|

시장보고서

상품코드

1871295

LDT 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Laboratory Developed Tests Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

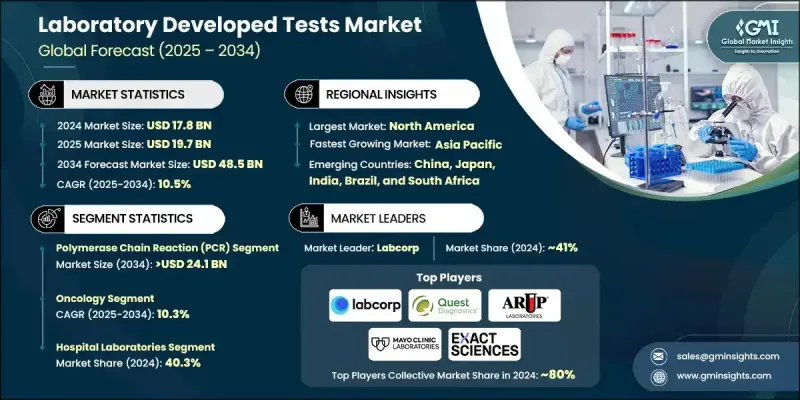

세계 LDT 시장은 2024년 178억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 10.5%로 성장하여 485억 달러에 이를 것으로 예측됩니다.

이 급속한 성장은 주로 다음 요인에 의해 견인됩니다. 질병의 조기 발견에 대한 의식의 증가, 감염증 및 만성 질환의 유병률 증가, 암이나 유전성 질환의 사례 수 증가입니다. 단일 검사실 내에서 개발·제조·사용되는 진단 검사인 LDT는 맞춤형 의료에 혁명을 가져와 질병 관리 개선과 임상 판단 지원을 실현하고 있습니다. 특정 환자 요구에 맞게 신속하게 검사를 혁신하고 적응시키는 능력은 특히 정밀하고 개별화된 진단을 필요로 하는 복잡한 질환에서 의료를 변화시키고 있습니다. 각 회사는 고급 차세대 시퀀싱(NGS) 패널에서 고급 분자진단, 바이오 마커 분석에 이르기까지 광범위한 검사를 제공합니다. 이러한 검사는 고처리량 유전체학, AI 구동 알고리즘, 바이오인포매틱스 플랫폼, 클라우드 지원 데이터 통합 등 최첨단 기술을 활용합니다. 암 발생률이 상승을 계속하는 가운데 조기, 정확 및 개별화된 진단에 대한 수요는 높아지고 있습니다. LDT는 유전자 변이, 바이오마커, 질병 하위유형의 신속한 검출을 가능하게 하고, 표적 치료의 개별화 및 환자 결과의 향상에 필수적인 역할을 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 178억 달러 |

| 예측 금액 | 485억 달러 |

| CAGR | 10.5% |

면역조직화학(IHC) 분야는 세계적인 암 부담 증가에 따라 2034년까지 연평균 복합 성장률(CAGR)은 9.9%를 보일 것으로 예측됩니다. IHC는 종양 마커의 식별, 치료 선택의 지원, 맞춤형 의료 전략의 지원에 필수적이며, 종양학 진단의 지위를 확고히 하고 있습니다.

전염병 분야는 2034년까지 연평균 복합 성장률(CAGR) 11%에서 바이러스성 및 박테리아성 전염병의 세계 발생률이 증가함에 따라 성장할 것으로 예측됩니다. LDT(Lab Development Test)가 제공하는 유연성과 신속한 결과 제공은 감염증 발생 시의 대응이나 일상적인 감염증 진단에 있어서 필수적인 존재가 되고 있습니다.

미국의 LDT 시장은 2024년 68억 달러 규모에 이르렀습니다. 이것은 특히 종양학, 감염증, 유전성 질환 분야에서 복잡한 검사의 개발 및 검증이 가능한 병원이나 참조 검사기관의 강력한 네트워크가 기여하고 있습니다. 북미, 특히 미국의 규제 환경은 기존보다 LDT의 혁신을 촉진하고 있으며, 검사 기관이 새로운 건강 과제에 대응할 수 있도록 하고 있습니다. AI, 자동화, 차세대 시퀀싱 기술의 통합은 성장을 지속적으로 촉진하고 있으며, 이 지역은 첨단 진단 개발의 선두 주자로 자리잡고 있습니다.

세계 실험실 개발 검사 시장의 주요 기업으로는 IgX, Freeome, GUARDANT, HealthBio, veracyte, BioReference, MicroGenDX, prognomiQ, MAYO CLINIC LABORATORIES, SONIC HEALTHCARE USA, GeneDx 등이 있습니다. 검사 개발 시장의 기업은 AI, 머신러닝, 차세대 시퀀싱 등의 첨단 기술을 통합하여 검사 정밀도와 소요 시간의 단축을 도모함으로써 지속적인 혁신에 주력하고 있습니다. 병원, 연구기관, 바이오테크놀러지 기업과의 전략적 제휴 및 파트너십을 통해 검사 포트폴리오의 확충과 시장 진입의 신속화를 실현하고 있습니다. 바이오인포매틱스 및 클라우드 컴퓨팅에 대한 투자는 고급 데이터 분석과 환자 정보의 원활한 통합을 촉진하고 진단 정확도를 향상시킵니다. 또한 각 회사는 규제 준수와 변화하는 의료 상황에 대한 신속한 적응을 우선하여 경쟁 우위를 유지하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 암 및 유전성 질환의 발생률 증가

