|

시장보고서

상품코드

1871314

생분해성 폴리머 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Biodegradable Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

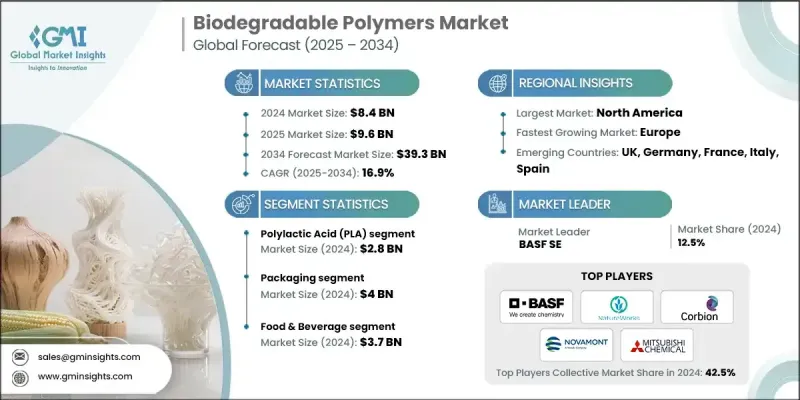

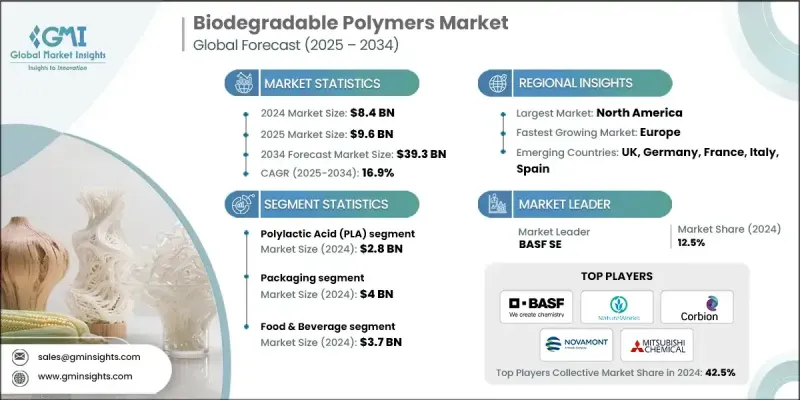

세계의 생분해성 폴리머 시장은 2024년 84억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 16.9%로 성장하여 393억 달러에 이를 것으로 예측됩니다.

생분해성 폴리머란 미생물, 열, 습기, 호기성 조건에 노출됨으로써 물, 이산화탄소, 바이오매스로 자연스럽게 분해되는 재료입니다. 환경에서 수세기에 걸쳐 남아있는 전통적인 플라스틱과는 달리, 이러한 중합체는 재생 가능 자원에서 유래하거나 합성으로 제조된 지속 가능한 대안을 제공합니다. 환경 의식 증가와 플라스틱 오염에 대한 규제 강화가 다양한 산업 분야에서의 채택을 촉진하고 있습니다. 세계 각국의 정부는 일회용 플라스틱의 사용 제한을 부과하고 기업이 환경 친화적인 선택으로 이행하도록 촉구하고 있습니다. 지속가능한 포장재, 농업용 필름, 일회용 제품에 대한 소비자 수요가 증가함에 따라 성장이 더욱 가속화되고 있습니다. 기술 발전으로 생분해성 폴리머의 성능, 가공성, 내구성이 향상되었습니다. 현재의 연구는 강도, 유연성 및 열 안정성을 향상시키면서 자연 분해성을 유지하기 위해 화학 구조를 최적화하는 데 중점을 둡니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034 |

| 시작 금액 | 84억 달러 |

| 예측 금액 | 393억 달러 |

| CAGR | 16.9% |

폴리유산(PLA)은 2024년 포장, 일회용 제품 및 의료용 응용 분야에 따라 28억 달러 시장 규모를 차지했습니다. 산업 규모의 퇴비화가 가능하고 기존 제조 설비와의 통합이 용이하기 때문에 지속 가능한 솔루션을 추구하는 기업으로부터 높은 지지를 얻고 있습니다. 폴리하이드록시알카노에이트(PHA)는 뛰어난 생분해성과 범용성으로 의료기기 및 특수 플라스틱 시장에서 주목을 받고 있습니다.

