되고 있습니다. AI를 활용한 솔루션은 의료 제공업체, 보험자, 생명과학기관, 의료기술 기업이 환자의 치료 성과를 향상시키고, 업무를 최적화하며, 컴플라이언스 기준을 충족할 수 있도록 하고 있습니다. 주요 솔루션은 AI 기반 이미징 소프트웨어, 디지털 병리 플랫폼, 질병의 자동 식별, 정확한 치료 계획 지원, 의료 품질 향상을 실현하는 예측 분석 도구 등을 포함합니다. 클라우드 기반 AI 용도, 디지털 병리학 및 예측 모델링의 발전으로 방사선 의학, 심장병학, 종양학 및 병리학에서 AI의 활용 범위가 확대되고 있습니다. 시장 도입은 임상 워크플로우에 대한 AI 통합을 촉진하는 규제 당국의 승인과 프레임워크에 의해 더욱 강화되고 있습니다. 의료기관, 기술공급자, 생명과학기업 간의 조사와 전략적 제휴 증가가 세계 혁신과 도입 가속을 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 105억 달러 |

| CAGR | 21.5% |

진단실 부문은 2024년에 3억 5,610만 달러의 수익을 창출하고 2034년까지 연평균 복합 성장률(CAGR)은 22.3%를 보일 것으로 예측됩니다. 실험실은 다양한 임상 응용 분야에서 의료 결과의 스크리닝, 분석 및 보고에 중요한 역할을 담당하기 때문에 AI 기술의 주요 사용자가 되었습니다. 워크플로우의 복잡화, 시료량 증가, 고스루풋 검사의 필요성이 높아지는 가운데, AI를 활용한 자동화 및 의사결정 지원 시스템에 대한 수요가 확대되고 있습니다.

방사선 의학 분야는 2024년에 28.4%의 점유율을 차지했고 2034년까지 30억 달러에 달할 것으로 예측되고 있습니다. 방사선 의학 분야는 질병을 조기 단계에서 검출하기 위한 신속하고 정확한 영상 분석이 긴급하게 요구되고 있기 때문에 진단 시장에서 인공지능의 주요 분야가 되고 있습니다. 만성 및 급성 질환의 유병률이 증가함에 따라 의료 영상 검사에 대한 수요가 증가하고 있습니다. AI 기반 방사선 의학 솔루션은 이미지 해석을 자동화하고 인위적 실수를 최소화하고 보다 신속한 결과를 제공함으로써 시기 적절한 치료 결정을 가능하게 합니다.

북미 진단 분야 인공지능(AI) 시장은 2024년 40.7%의 점유율을 차지했습니다. 이 지역의 주도적 지위는 첨단 의료 인프라, 디지털 기술의 광범위한 보급 및 엄청난 R&D 투자로 인한 것입니다. AI 구동 의료 영상 진단, 예측 분석, 디지털 병리 플랫폼은 병원, 클리닉, 실험실에서 널리 이용 가능합니다. 또한 심혈관질환, 암, 신경질환을 포함한 만성질환 증가가 이 지역에서 조기이고 정밀한 진단 수요를 견인하고 있습니다.

세계 진단 분야 인공지능(AI) 시장의 주요 기업으로는 Aidoc, AliveCor, Digital Diagnostics, Enlitic, HeartFlow, Imagen, NVIDIA, PathAI, Qure.ai, Riverain Technologies, Siemens Healthineers, Sophia Genetics, Tempus, Ultramics, Viza. 진단 분야 인공지능(AI) 시장의 기업은 자사의 지위를 강화하기 위해 다양한 전략을 실시했습니다. 구체적으로는 새로운 AI 알고리즘의 개발과 예측 정밀도의 향상을 위한 연구 개발 능력의 확충, 의료 기관·검사 기관·기술 기업과의 전략적 제휴의 구축, 기술 포트폴리오 강화를 위한 중소기업의 인수 등을 들 수 있습니다. 많은 조직은 규제 준수 및 승인 취득에 주력하여 시장 진입을 가속화하고 있습니다. 또한 클라우드 기반 및 SaaS(서비스로서의 소프트웨어) 솔루션을 우선적으로 채택하고 확장성이 뛰어난 사용자 친화적인 플랫폼을 제공하면서 보다 광범위한 시장에 전개하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 증가 경향

