|

시장보고서

상품코드

1876545

식물성 유제품 대체품 시장 : 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Plant-Based Dairy Alternatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

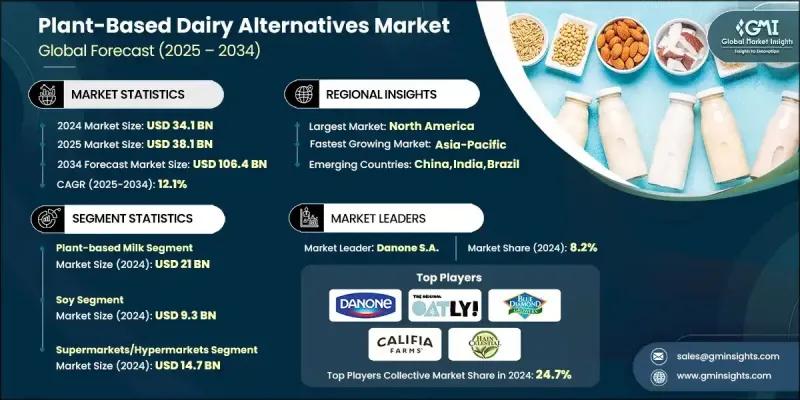

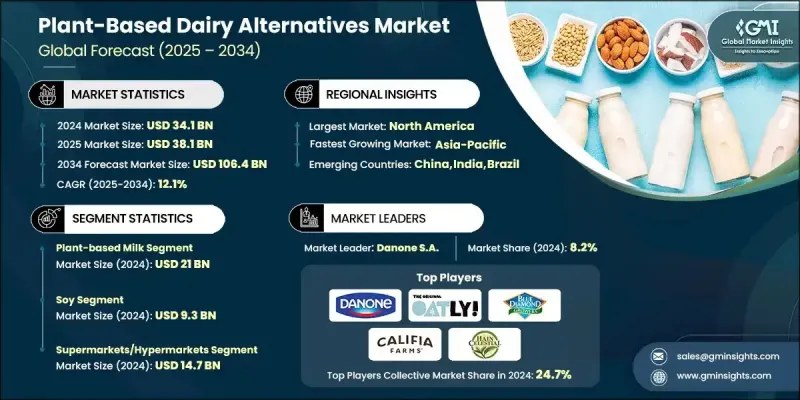

세계의 식물성 유제품 대체품 시장은 2024년에 341억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 12.1%로 성장하고 1,064억 달러에 이를 것으로 예측됩니다.

소비자가 기존의 유제품을 대체하는 지속가능하고 영양가가 높고 윤리적인 대체품을 점점 더 추구하는 가운데, 시장은 빠르게 성장하고 있습니다. 유당 프리나 비건용 제품 수요 증가와 원료 기술의 진보가 함께 업계를 견인하고 있습니다. 식물성 치즈와 요구르트는 현재 시장에서의 비율은 작지만 유제품의 식감, 풍미, 기능성을 재현하는 혁신적인 배합 기술에 힘입어 두 자리수의 견고한 성장률을 나타내고 있습니다. 이 분야에는 많은 자본 투자가 유입되고 있으며 기존 유제품 제조업체는 귀리, 완두콩, 아몬드 등의 원료를 가공하기 위해 시설의 근대화를 진행하고 있습니다. 식물성 단백질의 소비를 촉진하는 정책 변경이나 식물성 음료를 도입한 학교급식 프로그램도 수요를 더욱 자극하고 있습니다. 향후 규제의 명확화, 균형 잡힌 가격 설정, 탄소 배출량에 대한 설명 책임 등의 요소가 업계의 궤도를 형성하고 이들이 함께 북미 및 유럽의 주요 시장에서의 제품 혁신과 원재료 조달에 영향을 줄 전망입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 341억 달러 |

| 예측 금액 | 1,064억 달러 |

| CAGR | 12.1% |

식물성 우유 시장은 2024년에 210억 달러 규모에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 12.1%로 성장할 것으로 예측됩니다. 현재, 이 시장에서는 귀리 기반의 음료가 주류를 차지하고 있으며, 그 부드러운 맛, 범용성 및 우수한 지속가능성이 평가되고 있습니다. 소비자가 대두나 아몬드 이외의 대체품을 탐구하는 가운데, 햄프, 코코넛, 소라마메 등의 원료가 신제품 라인에 짜넣어져, 구색과 영양가의 확충이 진행되고 있습니다. 각 브랜드는 유제품과 동등하거나 그 이상의 맛, 입맛, 영양 밀도를 실현하기 위한 연구 개발에 지속적으로 투자하고 있습니다. 이 부문의 진화는 식물성 유제품 산업 전반에 걸친 혁신을 촉진하고 소비자의 수용성과 제품 다양성을 모두 향상시킵니다.

