|

시장보고서

상품코드

1871317

고셰병 치료제 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Gaucher Disease Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

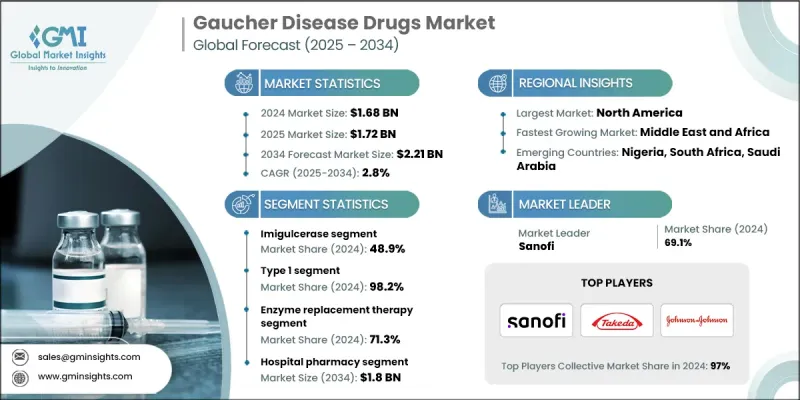

고셰병 치료제 시장은 2024년에 16억 8,000만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 2.8%로 성장하여 22억 1,000만 달러에 이를 것으로 예측됩니다.

희귀 유전성 질환에 대한 인식이 높아지고 진단 기술이 향상되고 효소 보충 요법과 기질 감소 요법에 대한 접근이 확대됨에 따라 시장이 꾸준히 확대되고 있습니다. 글루코세레브로시다아제 결핍으로 인한 리소좀 축적증인 고셰병은 지난 10년간 치료면에서 큰 진전을 이루고 있습니다. 표적 치료는 근본적인 효소 결핍에 대처하고, 삶의 질을 향상시키고, 질병 증상을 관리함으로써 환자 케어의 본질을 바꾸고 있습니다. 다케다약품공업주식회사, 존슨엔드 존슨, 사노피 등 주요 제약기업은 지속적인 연구개발, 전략적 제휴, 희소질환에 특화된 플랫폼을 통해 혁신을 추진하고 있습니다. 지역 차이가 치료의 초점을 좌우하고 있으며, 아시아태평양에서는 특정 하위유형을 더 많이 볼 수 있는 반면, 북미와 유럽에서는 유형 1사례가 주류가 되고 있습니다. 이는 지역별 치료법의 제공과 효소 보충 요법(ERT) 및 기질 감소 요법(SRT)에 대한 접근의 중요성을 강조합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034 |

| 시작 금액 | 16억 8,000만 달러 |

| 예측 금액 | 22억 1,000만 달러 |

| CAGR | 2.8% |

이미글루셀라제 부문은 2024년에 48.9%의 점유율을 차지했습니다. 이 재조합 효소 보충 요법은 글루코셀레브로시다아제 결핍을 보충하고 축적된 글루코셀레브로시드의 분해를 돕고 질병 증상을 완화시킵니다. 광범위한 채용은 강력한 임상적 효능, 입증된 장기적인 안전성 및 광범위한 규제 당국의 승인에 의해 지원되며, 건강 관리 제공업체와 환자 간에 신뢰할 수 있는 치료로서의 지위를 확립하고 있습니다.

2024년, 제1형 고쉐병(GD1) 부문은 98.2%의 점유율을 차지했습니다. 가장 흔한 아형인 GD1은 신경학적 관여를 수반하지 않는 전신 증상을 특징으로 하며 기존 치료에 대한 반응성이 높고 세계적인 의약품 개발·상업화의 중심적인 초점이 되고 있습니다.

미국 고셰병 치료제 시장은 2024년 6억 4,570만 달러로 평가되었습니다. 이 나라의 첨단 의료 인프라, 임상 현장에서의 광범위한 채용, 맞춤형 의료에 대한 중점적 노력은 고셰병의 조기 진단과 장기 관리를 지원합니다. 이미글루세라제나 베라글루세라제 알파 등의 효소 보충 요법에 더해, 엘리글루스타트 등의 경구 기질 감소 요법의 사용 증가가 이 지역의 치료 실천을 주도하고 있습니다.

