|

시장보고서

상품코드

1871287

인공 혈관 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Vascular Graft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

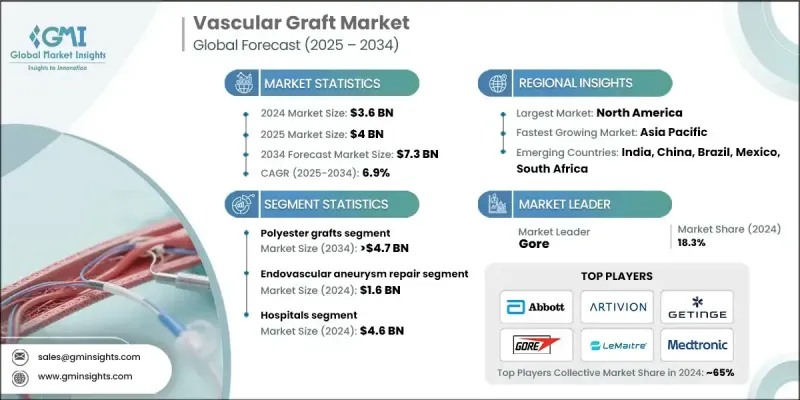

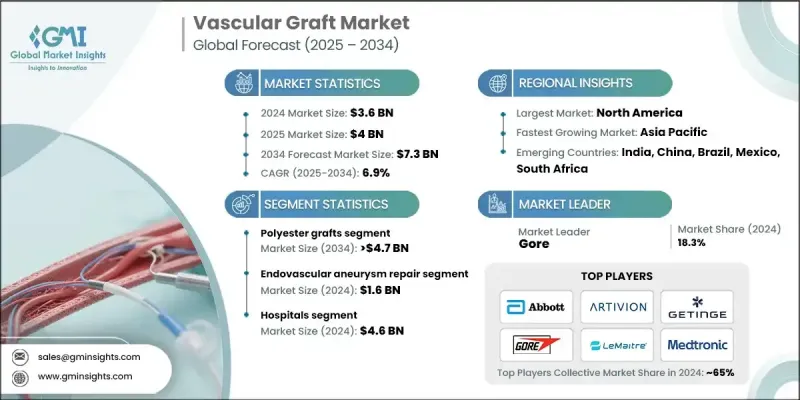

세계 인공 혈관 시장은 2024년 36억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 6.9%로 성장하여 73억 달러에 이를 것으로 예측됩니다.

시장 확대의 주요 요인으로는 심혈관 질환의 유병률 상승, 기술 혁신, 말기 신부전(ESRD)의 발생률 증가, 세계 외과적 개입 증가 등이 있습니다. 인공 혈관은 손상되거나 질병이 있는 혈관을 대체, 수리 또는 우회하여 정상적인 혈류를 회복하도록 설계된 의료기기입니다. 이러한 이식편은 합성 재료, 생체 조직 또는 그 하이브리드로부터 제조됩니다. 심혈관 질환, 동맥류, 혈액 투석 접근 등의 치료에 널리 사용됩니다. 바이오 엔지니어링 이식편, 헤파린 코팅 ePTFE 이식편, 하이브리드 재료 등의 최근 발전은 적합성을 향상시키고, 혈전증 위험을 줄이고, 장기적인 개존성을 향상시켰습니다. 또한 저침습 및 혈관내 치료에 대한 선호 증가, 조직공학 그래프트 및 생분해성 그래프트의 사용 증가, 약물용출형 및 코팅 그래프트의 채용, 신흥 시장에서의 확대 등의 요인도 함께 시장은 혜택을 받고 있으며, 이들이 종합적으로 업계의 성장을 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 36억 달러 |

| 예측 금액 | 73억 달러 |

| CAGR | 6.9% |

폴리에스터 이식편 부문은 2024년 62.3%의 점유율을 차지했습니다. 폴리에스테르 이식편은 내구성, 우수한 생체적합성 및 혈관 수복 및 우회 수술에서 장기적인 개존성이 입증되었기 때문에 선호하고 사용됩니다. 대동맥 및 말초 우회술에서 풍부한 임상 실적과 일관된 성능으로 외과의사로부터 높은 신뢰를 획득하고 혈관 수술에서 클래식이 되었습니다.

