|

시장보고서

상품코드

1876569

하이브리드 수소-전기 파워트레인 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Hybrid Hydrogen-Electric Powertrain Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

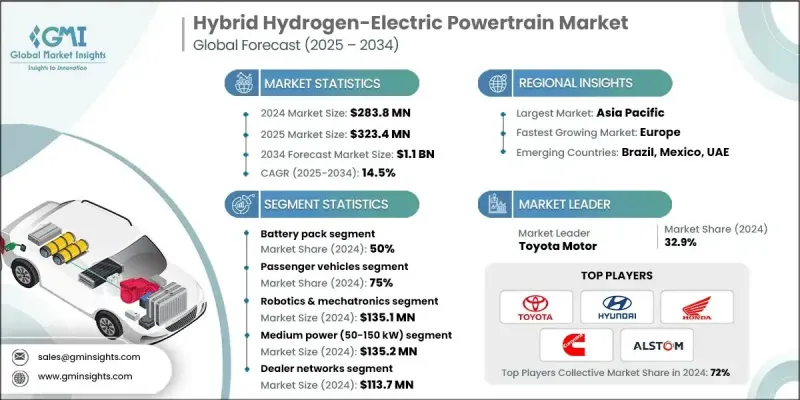

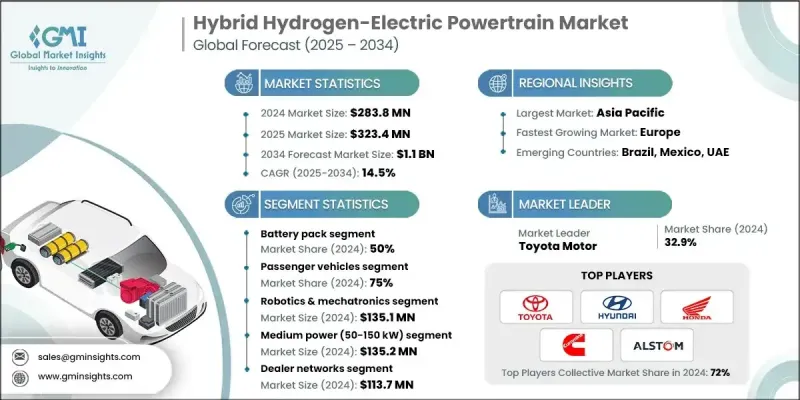

하이브리드 수소-전기 파워트레인 시장은 2024년에 2억 8,380만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 14.5%를 나타내 11억 달러에 이를 것으로 예측됩니다.

시장의 급속한 성장은 지속가능하고 에너지 효율적인 이동성에 대한 세계 관심 증가와 저배출형 운송 시스템으로의 전환에 의해 추진되고 있습니다. 승용차, 상용차, 특수 차량에서 하이브리드 수소-전기 파워트레인의 채용 확대는 엄격한 정부 정책, 연비 목표 향상, 보다 깨끗한 이동성 선택에 대한 수요에 의해 영향을 받고 있습니다. 경량 재료, 에너지 저장 시스템, 첨단 파워트레인 구조의 지속적인 발전은 기술 혁신을 더욱 촉진하고 있습니다. 스마트 제조와 디지털 자동화의 통합 확대는 제조업체에 의한 시스템 설계·생산 수법을 변화시키고 있습니다. IoT를 활용한 감시, AI에 의한 프로세스 관리, 예지 보전을 통해 자동차 제조업체는 효율성 향상, 생산 정지 시간 절감, 품질 기준 개선을 실현하고 있습니다. 첨단 연료전지 기술, 고효율 전기 모터, 지능형 에너지 관리 플랫폼은 하이브리드 수소-전기 시스템의 전반적인 성능을 향상시킵니다. 디지털 공장 에코시스템, 클라우드 기반 운영, 상호 운용가능한 자동화 플랫폼의 도입은 시장을 세계 탈탄소화 및 넷 제로 배출 이니셔티브와 매치시킵니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 2억 8,380만 달러 |

| 예측 금액 | 11억 달러 |

| CAGR | 14.5% |

2024년 배터리 팩 부문은 50%의 점유율을 차지했으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 14.5%를 나타낼 것으로 예측됩니다. 배터리 팩은 효율적인 에너지 저장 및 분배의 주요 원천으로서 하이브리드 수소-전기 파워트레인에 여전히 필수적입니다. 고체 전지 및 고밀도 리튬 이온 시스템과 같은 선진 전지 기술의 활용 확대는 재생에너지 회수, 항속 거리 연장, 수소 연료전지 및 전기 추진 시스템과의 원활한 연계를 지원합니다. 자동차 제조업체와 공급업체는 지속적인 신뢰성, 높은 에너지 효율 및 하이브리드 성능 향상을 보장하기 위해 고성능 배터리 팩의 우선순위를 지속적으로 강화하고 있습니다.