- AI 툴에 대한 수요 증가

- 기술적 진보

- 유리한 정부 시책과 자금 제공

- 업계의 잠재적 위험 및 과제

- 높은 조달 및 유지 관리 비용

- 데이터 프라이버시와 보안에 대한 우려

- 시장 기회

- 신흥 경제국에서의 확대

- 원격 의료 및 원격 진단과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술 상황

- 현재의 기술 동향

- AI 탑재 방사선·병리 화상 진단 소프트웨어

- 이상 검출을 신속하게 실시하는 머신러닝 알고리즘

- 병원 워크플로우와 통합된 디지털 병리 플랫폼

- 신규기술

- 통합 진단을 위한 AI 구동형 멀티모달 영상 진단

- 암 및 만성 질환의 조기 발견을 위한 심층 학습 알고리즘

- 확장 가능한 진단 솔루션을 위한 클라우드 기반 AI 플랫폼

- 현재의 기술 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

- 신흥 시장에서의 AI 진단 확대

- 원격 의료 및 원격 환자 모니터링과의 통합

- AI 통찰을 활용한 정밀의료·맞춤형 의료의 도입

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신서비스 유형 도입

- 확대 계획

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- 소프트웨어

- 서비스

- 하드웨어

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 방사선의학

- 종양학

- 심장병학

- 신경학

- 병리학

- 감염증

- 기타 용도

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원 및 진료소

- 진단실험실

- 화상 진단센터

- 기타 최종 용도

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Aidoc

- AliveCor

- Digital Diagnostics

- Enlitic

- HeartFlow

- Imagen

- NVIDIA

- PathAI

- Qure.ai

- Riverain Technologies

- Siemens Healthineers

- Sophia Genetics

- Tempus

- Ultromics

- Viz.ai

- Vuno

- Zebra Medical Vision

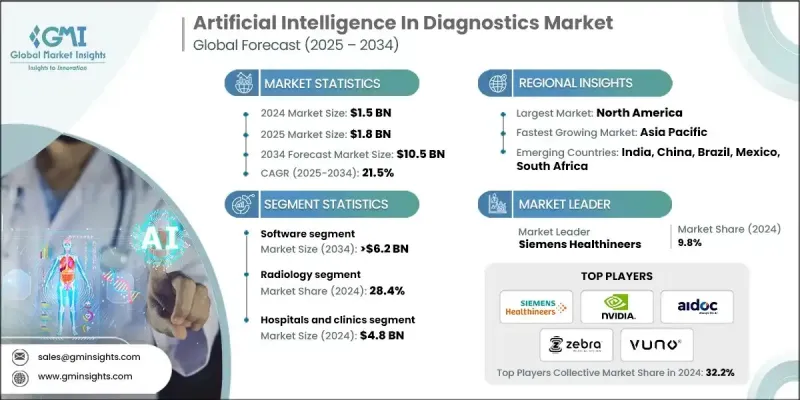

The Global Artificial Intelligence In Diagnostics Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 10.5 billion by 2034.

The market is being propelled by increasing demand for early disease detection, AI integration in medical imaging, precision diagnostics, and regulatory compliance facilitation. AI-powered solutions are enabling healthcare providers, payers, life sciences organizations, and health technology companies to improve patient outcomes, optimize operations, and meet compliance standards. Key solutions include AI-based imaging and diagnostic software, digital pathology platforms, and predictive analytics tools that automate disease identification, assist in accurate treatment planning, and enhance care quality. Advancements in cloud-based AI applications, digital pathology, and predictive modeling are broadening the use of AI across radiology, cardiology, oncology, and pathology. Market adoption is further supported by regulatory approvals and frameworks that encourage the integration of AI into clinical workflows. Increasing research investments and strategic partnerships among healthcare institutions, technology providers, and life sciences firms are driving innovation and accelerating adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 21.5% |

The diagnostic laboratories segment generated USD 356.1 million in 2024 and is expected to grow at a CAGR of 22.3% through 2034. Laboratories are major users of AI technologies due to their critical role in screening, analyzing, and reporting medical results across a variety of clinical applications. Rising workflow complexity, growing sample volumes, and the need for high-throughput testing are driving the demand for AI-driven automation and decision support systems.