혈액 투석 접근 분야는 2034년까지 연평균 복합 성장률(CAGR) 6.3%를 보일 것으로 예측됩니다. 말기 신부전(ESRD) 환자 증가와 장기적인 혈액 투석을 필요로 하는 환자 수 증가는 인공 혈관 수요를 견인하고 있습니다. 개존성을 향상시키고 감염 위험을 최소화하는 이식편 설계의 혁신은 이 분야의 성장을 더욱 강화하고 있습니다.

북미의 인공 혈관 시장은 2024년 32.2%의 점유율을 차지했습니다. 관상 동맥 질환, 말초 동맥 질환 및 대동맥류 발생률이 높아지면서 이 지역의 강한 수요에 기여합니다. 전문 혈관 수술센터를 갖추고 있으며 고급 수술 기술을 이용할 수 있는 정평이 있는 병원이 개복 수술과 혈관 내 이식편 수술을 모두 채택하도록 지원합니다.

세계의 인공 혈관 시장의 주요 기업으로는 Cook Medical, Gore, Terumo, Medtronic, B. Braun, Merit Medical Systems, LeMaitre, Abbott, Endologix, Vascular Graft Solutions, MicroPort, Artivion, BD (Becton, Dickinson & Company), Getinge, Cordis 등이 있습니다. 인공 혈관 시장의 기업은 시장에서의 지위를 강화하기 위해 여러 전략을 채택하고 있습니다. 이들은 개존성, 생체적합성이 향상되고 합병증 위험이 감소된 혁신적인 이식편을 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 전략적 합병, 인수 및 제휴는 제품 포트폴리오 및 지역 배포의 확대에 기여합니다. 많은 기업들은 약물용출형, 생체공학, 하이브리드 그래프트 등의 기술적 진보에 주력하고 있습니다. 마케팅 캠페인, 외과 의사 교육 프로그램, 강력한 병원과의 제휴로 브랜드 인지도와 신뢰성이 향상되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계적으로 증가하는 만성질환의 수

- 개발도상국에서 말기신질환 증가 경향

- 선진국의 기술적 진보

- 장기 이식 증가

- 업계의 잠재적 위험 및 과제

- 개발도상국에서의 숙련인력의 부족

- 이식편 감염 및 혈전증의 위험

- 시장 기회

- 생체 흡수성 그래프트 및 하이브리드 그래프트의 개발

- 이식편 개발에 있어서의 3D 프린팅 기술 채용 확대

- 성장 촉진요인

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술 상황

- 현재의 기술 동향

- 신흥기술

- 소비자 분석

- 밸류체인 분석

- 장래 시장 동향

- 주요 투자 및 확대 동향

- 이식편의 유형에 관한 개요

- 이식 재료 및 코팅의 혁신

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신원료의 발매

- 확장 계획

제5장 시장 추계 및 예측 : 원료별, 2021-2034년

- 주요 동향

- 폴리에스테르제 그래프트

- ePTFE 그래프트

- 생체 합성 이식편

- 폴리우레탄제 그래프트

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 혈관내 동맥류 수복술

- 복부 대동맥류 수복술

- 흉부 대동맥류 수복술

- 혈액 투석용 액세스

- 말초 혈관 복구

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- Artivion

- B. Braun

- BD(Becton, Dickinson &Company)

- Cook Medical

- Cordis

- Endologix

- Getinge

- Gore

- LeMaitre

- Medtronic

- Merit Medical Systems

- MicroPort

- Terumo

- Vascular Graft Solutions

The Global Vascular Graft Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 7.3 billion by 2034.