승용차 부문은 75%의 점유율을 차지했으며 2034년까지 연평균 복합 성장률(CAGR) 14.4%를 나타낼 것으로 예측됩니다. 이 부문의 이점은 하이브리드 자동차 및 수소-전기 승용차의 생산 확대, 배출 가스 규제 강화, 스마트 제조 기술의 보급에 의해 지원됩니다. 자동차 제조업체는 생산 정밀도, 에너지 효율, 환경 규제에 대한 적합성을 높이기 위해 로봇 공학, AI 기반 분석, 클라우드 연결 모니터링 시스템 등의 지능형 공장 솔루션에 많은 투자를 하고 있습니다.

일본의 하이브리드 수소-전기 파워트레인 시장은 2024년에 6,960만 달러의 규모가 되어, 33%의 점유율을 차지했습니다. 이 나라의 견고한 제조거점 외에도 OEM, Tier 1, Tier 2 공급업체 및 기술 개발 기업의 광범위한 수요가 시장의 꾸준한 확대를 지원하고 있습니다. 일본 기업은 예측 분석, IoT 기반 모니터링 시스템, 에너지 관리 플랫폼 등 첨단 디지털 솔루션을 파워트레인의 밸류체인 전체에 도입하고 있습니다. 모듈식으로 확장 가능한 파워트레인 시스템에 중점을 두면 제조업체는 운영 효율성, 신뢰성 및 지속가능성 성능을 향상시키면서 엄격한 환경 요구 사항을 충족할 수 있습니다.

세계의 하이브리드 수소-전기 파워트레인 시장에 참가하고 있는 유명 기업으로는 Alstom SA, Ballard Power Systems, BMW Group, Cummins, Honda Motor, Hyundai Motor, Kawasaki Heavy, PowerCell Sweden AB, Symbio, Toyota Motor 등이 있습니다. 세계 하이브리드 수소-전기 파워트레인 시장의 주요 제조업체는 혁신, 협업 및 확장을 결합하여 경쟁력을 강화하고 있습니다. 많은 기업들이 시스템 효율성, 수소 연료전지 성능 및 배터리 통합을 강화하기 위한 R&D에 투자하고 있습니다. 자동차 제조업체, 부품 공급업체 및 에너지 기업 간의 전략적 파트너십으로 기술 상업화와 대규모 배포가 가속화되고 있습니다. 각 회사는 디지털 변환에 중점을 두고 AI 기반 에너지 최적화를 통합하고 확장성과 유연성을 향상시키는 모듈식 설계를 채택합니다. 또한 현지 생산시설에 장기적인 투자와 지속가능성에 중점을 둔 이니셔티브를 통해 주요 기업은 비용면에서 우위를 실현하고 세계 배출감소 목표에 부합하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 정부의 탈탄소화 정책 및 수소 전략

- 기술의 성숙도와 상업적 실현 가능성의 검증

- 배터리 전용 솔루션에 대한 중부하 용도에 있어서 우위성

- 인프라 투자와 관민 연계

- 업계의 잠재적 위험 및 과제

- 고비용의 시스템과 부품 가격의 프리미엄

- 수소 충전 인프라의 부족

- 시장 기회

- 철도전화에 있어서 갭과 디젤 대체의 가능성

- 선박의 탈탄소화 요건

- 산업용 및 고정식 전원 용도

- 철도 및 선박의 탈탄소화

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 세계의 수소 연료전지 정책

- 배출규제와 탈탄소화규제

- 안전성 및 차량 기준

- 인프라 및 급유 컴플라이언스

- 연구개발 및 이노베이션 촉진책

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 연료전지 기술

- 배터리 및 에너지 저장

- 파워 일렉트로닉스 및 제어 유닛

- 전기 모터 및 구동계

- 디지털 및 스마트 제조의 통합

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 코스트 내역 분석

- 특허 분석

- 지속가능성 및 환경적 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 최상의 시나리오

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신제품 발매

- 사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 배터리 팩

- 연료전지 스택

- 전기 모터 및 구동계

- 파워 일렉트로닉스 및 제어 장치

- 수소 저장 시스템

- 플랜트 균형 장치(BoP)