패키징 부문은 생분해성 폴리머의 응용 확대로 2024년 40억 달러 규모를 창출했습니다. 식품, 음료, 소매 부문의 기업들은 규제 요건과 소비자의 기대에 부응하기 위해 기존의 플라스틱을 PLA, 전분계 필름, 셀룰로오스 제품으로 대체하는 움직임을 가속화하고 있습니다. 이 부문은 대량 사용과 눈에 보이는 지속가능성의 장점을 결합하여 생분해성 폴리머 도입에서 가장 상업적으로 진행된 분야가 되었습니다.

미국의 생분해성 폴리머 시장은 2024년 21억 달러 규모에 달했습니다. 북미는 기업과 소비자가 환경 친화적인 솔루션을 우선하는 자세를 계속해, 계속 주도적인 입장을 유지하고 있습니다. 연방 및 주 수준의 정책과 플라스틱 오염에 대한 인식이 높아짐에 따라 포장, 농업 및 소비재 분야에서 생분해성 소재의 통합이 촉진됩니다. 폴리머 과학의 진보로 비용 효율성과 성능이 향상되고 환경 부하 저감을 목표로 하는 산업에 있어서 생분해성 폴리머는 매력적인 선택이 되고 있습니다. 이에 따라 북미는 지속 가능한 폴리머 솔루션의 혁신과 광범위한 채택에 있어서 핵심 지역으로서의 지위를 확립하고 있습니다.

세계의 생분해성 폴리머 시장의 주요 기업으로는 BASF SE, NatureWorks LLC, Novamont S.p.A., Corbion N.V., Mitsubishi Chemical Group, Kaneka Corporation, Biome Bioplastics Limited, FKuR Kunststoff GmbH, Braskem S.A., Kingfa Sci. & Tech.Co., Ltd., Bio On S.p.A., Plantic Technologies Limited, Genomatica Inc., Mango Materials Inc., Full Cycle Bioplastics Inc., RWDC Industries Pte Ltd., Bioplastics Feedstock Alliance, and CJ CheilJedang Corporation 등이 있습니다. 생분해성 폴리머 시장의 각 회사는 여러 전략적 접근을 통해 존재감을 강화하고 있습니다. 강도, 열안정성, 생분해성을 향상시킨 새로운 폴리머 배합의 개발을 향해, 연구 개발에 상당액의 투자를 실시했습니다. 포장, 소비재, 농업 관련 기업과의 전략적 제휴 및 협업을 통해 시장 범위를 확대하고 맞춤형 솔루션을 개발하고 있습니다. 기술력의 통합과 생산 규모의 확대를 목적으로 한 합병·인수도 추진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 생산기술의 진보

- 포장 업계 수요 증가

- 의료 및 농업 분야에서의 이용 증가

- 환경에 배려한 제품에 대한 소비자의 기호

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용

- 성능상의 제약

- 시장 기회

- 의료·농업 분야에 있어서의 확대

- 기술 혁신

- 순환형 경제 모델의 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 폴리머유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 폴리머 유형별, 2021-2034

- 주요 동향

- 폴리유산(PLA)

- 폴리하이드록시알카노에이트(PHA)

- 폴리부틸렌 석시네이트(PBS)

- 폴리카프로락톤(PCL)

- 전분기반 폴리머

- 셀룰로오스 유도체

- 신규 유형

제6장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 포장

- 농업 분야

- 의료 및 헬스케어

- 섬유·섬유 제품

- 소비재

- 기타 용도

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 식음료

- 농업·원예

- 의료 및 헬스케어

- 자동차

- 전자제품 및 소비재

- 섬유 및 의류

제8장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- BASF SE

- NatureWorks LLC

- Novamont SpA

- Corbion NV

- Mitsubishi Chemical Group

- Kaneka Corporation

- Biome Bioplastics Limited

- FKuR Kunststoff GmbH

- Braskem SA

- Kingfa Sci. &Tech.Co.,Ltd.

- Bio On SpA

- Plantic Technologies Limited

- Genomatica Inc.

- Mango Materials Inc.

- Full Cycle Bioplastics Inc.

- RWDC Industries Pte Ltd.

- Bioplastics Feedstock Alliance

- CJ CheilJedang Corporation

The Global Biodegradable Polymers Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 16.9% to reach USD 39.3 billion by 2034.