슈퍼마켓 및 하이퍼마켓 부문은 2024년 147억 달러 규모에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 11.1%로 성장하고 43.2%의 점유율을 차지할 것으로 예측됩니다. 이 소매점은 광대한 선반 공간과 높은 가시성으로 유통을 지배하고 있으며 식물성 제품이 일반 소비자층에 도달할 수 있도록 지원합니다. 한편, 전문 소매점과 건강 식품 소매점은 신제품 형식의 테스트와 런치에서 중요한 역할을 계속하고 있습니다. 식물성 유제품이 점점 일반화되고 있는 가운데, 개인 브랜드가 확대되어 경쟁력 있는 가격의 대체품을 제공합니다. 편의점도 일상적인 쇼핑 환경에서 손쉽게 구입할 수 있는 식물성 제품 수요 증가에 대응하여 구색을 확충하고 있습니다.

독일의 식물성 유제품 대체품 시장은 2024년 19억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 11.7%로 성장할 것으로 예측됩니다. 이 나라는 높은 환경 의식, 아몬드 및 귀리 기반 유제품 대체품의 보급, 지속 가능하고 현지 제품에 대한 소비자 선호 증가로 유럽을 선도하고 있습니다. 국내 브랜드와 슈퍼마켓 체인 간의 치열한 경쟁은 개인 브랜드 개발을 촉진하고 소비자의 시도 범위를 확대하고 시장의 성장을 가속화하고 있습니다.

세계의 식물성 유제품 대체품 시장에서 사업을 전개하는 주요 기업으로는 Hain Celestial Group, Blue Diamond Growers, Oatly Group AB, Califia Farms, Danone SA 등이 있습니다. 식물성 유제품 대체품 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 혁신, 사업 확대 및 협업을 추진하고 있습니다. 첨단 가공 기술과 원료 최적화를 통해 유제품의 식감과 영양 프로파일을 재현하기 위해 제품 연구에 많은 투자를 하고 있습니다. 소매업체와 외식 체인과의 전략적 제휴를 통해 제품 인지도와 가용성 향상을 도모하고 있습니다. 또한 세계적인 수요 증가에 대응하기 위해 생산 능력 확대와 신규 지역 시장 진출을 진행하고 있습니다. 귀리, 대마, 소라 콩과 같은 대체 단백질 소스로의 다각화는 공급망의 탄력성과 지속가능성 목표 달성을 지원합니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사·검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규 기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2025년-2034년

- 주요 동향

- 식물성 우유

- 상온 보존 가능

- 콜드 스토리지

- 식물성 요구르트

- 스푼형

- 음용형

- 식물성 치즈

- 블록 및 휠

- 슈레드 및 강판

- 슬라이스

- 크림치즈 및 스프레드

- 외식산업용 대체품

- 식물성 아이스크림 및 냉동 디저트

- 파인트·튜브

- 참신 상품

- 식물성 버터 스프레드

- 스틱/블록

- 소프트 튜브 스프레드

- 크리머

- 냉장액

- 상온 보존 가능한 액체 제품

- 분말

- 기타

제6장 시장 추정 및 예측 : 소스별, 2025년-2034년

- 주요 동향

- 콩

- 아몬드

- 귀리

- 코코넛

- 햄프(대마씨)

- 혼합/블렌드 베이스

- 신규 단백질

- 율무콩

- 아마씨

- 퀴노아

- 기타 단백질

제7장 시장 추정 및 예측 : 유통 채널별, 2025년-2034년

- 주요 동향

- 슈퍼마켓 및 하이퍼마켓

- 편의점·식료품점

- 전문점 및 건강식품점

- 온라인 소매/DTC

- 외식산업

- 공업용/B2B용 원료

제8장 시장 추정 및 예측 : 지역별, 2025년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Blue Diamond Growers

- Califia Farms

- Danone SA

- Earth's Own Food Company Inc.

- Eden Foods, Inc.

- Elmhurst 1925

- Good Karma Foods

- Happy Planet Foods

- Hain Celestial Group

- Nestle SA

- Oatly Group AB

- Pacific Foods of Oregon, LLC

- Ripple Foods

- SunOpta Inc.

- The Coca-Cola Company(Fairlife/Simply platforms)

- The Hain Celestial Group

- The Hershey Company(via SOFIT)

- TurtleTree

- Valio Ltd

- Yili Group

The Global Plant-Based Dairy Alternatives Market was valued at USD 34.1 billion in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 106.4 billion by 2034.