The radiology segment held a 28.4% share in 2024 and is projected to reach USD 3 billion by 2034. Radiology leads the Artificial Intelligence in the diagnostics market because of the urgent need for rapid and precise imaging analysis to detect diseases at early stages. The increasing prevalence of chronic and acute conditions has raised the demand for medical imaging tests. AI-based radiology solutions automate image interpretation, minimize human error, and deliver faster results, enabling timely treatment decisions.

North America Artificial Intelligence In Diagnostics Market held a 40.7% share in 2024. The region's leadership is attributed to advanced healthcare infrastructure, widespread adoption of digital technologies, and significant research and development investments. AI-driven medical imaging, predictive analytics, and digital pathology platforms are widely available across hospitals, clinics, and laboratories. Additionally, the growing prevalence of chronic conditions, including cardiovascular diseases, cancer, and neurological disorders, is driving demand for early and precise diagnostics in the region.

Key players operating in the Global Artificial Intelligence In Diagnostics Market include Aidoc, AliveCor, Digital Diagnostics, Enlitic, HeartFlow, Imagen, NVIDIA, PathAI, Qure.ai, Riverain Technologies, Siemens Healthineers, Sophia Genetics, Tempus, Ultromics, Viz.ai, Vuno, and Zebra Medical Vision. To strengthen their position, companies in the Artificial Intelligence In Diagnostics Market are implementing a variety of strategies. These include expanding research and development capabilities to innovate new AI algorithms and improve predictive accuracy, forming strategic partnerships with healthcare providers, laboratories, and technology firms, and acquiring smaller companies to enhance technological portfolios. Many organizations are focusing on regulatory compliance and obtaining approvals to accelerate market entry. Companies are also prioritizing cloud-based and software-as-a-service solutions to reach broader markets while offering scalable, user-friendly platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Increasing demand for AI tools

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favourable government initiatives and funding

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procurement and maintenance costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging economies

- 3.2.3.2 Integration with telemedicine and remote diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered radiology and pathology imaging software

- 3.5.1.2 Machine learning algorithms for rapid anomaly detection

- 3.5.1.3 Digital pathology platforms integrated with hospital workflows

- 3.5.2 Emerging technologies

- 3.5.2.1 AI-driven multi-modal imaging for integrated diagnostics

- 3.5.2.2 Deep learning algorithms for early cancer and chronic disease detection

- 3.5.2.3 Cloud-based AI platforms for scalable diagnostics solutions

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Expansion of AI diagnostics in emerging markets

- 3.9.2 Integration with telemedicine and remote patient monitoring

- 3.9.3 Adoption of precision and personalized medicine using AI insights

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.4 Hardware

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Radiology

- 6.3 Oncology

- 6.4 Cardiology

- 6.5 Neurology

- 6.6 Pathology

- 6.7 Infectious diseases

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Diagnostic laboratories

- 7.4 Imaging centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aidoc

- 9.2 AliveCor

- 9.3 Digital Diagnostics

- 9.4 Enlitic

- 9.5 HeartFlow

- 9.6 Imagen

- 9.7 NVIDIA

- 9.8 PathAI

- 9.9 Qure.ai

- 9.10 Riverain Technologies

- 9.11 Siemens Healthineers

- 9.12 Sophia Genetics

- 9.13 Tempus

- 9.14 Ultromics

- 9.15 Viz.ai

- 9.16 Vuno

- 9.17 Zebra Medical Vision