세계 고셰병 치료제 시장의 주요 기업으로는 ANI Pharmaceuticals, Inc., Pfizer Inc., Takeda Pharmaceutical Company Limited, Johnson & Johnson, Protalix BioTherapeutics, Inc., Navinta, LLC, Dipharma SA, Prevail Therapeutics, ISU ABXIS, Generium, and Sanofi 등이 있습니다. 고셰병 치료제 시장의 기업은 차세대 치료법과 희귀질환 플랫폼의 연구개발(R&D)에 많은 투자를 하고 존재감을 강화하고 있습니다. 세계 액세스 확대 및 규제 당국의 승인 취득을 목표로 전략적 파트너십 및 협업을 추진하고 있습니다. 시장 리더 기업은 다른 하위 유형과 지역에 맞는 개인화 치료를 포함한 환자 중심 접근법에 주력하고 있습니다. 또한 헬스케어 종사자와 환자 커뮤니티를 위한 교육 프로그램을 통해 인지도 향상을 도모하고 있습니다. 지속적인 혁신, 타겟 마케팅 전략, 신흥 시장 진출은 기업이 경쟁 우위를 유지하는 데 도움이 됩니다. 한편, 규제 준수와 지적 재산 보호는 시장에서의 발판을 더욱 굳히는 것으로 이어지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 고셰병의 유병률 증가

- 고셰병 치료법 개발에 대한 투자 확대

- 적시의 진단과 치료에 대한 의식의 고조

- 희소질환 치료에 대한 정부 지원 확대

- 업계의 잠재적 위험 및 과제

- 치료법의 고비용

- 엄격한 규제 승인 절차의 존재

- 시장 기회

- 신흥 시장으로의 확대와 현지생산

- 기질 감소 요법의 도입 상황

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 현재의 기술 동향

- 임상 바이오마커 개선

- 유전자 치료 접근

- AI를 활용한 창약 플랫폼

- 신규기술

- 맞춤형 치료를 위한 멀티오믹스 통합

- 약물 설계 최적화를 위한 양자 컴퓨팅

- 현재의 기술 동향

- 특허 분석

- 장래 시장 동향

- 파이프라인 분석

- 가격 분석, 2024

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 약제 유형별, 2021-2034

- 주요 동향

- Imiglucerase

- Velaglucerase alfa

- Taliglucerase alfa

- Eliglustat

- Miglustat

제6장 시장 추정 및 예측 : 질환 유형별, 2021-2034

- 주요 동향

- 유형 1

- 유형 3

제7장 시장추정 및 예측 : 치료법별, 2021-2034

- 주요 동향

- 효소 대체 요법

- 기질 치환 요법

제8장 시장추정 및 예측 : 유통채널별, 2021-2034

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

- 콜롬비아

- 페루

- 에콰도르

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 나이지리아

- 이스라엘

- 이란

제10장 기업 프로파일

- ANI Pharmaceuticals, Inc.

- Dipharma SA

- Generium

- ISU ABXIS

- Johnson & Johnson

- Navinta, LLC

- Pfizer Inc.

- Prevail Therapeutics

- Protalix BioTherapeutics, Inc.

- Sanofi

- Takeda Pharmaceutical Company Limited

The Gaucher Disease Drugs Market was valued at USD 1.68 billion in 2024 and is estimated to grow at a CAGR of 2.8% to reach USD 2.21 billion by 2034.

The market is steadily expanding as awareness of rare genetic disorders rises, diagnostic techniques improve, and access to enzyme replacement and substrate reduction therapies broadens. Gaucher disease, a lysosomal storage disorder caused by glucocerebrosidase deficiency, has seen significant therapeutic breakthroughs over the past decade. Targeted treatments are reshaping patient care by addressing the underlying enzyme deficiency, improving quality of life, and managing disease symptoms. Leading pharmaceutical companies such as Takeda Pharmaceutical Company Limited, Johnson & Johnson, and Sanofi are driving innovation through continuous research and development, strategic collaborations, and rare disease-focused platforms. Regional variations influence treatment focus, with certain subtypes more prevalent in Asia Pacific, while North America and Europe are dominated by Type 1 cases, highlighting the importance of region-specific therapy availability and access to both enzyme replacement therapies (ERTs) and substrate reduction therapies (SRTs).