제6장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제7장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 양성자 교환막(PEM) 연료전지 시스템

- 고체산화물 연료전지(SOFC) 시스템

- 인산형 연료전지(PAFC) 시스템

- 용융 탄산염 연료전지(MCFC) 시스템

- 알칼리 연료전지(AFC) 시스템

제8장 시장 추계·예측 : 출력별(2021-2034년)

- 주요 동향

- 중출력(50-150kW)

- 고출력(150-300kW)

- 저출력(50kW 미만)

- 초고출력(300kW 초과)

제9장 시장 추계·예측 : 하이브리드 구성별(2021-2034년)

- 주요 동향

- 직렬 하이브리드(연료전지가 배터리를 충전하고, 배터리가 모터를 구동하는 방식)

- 병렬 하이브리드(연료전지와 배터리 모두 모터를 구동)

- 직렬-병렬 하이브리드(복합 구성)

- 플러그인 하이브리드(외부 충전 기능)

제10장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- 딜러 네트워크

- 플릿 판매

- 리스 회사

- OEM 직접 판매

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제12장 기업 프로파일

- Global Player

- Alstom SA

- Ballard Power Systems

- BMW

- Bosch

- Cummins

- Honda Motor

- Hyundai Motor

- Kawasaki Heavy

- Symbio

- Toyota Motor

- Regional Player

- Bloom Energy Corporation

- BYD

- Daimler AG

- FuelCell Energy

- Hexagon Composites ASA

- Magna International

- Nissan Motor

- Stellantis NV

- Volvo Group AB

- Worthington Enterprises

- 신흥기업

- ITM Power PLC

- Nel ASA

- Plug Power

- PowerCell Sweden AB

- Viritech

The Hybrid Hydrogen-Electric Powertrain Market was valued at USD 283.8 million in 2024 and is estimated to grow at a CAGR of 14.5% to reach USD 1.1 billion by 2034.

The market's rapid growth is propelled by the rising global focus on sustainable, energy-efficient mobility and the shift toward low-emission transportation systems. Increasing adoption of hybrid hydrogen-electric powertrains in passenger, commercial, and specialized vehicles is being influenced by stringent government policies, improved fuel economy goals, and the demand for cleaner mobility options. Ongoing progress in lightweight materials, energy storage systems, and advanced powertrain architectures is further driving technological innovation. The expanding integration of smart manufacturing and digital automation is transforming the way manufacturers design and produce these systems. Through IoT-enabled monitoring, AI-powered process management, and predictive maintenance, automotive producers are achieving greater efficiency, reduced production downtime, and improved quality standards. Advanced fuel cell technology, high-efficiency electric motors, and intelligent energy management platforms are enhancing the overall capability of hybrid hydrogen-electric systems. The adoption of digital factory ecosystems, cloud-based operations, and interoperable automation platforms is aligning the market with global decarbonization and net-zero emission initiatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $283.8 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 14.5% |

In 2024, the battery pack segment held a 50% share and is forecast to grow at a CAGR of 14.5% between 2025 and 2034. Battery packs remain vital to hybrid hydrogen-electric powertrains, serving as the primary source for efficient energy storage and distribution. The increasing use of advanced battery technologies such as solid-state and high-density lithium-ion systems supports regenerative energy capture, extended driving range, and seamless coordination with hydrogen fuel cells and electric propulsion systems. Automakers and suppliers continue to prioritize high-performance battery packs to ensure consistent reliability, strong energy efficiency, and enhanced hybrid performance.

The passenger vehicle segment held a 75% share and is projected to grow at a CAGR of 14.4% through 2034. This segment's dominance is supported by growing production of hybrid and hydrogen-electric passenger cars, tighter emissions standards, and the expansion of smart manufacturing practices. Automotive manufacturers are investing heavily in intelligent factory solutions such as robotics, AI-based analytics, and cloud-connected monitoring systems to enhance production precision, energy efficiency, and compliance with environmental regulations.

Japan Hybrid Hydrogen-Electric Powertrain Market generated USD 69.6 million in 2024 and held a 33% share. The country's strong manufacturing base, along with extensive demand from original equipment manufacturers, Tier-1 and Tier-2 suppliers, and technology developers, supports steady market expansion. Japanese companies are implementing advanced digital solutions, including predictive analytics, IoT-based monitoring systems, and energy management platforms, across the entire powertrain value chain. The focus on modular and scalable powertrain systems enables manufacturers to meet strict environmental requirements while improving operational efficiency, reliability, and sustainability performance.