Biodegradable polymers are materials capable of breaking down naturally through exposure to microorganisms, heat, moisture, and aerobic conditions into water, carbon dioxide, and biomass. Unlike conventional plastics that persist in the environment for centuries, these polymers offer sustainable alternatives derived from renewable sources or produced synthetically. Growing environmental awareness and stricter regulations on plastic pollution are driving their adoption across industries. Governments worldwide are imposing restrictions on single-use plastics, encouraging companies to switch to eco-friendly options. Rising consumer demand for sustainable packaging, agricultural films, and disposable products further accelerates growth. Technological advancements are enhancing the performance, processability, and durability of biodegradable polymers. Current research focuses on optimizing chemical structures to improve strength, flexibility, and thermal stability while ensuring they remain naturally degradable.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $39.3 Billion |

| CAGR | 16.9% |

The polylactic Acid (PLA) accounted for USD 2.8 billion in 2024, driven by its application in packaging, disposable products, and biomedical uses. Its ability to compost industrially and integrate with existing manufacturing setups makes it highly favored by companies pursuing sustainable solutions. Polyhydroxyalkanoates (PHAs) are gaining traction in medical devices and specialty plastics markets due to their excellent biodegradability and versatility.

The packaging segment generated USD 4 billion in 2024, driven by the growing application of biodegradable polymers. Companies in the food, beverage, and retail sectors are increasingly replacing conventional plastics with PLA, starch-based films, and cellulose products to meet regulatory requirements and consumer expectations. This segment combines high-volume usage with visible sustainability benefits, making it the most commercially advanced area for biodegradable polymer adoption.

U.S. Biodegradable Polymers Market generated USD 2.1 billion in 2024. North America continues to lead as companies and consumers prioritize eco-friendly solutions. Federal and state policies, along with growing awareness of plastic pollution, have encouraged the integration of biodegradable materials in packaging, agriculture, and consumer products. Advances in polymer science have enhanced cost-efficiency and performance, making biodegradable polymers an attractive option for industries aiming to lower their environmental impact. This positions North America as a hub for innovation and widespread adoption of sustainable polymer solutions.

Key players operating in the Global Biodegradable Polymers Market include BASF SE, NatureWorks LLC, Novamont S.p.A., Corbion N.V., Mitsubishi Chemical Group, Kaneka Corporation, Biome Bioplastics Limited, FKuR Kunststoff GmbH, Braskem S.A., Kingfa Sci. & Tech. Co., Ltd., Bio On S.p.A., Plantic Technologies Limited, Genomatica Inc., Mango Materials Inc., Full Cycle Bioplastics Inc., RWDC Industries Pte Ltd., Bioplastics Feedstock Alliance, and CJ CheilJedang Corporation. Companies in the Biodegradable Polymers Market are strengthening their presence through multiple strategic approaches. They are investing heavily in research and development to innovate new polymer formulations with improved strength, thermal stability, and biodegradability. Strategic partnerships and collaborations with packaging, consumer goods, and agricultural firms allow them to expand market reach and develop tailored solutions. Mergers and acquisitions are being pursued to consolidate technological capabilities and scale production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in production technology

- 3.2.1.2 Rising demand in packaging industry

- 3.2.1.3 Increasing use in medical and agricultural applications

- 3.2.1.4 Consumer preference for eco-friendly products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Performance limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in medical and agriculture sectors

- 3.2.3.2 Technological innovations

- 3.2.3.3 Development of circular economy models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By polymer type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polylactic acid (PLA)

- 5.3 Polyhydroxyalkanoates (PHA)

- 5.4 Polybutylene succinate (PBS)

- 5.5 Polycaprolactone (PCL)

- 5.6 Starch-based polymers

- 5.7 Cellulose derivatives

- 5.8 Emerging types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Packaging

- 6.3 Agricultural

- 6.4 Medical & healthcare

- 6.5 Textile & fiber

- 6.6 Consumer goods

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Agriculture & horticulture

- 7.4 Healthcare & medical

- 7.5 Automotive

- 7.6 Electronics & consumer

- 7.7 Textile & apparel

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 NatureWorks LLC

- 9.3 Novamont S.p.A

- 9.4 Corbion N.V.

- 9.5 Mitsubishi Chemical Group

- 9.6 Kaneka Corporation

- 9.7 Biome Bioplastics Limited

- 9.8 FKuR Kunststoff GmbH

- 9.9 Braskem S.A.

- 9.10 Kingfa Sci. & Tech.Co.,Ltd.

- 9.11 Bio On S.p.A.

- 9.12 Plantic Technologies Limited

- 9.13 Genomatica Inc.

- 9.14 Mango Materials Inc.

- 9.15 Full Cycle Bioplastics Inc.

- 9.16 RWDC Industries Pte Ltd.

- 9.17 Bioplastics Feedstock Alliance

- 9.18 CJ CheilJedang Corporation