- 감염증 및 만성 질환 증가 경향

- 질병의 조기 발견에 대한 인식과 주목의 고조

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 대체 검사 방법의 이용 가능성

- 시장 기회

- 자동화와 디지털 병리의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 상환 시나리오

- LDT 가격 설정 모델과 전략

- 임상 검사 요금 체계(CLFS)의 영향 분석

- 메디케어 파트 B 보장 범위 및 상환률

- 규제 상황

- 기술적 상황

- 현행 기술

- 신규 기술

- 장래 시장 동향

- 밸류체인 분석

- 소비자 행동 분석

- 투자 상황

- 가격 분석, 2024년

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 중합효소 연쇄반응(PCR)

- 차세대 시퀀싱(NGS)

- 면역조직화학(IHC)

- 기타 기술

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 종양학

- 감염증

- 유전성 질환 및 희귀질환

- 심장병학

- 자가면역 질환 및 염증성 질환

- 기타 용도

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원 검사실

- 민간검사기관

- 전문 진단실험실

- 기타 용도

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- ARUP Laboratories

- BioReference

- EXACT SCIENCES

- Freenome

- GeneDx

- GUARDANT

- HealthBio

- IgX

- Labcorp

- MAYO CLINIC LABORATORIES

- MicroGenDX

- prognomiQ

- Quest Diagnostics

- SONIC HEALTHCARE USA

- Veracyte

The Global Laboratory Developed Tests Market was valued at USD 17.8 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 48.5 billion by 2034.

The rapid growth is largely driven by increasing awareness around early disease detection, the rising prevalence of infectious and chronic illnesses, and a growing number of cancer and genetic disorder cases. LDTs, which are diagnostic tests created, manufactured, and used within a single laboratory, revolutionize personalized medicine, improving disease management and aiding clinical decision-making. Their ability to rapidly innovate and tailor tests to specific patient needs is transforming healthcare, especially in the context of complex conditions that require precise and individualized diagnostics. Companies offer an extensive range of tests, from advanced next-generation sequencing (NGS) panels to sophisticated molecular diagnostics and biomarker assays. These tests utilize state-of-the-art technologies, including high-throughput genomics, AI-driven algorithms, bioinformatics platforms, and cloud-enabled data integration. As cancer rates continue to climb, the demand for early, accurate, and personalized diagnostics intensifies. LDTs play a crucial role by enabling the swift detection of genetic mutations, biomarkers, and disease subtypes, which are vital for tailoring targeted treatments and enhancing patient outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.8 Billion |

| Forecast Value | $48.5 Billion |

| CAGR | 10.5% |

The immunohistochemistry (IHC) segment is anticipated to grow at a CAGR of 9.9% through 2034, due to the increasing global burden of cancer. IHC is essential for identifying tumor markers, assisting treatment choices, and supporting personalized medicine strategies, solidifying its place in oncology diagnostics.

The infectious diseases segment is expected to grow at a 11% CAGR through 2034, driven by the rising global incidence of viral and bacterial infections. The flexibility and rapid turnaround offered by LDTs make them indispensable for managing outbreaks and everyday infectious disease diagnosis.

U.S. Laboratory Developed Tests Market generated USD 6.8 billion in 2024, benefiting from a robust network of hospitals and reference labs capable of developing and validating complex tests, particularly in oncology, infectious diseases, and genetic conditions. The regulatory environment in North America, especially the U.S., has traditionally encouraged innovation in LDTs, allowing labs to respond to emerging health challenges. The integration of AI, automation, and next-generation sequencing technologies continues to fuel growth, establishing the region as a leader in advanced diagnostic development.

Leading companies in the Global Laboratory Developed Tests Market include IgX, Freenome, GUARDANT, HealthBio, veracyte, BioReference, MicroGenDX, prognomiQ, MAYO CLINIC LABORATORIES, SONIC HEALTHCARE USA, and GeneDx. Companies in the Laboratory Developed Tests Market focus on continuous innovation by integrating cutting-edge technologies such as AI, machine learning, and next-generation sequencing to enhance test accuracy and turnaround time. Strategic collaborations and partnerships with hospitals, research institutes, and biotech firms enable expanded test portfolios and faster market entry. Investments in bioinformatics and cloud computing facilitate advanced data analytics and seamless integration of patient information, improving diagnostic precision. Additionally, companies prioritize regulatory compliance and agile adaptation to changing health landscapes to maintain a competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of cancer and genetic disorders

- 3.2.1.2 Rising prevalence of infectious and chronic diseases

- 3.2.1.3 Growing awareness and focus on early disease detection

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Availability of alternative testing methods

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of automation & digital pathology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.4.1 LDT pricing models & strategies

- 3.4.2 Clinical laboratory fee schedule (CLFS) impact analysis

- 3.4.3 Medicare Part B coverage & reimbursement rates

- 3.5 Regulatory landscape

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Consumer behavior analysis

- 3.10 Investment landscape

- 3.11 Pricing analysis, 2024

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Polymerase chain reaction (PCR)

- 5.3 Next-generation sequencing (NGS)

- 5.4 Immunohistochemistry (IHC)

- 5.5 Other technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Infectious diseases

- 6.4 Genetic & rare disorders

- 6.5 Cardiology

- 6.6 Autoimmune & inflammatory conditions

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital laboratories

- 7.3 Private reference labs

- 7.4 Specialty diagnostic labs

- 7.5 Other End use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ARUP Laboratories

- 9.2 BioReference

- 9.3 EXACT SCIENCES

- 9.4 Freenome

- 9.5 GeneDx

- 9.6 GUARDANT

- 9.7 HealthBio

- 9.8 IgX

- 9.9 Labcorp

- 9.10 MAYO CLINIC LABORATORIES

- 9.11 MicroGenDX

- 9.12 prognomiQ

- 9.13 Quest Diagnostics

- 9.14 SONIC HEALTHCARE USA

- 9.15 Veracyte