The market is experiencing rapid growth as consumers increasingly seek sustainable, nutritious, and ethical alternatives to traditional dairy products. Rising demand for lactose-free and vegan options, combined with advancements in ingredient technology, is propelling the industry forward. Although plant-based cheese and yogurt currently represent smaller portions of the market, they are growing at strong double-digit rates, supported by innovative formulations that replicate the texture, flavor, and functionality of dairy. Significant capital investments are flowing into the sector, with established dairy producers modernizing their facilities to process ingredients such as oats, peas, and almonds. Policy changes encouraging plant protein consumption and school nutrition programs that incorporate plant-based beverages are further stimulating demand. Looking ahead, the industry's trajectory will be shaped by factors such as regulatory clarity, balanced pricing, and accountability for carbon emissions, which together will influence product innovation and raw material sourcing in key markets across North America and Europe.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.1 Billion |

| Forecast Value | $106.4 Billion |

| CAGR | 12.1% |

The plant-based milk segment generated USD 21 billion in 2024 and is anticipated to grow at a CAGR of 12.1% between 2025 and 2034. Oat-based beverages currently dominate this segment, appreciated for their mild taste, versatility, and favorable sustainability profile. As consumers explore alternatives beyond soy and almond, ingredients like hemp, coconut, and fava beans are being incorporated into new product lines to expand variety and nutritional value. Brands continue to invest in research and development aimed at improving taste, mouthfeel, and nutrient density to match or surpass dairy equivalents. The evolution of this segment is driving innovation across the wider plant-based dairy industry, enhancing both consumer acceptance and product diversity.

The supermarkets and hypermarkets segment was valued at USD 14.7 billion in 2024 and is expected to grow at a CAGR of 11.1% from 2025 to 2034, representing 43.2% share. These retail outlets dominate distribution due to extensive shelf space and visibility, helping plant-based products reach mainstream consumers. At the same time, specialty and health-food retailers continue to play a crucial role in testing and launching new product formats. As plant-based dairy becomes increasingly normalized, private-label brands are expanding, offering competitively priced alternatives. Convenience stores are also broadening their offerings to meet the growing consumer preference for accessible plant-based options in everyday shopping environments.

Germany Plant-Based Dairy Alternatives Market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 11.7% through 2034. The country leads in Europe due to strong environmental awareness, widespread adoption of almond and oat-based dairy substitutes, and growing consumer preference for sustainable and locally sourced products. Intense competition among domestic brands and supermarket chains has spurred private-label development and broadened consumer trials, further accelerating market expansion.

Key players operating in the Global Plant-Based Dairy Alternatives Market include Hain Celestial Group, Blue Diamond Growers, Oatly Group AB, Califia Farms, and Danone S.A. Leading companies in the plant-based dairy alternatives market are pursuing innovation, expansion, and collaboration to strengthen their market foothold. They are investing heavily in product research to replicate the texture and nutritional profile of dairy through advanced processing and ingredient optimization. Strategic partnerships with retailers and foodservice chains are helping enhance product visibility and accessibility. Companies are also expanding production capacity and entering new regional markets to meet rising global demand. Diversification into alternative protein sources such as oats, hemp, and fava beans supports supply chain resilience and sustainability goals.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Source

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2025 - 2034 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based milk

- 5.2.1 Shelf-stable

- 5.2.2 Refrigerated

- 5.3 Plant-based yogurt

- 5.3.1 Spoonable

- 5.3.2 Drinkable

- 5.4 Plant-based cheese

- 5.4.1 Block & wheel

- 5.4.2 Shredded & grated

- 5.4.3 Sliced

- 5.4.4 Cream-cheese & spreads

- 5.4.5 Food-service analogues

- 5.5 Plant-based ice cream & frozen dessert

- 5.5.1 Pints & tubs

- 5.5.2 Novelties

- 5.6 Plant-based butter & spreads

- 5.6.1 Stick / block

- 5.6.2 Soft-tub spreads

- 5.7 Creamers

- 5.7.1 Refrigerated liquid

- 5.7.2 Shelf-stable liquid

- 5.7.3 Powdered

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Source, 2025 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Soy

- 6.3 Almond

- 6.4 Oat

- 6.5 Coconut

- 6.6 Hemp

- 6.7 Mixed / blended bases

- 6.8 Novel proteins

- 6.8.1 Faba bean

- 6.8.2 Flaxseed

- 6.8.3 Quinoa

- 6.8.4 Other proteins

Chapter 7 Market Estimates and Forecast, By Distribution channel, 2025 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets & hypermarkets

- 7.3 Convenience & grocery stores

- 7.4 Specialty & health-food stores

- 7.5 Online retail / DTC

- 7.6 Food-service

- 7.7 Industrial / B2B ingredients

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Blue Diamond Growers

- 9.2 Califia Farms

- 9.3 Danone S.A.

- 9.4 Earth’s Own Food Company Inc.

- 9.5 Eden Foods, Inc.

- 9.6 Elmhurst 1925

- 9.7 Good Karma Foods

- 9.8 Happy Planet Foods

- 9.9 Hain Celestial Group

- 9.10 Nestle S.A.

- 9.11 Oatly Group AB

- 9.12 Pacific Foods of Oregon, LLC

- 9.13 Ripple Foods

- 9.14 SunOpta Inc.

- 9.15 The Coca-Cola Company (Fairlife/Simply platforms)

- 9.16 The Hain Celestial Group

- 9.17 The Hershey Company (via SOFIT)

- 9.18 TurtleTree

- 9.19 Valio Ltd

- 9.20 Yili Group