The market expansion is driven by the rising prevalence of cardiovascular disorders, technological innovations, and the growing incidence of end-stage renal disease (ESRD), along with an increase in surgical interventions worldwide. Vascular grafts are medical devices designed to replace, repair, or bypass damaged or diseased blood vessels, restoring normal blood flow. These grafts are manufactured from synthetic materials, biological tissues, or a hybrid of both. They are widely used in treatments for cardiovascular conditions, aneurysms, and hemodialysis access. Recent advancements, such as bioengineered grafts, heparin-coated ePTFE grafts, and hybrid materials, enhance compatibility, reduce thrombosis risk, and improve long-term patency. The market is also benefiting from the growing preference for minimally invasive and endovascular procedures, increasing use of tissue-engineered and biodegradable grafts, adoption of drug-eluting and coated grafts, and expansion in emerging markets, collectively propelling industry growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 6.9% |

The polyester grafts segment held a 62.3% share in 2024. Polyester grafts are preferred for their durability, excellent biocompatibility, and proven long-term patency in vascular repair and bypass procedures. Their extensive clinical history and consistent performance in aortic and peripheral bypass surgeries have earned them high trust among surgeons, making them a staple in vascular procedures.

The hemodialysis access segment is expected to grow at a CAGR of 6.3% through 2034. Rising cases of ESRD and an increasing number of patients requiring long-term hemodialysis are driving demand for vascular grafts. Innovations in graft design that improve patency and minimize infection risks further support growth in this segment.

North America Vascular Graft Market held a 32.2% share in 2024. High rates of coronary artery disease, peripheral artery disease, and aortic aneurysms contribute to the region's strong demand. Well-established hospitals with specialized vascular surgery centers and access to advanced surgical technologies support the adoption of both open and endovascular graft procedures.

Key players in the Global Vascular Graft Market include Cook Medical, Gore, Terumo, Medtronic, B. Braun, Merit Medical Systems, LeMaitre, Abbott, Endologix, Vascular Graft Solutions, MicroPort, Artivion, BD (Becton, Dickinson & Company), Getinge, and Cordis. Companies in the Vascular Graft Market are adopting multiple strategies to strengthen their market position. They are heavily investing in research and development to create innovative grafts with improved patency, biocompatibility, and reduced complication risks. Strategic mergers, acquisitions, and partnerships help expand product portfolios and regional reach. Many firms focus on technological advancements, including drug-eluting, bioengineered, and hybrid grafts. Marketing campaigns, surgeon education programs, and strong hospital collaborations improve brand recognition and trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Raw Material trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number chronic diseases worldwide

- 3.2.1.2 Growing number of end-stage renal disorders in developing economies

- 3.2.1.3 Technological advancements in developed countries

- 3.2.1.4 Rise in organ transplantation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled personnel in developing countries

- 3.2.2.2 Risk of graft infection and thrombosis

- 3.2.3 Market opportunities

- 3.2.3.1 Development of bioresorbable and hybrid grafts

- 3.2.3.2 Rising adoption of 3D printing in graft development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 LAMEA

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Consumer analysis

- 3.8 Value chain analysis

- 3.9 Future market trends

- 3.10 Key investment and expansion trends

- 3.11 Overview of graft types

- 3.12 Innovations in graft materials and coatings

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New raw material launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Raw Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Polyester grafts

- 5.3 ePTFE grafts

- 5.4 Biosynthetic grafts

- 5.5 Polyurethane grafts

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Endovascular aneurysm repair

- 6.2.1 Abdominal aortic aneurysm repair

- 6.2.2 Thoracic aortic aneurysm repair

- 6.3 Hemodialysis access

- 6.4 Peripheral vascular repair

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Artivion

- 9.3 B. Braun

- 9.4 BD (Becton, Dickinson & Company)

- 9.5 Cook Medical

- 9.6 Cordis

- 9.7 Endologix

- 9.8 Getinge

- 9.9 Gore

- 9.10 LeMaitre

- 9.11 Medtronic

- 9.12 Merit Medical Systems

- 9.13 MicroPort

- 9.14 Terumo

- 9.15 Vascular Graft Solutions