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.68 Billion |

| Forecast Value | $2.21 Billion |

| CAGR | 2.8% |

The Imiglucerase segment held a share of 48.9% in 2024. This recombinant enzyme replacement therapy compensates for glucocerebrosidase deficiency, aiding the breakdown of accumulated glucocerebroside and alleviating disease manifestations. Its widespread adoption is supported by strong clinical efficacy, proven long-term safety, and broad regulatory approval, establishing it as a trusted treatment among healthcare providers and patients.

Type 1 Gaucher disease (GD1) segment held a 98.2% share in 2024. GD1, the most common subtype, is characterized by systemic symptoms without neurological involvement, making it more responsive to existing therapies and a central focus for drug development and commercialization efforts globally.

U.S. Gaucher Disease Drugs Market was valued at USD 645.7 million in 2024. The country's advanced healthcare infrastructure, widespread clinical adoption, and emphasis on personalized medicine support early diagnosis and long-term management of Gaucher disease. Enzyme replacement therapies like imiglucerase and velaglucerase alfa, along with increasing use of oral substrate reduction therapies such as eliglustat, dominate treatment practices in the region.

Key players in the Global Gaucher Disease Drugs Market include ANI Pharmaceuticals, Inc., Pfizer Inc., Takeda Pharmaceutical Company Limited, Johnson & Johnson, Protalix BioTherapeutics, Inc., Navinta, LLC, Dipharma SA, Prevail Therapeutics, ISU ABXIS, Generium, and Sanofi. Companies in the Gaucher Disease Drugs Market are strengthening their presence by investing heavily in R&D for next-generation therapies and rare disease platforms. They pursue strategic partnerships and collaborations to expand global access and regulatory approvals. Market leaders focus on patient-centric approaches, including tailored therapies for different subtypes and regions. They also enhance visibility through education programs for healthcare providers and patient communities. Continuous innovation, targeted marketing strategies, and expansion into emerging markets help companies maintain a competitive edge, while regulatory compliance and intellectual property protections further consolidate their market foothold.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug type trends

- 2.2.3 Disease type trends

- 2.2.4 Therapy type trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of Gaucher disease

- 3.2.1.2 Growing investments for developing Gaucher disease therapies

- 3.2.1.3 Increasing awareness towards timely diagnosis and treatment

- 3.2.1.4 Rising government support for rare disease therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of therapies

- 3.2.2.2 Presence of stringent regulatory approval procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market expansion and local manufacturing

- 3.2.3.2 Substrate reduction therapy adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Improved clinical biomarkers

- 3.5.1.2 Gene therapy approaches

- 3.5.1.3 AI- guided drug discovery platforms

- 3.5.2 Emerging technologies

- 3.5.2.1 Multi-omics integration for personalized therapy

- 3.5.2.2 Quantum computing for drug design optimization

- 3.5.1 Current technological trends

- 3.6 Patent analysis

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Pricing analysis, 2024

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Imiglucerase

- 5.3 Velaglucerase alfa

- 5.4 Taliglucerase alfa

- 5.5 Eliglustat

- 5.6 Miglustat

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 1

- 6.3 Type 3

Chapter 7 Market Estimates and Forecast, By Therapy Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Enzyme replacement therapy

- 7.3 Substrate replacement therapy

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Retail pharmacy

- 8.4 Online pharmacy

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.5.5 Colombia

- 9.5.6 Peru

- 9.5.7 Ecuador

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Egypt

- 9.6.5 Nigeria

- 9.6.6 Israel

- 9.6.7 Iran

Chapter 10 Company Profiles

- 10.1 ANI Pharmaceuticals, Inc.

- 10.2 Dipharma SA

- 10.3 Generium

- 10.4 ISU ABXIS

- 10.5 Johnson & Johnson

- 10.6 Navinta, LLC

- 10.7 Pfizer Inc.

- 10.8 Prevail Therapeutics

- 10.9 Protalix BioTherapeutics, Inc.

- 10.10 Sanofi

- 10.11 Takeda Pharmaceutical Company Limited