|

시장보고서

상품코드

1871284

롤러 베어링 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Roller Bearings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

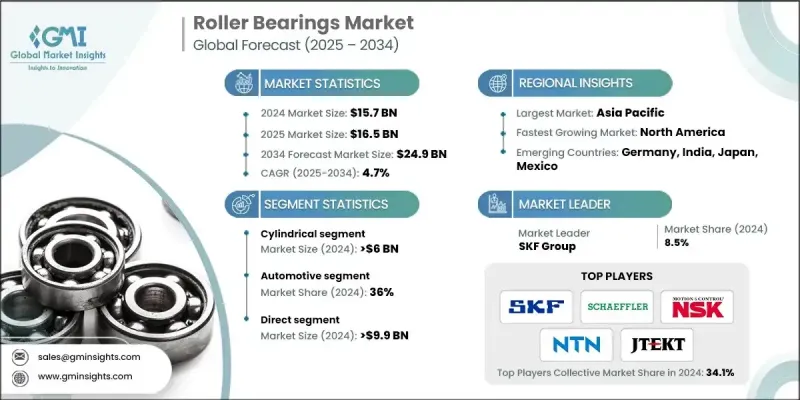

세계의 롤러 베어링 시장은 2024년 157억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 4.7%로 성장하여 249억 달러에 이를 것으로 예측됩니다.

롤러 베어링은 건설, 광업, 제조업 등 신뢰성과 내구성이 효율적인 조업의 열쇠가 되는 산업에 있어서 필수적인 부품으로서 기능하고 있습니다. 산업분야 전체에서의 자동화와 첨단 기계의 도입 확대는 고하중, 고압력, 극단적인 온도변동에 대응 가능한 고성능 베어링 수요를 견인하고 있습니다. 산업 자동화와 에너지 절약 시스템을 추진하는 각국 정부의 이니셔티브도 시장 성장을 더욱 가속화하고 있습니다. 연구개발에 대한 주력이 진행되는 가운데 롤러베어링은 가혹한 산업환경에서 성능, 정밀도, 수명 향상을 실현하는 방향으로 진화를 계속하고 있습니다. 신재생에너지와 스마트제조를 지원하는 세계적인 노력도 시장의 진화에 계속 영향을 주어 효율성과 가동안정성을 높이는 혁신을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 157억 달러 |

| 예측 금액 | 249억 달러 |

| CAGR | 4.7% |

원통형 롤러 베어링 부문은 2024년 60억 달러에 달했습니다. 이것은 무거운 레이디얼 하중을 지원하고 빠르고 효율적으로 작동하는 베어링에 대한 수요에 견인되었습니다. 이 베어링은 산업용 모터, 제조 및 자동차 시스템에서 널리 채택됩니다. 산업용 모터만으로 제조업의 총 에너지 소비량의 절반 이상을 차지하고 있으며, 원통형 롤러 베어링은 그 운전 효율 향상에 중요한 역할을 하고 있습니다. 이로 인해 에너지 절약과 유지 보수 비용 절감을 요구하는 업계 전반에 걸쳐 강한 수요가 발생합니다.

직접 판매 부문은 2024년 99억 달러에 이르렀으며 OEM과의 직접적인 파트너십 유지의 효과로 인해 롤러 베어링 시장을 독점하고 있습니다. 직접 유통을 통해 제조업체는 맞춤형 솔루션을 제공하는 동시에 원활한 커뮤니케이션과 기술 협력을 보장 할 수 있습니다. 이 접근법은 정확도, 품질 보증 및 성능 신뢰성이 OEM의 주요 의사 결정 요인이 되는 자동차, 항공우주, 중장비 제조와 같은 고부가가치 분야에서 특히 유용합니다.

미국 롤러 베어링 시장은 2024년 77.1%의 점유율을 차지했습니다. 이 나라의 첨단 제조 에코시스템, 견고한 자동차 산업 기반, 확대를 계속하는 항공우주 및 중기 섹터가 성장의 주요인입니다. 지속적인 기술 개발과 주요 업계 선수의 존재는 미국을 지역의 주도적 세력으로 강화하고 산업용 롤러 베어링의 국내외 수요를 지원합니다.

세계 롤러 베어링 시장의 주요 기업은 NBI Bearings Europe, HKT Bearings, C&U Group, Minebea, NTN, NSK, SKF, Schaeffler Group, The Timken Company, RBC Bearings, Brammer, Daido Metal, Harbin Bearing Manufacturing, JTEKT, Rexnord 등이 있습니다. 롤러 베어링 시장의 기업은 기술 혁신, 제품 다양화, 전략적 제휴에 주력하여 세계 존재감을 강화하고 있습니다. 연구개발에 엄청난 투자를 통해 가혹한 환경에서도 효율적으로 작동하는 첨단적이고 내구성이 높은 베어링을 개발할 수 있습니다. 많은 기업들이 자동화와 스마트 제조 공정을 도입하여 정확도 향상과 생산 비용 절감을 도모하고 있습니다. 산업, 자동차, 항공우주 분야의 OEM 제조업체와의 협력을 통해 장기 계약 및 제품 맞춤화 기회를 확보하고 있습니다. 지역 제조 기지와 공급망 확대로 신속한 납품과 비용 효율성을 높일 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업 확대 및 자동화