Prominent companies participating in the Global Hybrid Hydrogen-Electric Powertrain Market include Alstom SA, Ballard Power Systems, BMW Group, Cummins, Honda Motor, Hyundai Motor, Kawasaki Heavy, PowerCell Sweden AB, Symbio, and Toyota Motor. Leading manufacturers in the Global Hybrid Hydrogen-Electric Powertrain Market are strengthening their competitive positions through a combination of innovation, collaboration, and expansion. Many are investing in R&D to enhance system efficiency, hydrogen fuel cell performance, and battery integration. Strategic partnerships between automakers, component suppliers, and energy firms are accelerating technology commercialization and large-scale deployment. Companies are emphasizing digital transformation, integrating AI-based energy optimization, and adopting modular designs to improve scalability and flexibility. Furthermore, long-term investments in localized production facilities and sustainability-driven initiatives are helping leading players achieve cost advantages and align with global emission reduction goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Power Output

- 2.2.6 Hybrid Configuration

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Government decarbonization policies & hydrogen strategies

- 3.2.1.2 Technology maturation & commercial viability demonstration

- 3.2.1.3 Heavy-duty application advantages over battery-only solutions

- 3.2.1.4 Infrastructure investment & public-private partnerships

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system costs & component price premiums

- 3.2.2.2 Limited hydrogen refueling infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rail electrification gap & diesel replacement potential

- 3.2.3.2 Marine decarbonization requirements

- 3.2.3.3 Industrial & stationary power applications

- 3.2.3.4 Rail and marine decarbonization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global hydrogen & fuel cell policies

- 3.4.2 Emission & decarbonization regulations

- 3.4.3 Safety & vehicle standards

- 3.4.4 Infrastructure & refueling compliance

- 3.4.5 R&D & innovation incentives

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Fuel cell technologies

- 3.7.2 Battery & energy storage

- 3.7.3 Power electronics & control units

- 3.7.4 Electric motors & drivetrains

- 3.7.5 Digital & smart manufacturing integration

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Best case scenarios

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Battery pack

- 5.3 Fuel cell stack

- 5.4 Electric motor & drivetrain

- 5.5 Power electronics & control unit

- 5.6 Hydrogen storage system

- 5.7 Balance of plant (BoP)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Proton exchange membrane (PEM) fuel cell systems

- 7.3 Solid oxide fuel cell (SOFC) systems

- 7.4 Phosphoric acid fuel cell (PAFC) systems

- 7.5 Molten carbonate fuel cell (MCFC) systems

- 7.6 Alkaline fuel cell (AFC) systems

Chapter 8 Market Estimates & Forecast, By Power Output, 2021 - 2034 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Medium power (50-150 kW)

- 8.3 High power (150-300 kW)

- 8.4 Low power (<50 kW)

- 8.5 Ultra-High power (>300 kW)

Chapter 9 Market Estimates & Forecast, By Hybrid Configuration, 2021 - 2034 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Series hybrid (FC charges battery, battery drives motor)

- 9.3 Parallel hybrid (FC and battery both drive motor)

- 9.4 Series-Parallel hybrid (Combined configuration)

- 9.5 Plug-in hybrid (External charging capability)

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($ Mn, Units)

- 10.1 Key trends

- 10.2 Dealer Networks

- 10.3 Fleet Sales

- 10.4 Leasing Companies

- 10.5 OEM Direct Sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 Alstom SA

- 12.1.2 Ballard Power Systems

- 12.1.3 BMW

- 12.1.4 Bosch

- 12.1.5 Cummins

- 12.1.6 Honda Motor

- 12.1.7 Hyundai Motor

- 12.1.8 Kawasaki Heavy

- 12.1.9 Symbio

- 12.1.10 Toyota Motor

- 12.2 Regional Player

- 12.2.1 Bloom Energy Corporation

- 12.2.2 BYD

- 12.2.3 Daimler AG

- 12.2.4 FuelCell Energy

- 12.2.5 Hexagon Composites ASA

- 12.2.6 Magna International

- 12.2.7 Nissan Motor

- 12.2.8 Stellantis N.V.

- 12.2.9 Volvo Group AB

- 12.2.10 Worthington Enterprises

- 12.3 Emerging Players

- 12.3.1 ITM Power PLC

- 12.3.2 Nel ASA

- 12.3.3 Plug Power

- 12.3.4 PowerCell Sweden AB

- 12.3.5 Viritech