- 자동차 산업의 성장

- 기술적 진보와 제품 혁신

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용

- 대체 기술의 상승

- 기회

- 에너지 절약형 및 스마트 롤러 베어링 시스템

- 산업 자동화 및 스마트 제조의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- 무역 통계(HS코드-8482)

- 주요 수입국

- 주요 수출국

- 갭 분석

- 리스크 평가 및 경감책

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 유형별, 2021-2034년

- 주요 동향

- 원통형

- 테이퍼 가공

- 구형

- 기타

- 바늘

- 스러스트

- 분할

제6장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 강재

- 세라믹

- 폴리머

- 하이브리드

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 기어박스

- 전기 모터

- 펌프 및 컴프레서

- 풍력 터빈

- 컨베이어

- 공작기계

제8장 시장 추계 및 예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 자동차

- 농업

- 전기

- 광업 및 건설업

- 철도 및 항공우주산업

- 자동차 애프터마켓

- 기타

제9장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 직접 판매

- 간접

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Brammer

- C&U Group

- Daido Metal

- Harbin Bearing Manufacturing

- HKT Bearings

- JTEKT

- Minebea

- NBI Bearings Europe

- NSK

- NTN

- RBC Bearings

- Rexnord

- Schaeffler Group

- SKF

- The Timken Company

The Global Roller Bearings Market was valued at USD 15.7 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 24.9 billion by 2034.

Roller bearings serve as essential components across industries such as construction, mining, and manufacturing, where reliability and durability are key to efficient operations. The growing adoption of automation and advanced machinery across industrial sectors has driven the need for high-performance bearings capable of handling heavy loads, high pressure, and extreme temperature variations. Governments promoting industrial automation and energy-efficient systems are further fueling market growth. With increased focus on research and development, roller bearings are evolving to deliver improved performance, precision, and longevity in demanding industrial environments. Global initiatives supporting renewable energy and smart manufacturing also continue to influence the market's evolution, encouraging innovations that enhance efficiency and operational stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.7 Billion |

| Forecast Value | $24.9 Billion |

| CAGR | 4.7% |

The cylindrical roller bearing segment reached USD 6 billion in 2024, driven by demand for bearings that support heavy radial loads and perform efficiently at high speeds. These bearings are widely adopted in industrial motors, manufacturing, and automotive systems. Industrial motors alone account for more than half of total energy consumption in manufacturing, and cylindrical bearings play a crucial role in improving their operational efficiency, thereby driving strong demand across industries seeking energy savings and reduced maintenance costs.

The direct sales segment reached USD 9.9 billion in 2024, dominating the roller bearings market due to its effectiveness in maintaining direct partnerships with OEMs. Direct distribution enables manufacturers to deliver customized solutions while ensuring seamless communication and technical collaboration. This approach is particularly beneficial in high-value sectors such as automotive, aerospace, and heavy equipment manufacturing, where precision, quality assurance, and performance reliability are key decision factors for OEMs.

U.S. Roller Bearings Market held 77.1% share in 2024. The country's advanced manufacturing ecosystem, strong automotive base, and expanding aerospace and heavy machinery sectors are major contributors to this growth. Continuous technological development and the presence of key industry players have reinforced the U.S. as a dominant force in the region, supporting both domestic and global demand for industrial-grade roller bearings.

Major players in the Global Roller Bearings Market include NBI Bearings Europe, HKT Bearings, C&U Group, Minebea, NTN, NSK, SKF, Schaeffler Group, The Timken Company, RBC Bearings, Brammer, Daido Metal, Harbin Bearing Manufacturing, JTEKT, and Rexnord. Companies in the Roller Bearings Market are focused on technological innovation, product diversification, and strategic partnerships to strengthen their global presence. Heavy investment in R&D enables them to develop advanced, high-durability bearings that perform efficiently under extreme conditions. Many players are adopting automation and smart manufacturing processes to improve precision and reduce production costs. Collaborations with OEMs across industrial, automotive, and aerospace sectors ensure long-term contracts and product customization opportunities. Expanding regional manufacturing bases and supply chains allows for faster delivery and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Application

- 2.2.5 End use Industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial expansion and automation

- 3.2.1.2 Automotive industry growth

- 3.2.1.3 Technological advancements and product innovation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Emergence of alternative technologies

- 3.2.3 Opportunities

- 3.2.3.1 Energy-efficient and smart roller bearing systems

- 3.2.3.2 Growth in industrial automation and smart manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code-8482)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Tapered

- 5.4 Spherical

- 5.5 Others

- 5.5.1 Needle

- 5.5.2 Thrust

- 5.5.3 Split

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Ceramic

- 6.4 Polymer

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Gearboxes

- 7.3 Electric Motors

- 7.4 Pumps & Compressors

- 7.5 Wind Turbines

- 7.6 Conveyors

- 7.7 Machine Tools

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Agriculture

- 8.4 Electrical

- 8.5 Mining & Construction

- 8.6 Railway & Aerospace

- 8.7 Automotive aftermarket

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Brammer

- 11.2 C&U Group

- 11.3 Daido Metal

- 11.4 Harbin Bearing Manufacturing

- 11.5 HKT Bearings

- 11.6 JTEKT

- 11.7 Minebea

- 11.8 NBI Bearings Europe

- 11.9 NSK

- 11.10 NTN

- 11.11 RBC Bearings

- 11.12 Rexnord

- 11.13 Schaeffler Group

- 11.14 SKF

- 11.15 The Timken Company