|

시장보고서

상품코드

1876592

AI 구동형 망막 스크리닝 장치 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)AI-Driven Retinal Screening Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

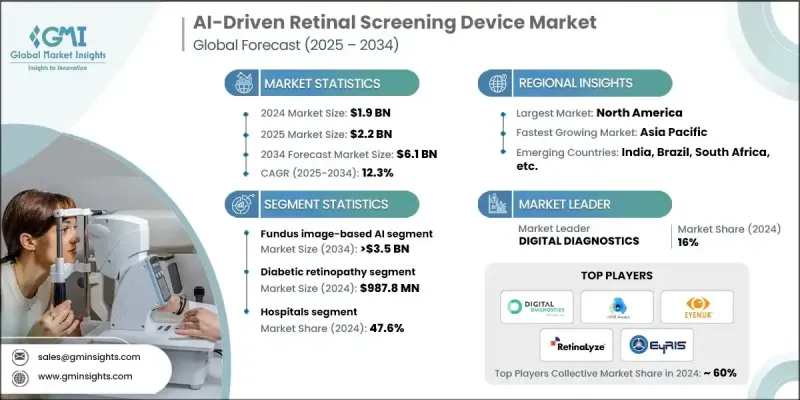

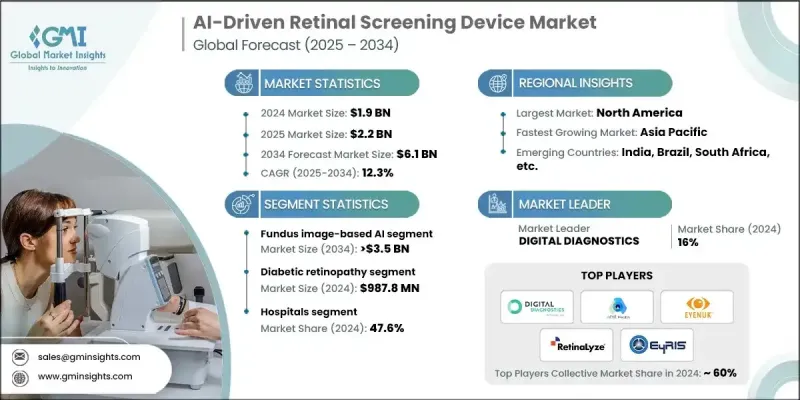

세계의 AI 구동형 망막 스크리닝 장치 시장은 2024년에 19억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 12.3%를 나타내 61억 달러에 이를 것으로 예측됩니다.

당뇨병 환자 증가, 기술 혁신의 진전, AI 기반 의료 영상 진단 도구의 보급 확대 등이 이 성장을 견인하는 주요 요인입니다. 정부 및 민간 의료 시스템에 의한 지원을 받은 계발 프로그램과 스크리닝 시책의 확대가 수요를 더욱 뒷받침하고 있습니다. 인공지능을 망막 진단에 통합함으로써 정밀하고 실시간 스크리닝이 가능해 여러 안 질환의 조기 발견을 지원합니다. 의료 제공업체가 예방 의료 및 원격 진단으로 이행하는 동안 AI 탑재 망막 진단 장치는 특히 자원이 부족한 지역에서 세계 안과 의료의 성과 향상과 접근성 향상에 필수적인 도구가되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 19억 달러 |

| 예측 금액 | 61억 달러 |

| CAGR | 12.3% |

심층 학습 알고리즘, 이미징 기술 및 휴대용 진단 장비의 발전으로 AI 기반 망막 스크리닝 시스템의 성능과 사용 편의성이 크게 향상되었습니다. 이러한 장치는 현재 실시간 분석을 제공하고 여러 눈 질환을 동시에 감지하고 디지털 건강 기록 시스템과 원활하게 작동합니다. 컴팩트한 클라우드 지원 영상 진단 도구의 출현으로 망막 스크리닝은 보다 빠르고 합리적인 가격으로 다양한 의료 환경에서 더 쉽게 액세스할 수 있게 되었습니다. 차세대 AI 알고리즘은 더욱 세련되고 미세한 망막 변화를 식별할 수 있게 되어 조기 개입과 맞춤 치료 계획을 가능하게 하고 있습니다. 세계보건기구(WHO)를 비롯해, 지방자치단체나 의료기관과 제휴해, 예방 가능한 실명과 싸우기 위한 계발 활동이나 대규모 스크리닝 캠페인을 실시했습니다. AI 기술을 탑재한 이동식 진단 유닛은 의료 서비스가 미치지 못한 지역에 도달하고, AI 스크리닝 툴은 표준 건강 진단에 통합되어 조기 발견과 예방적 안과 의료의 강화에 공헌하고 있습니다. AI 구동형 망막 스크리닝 장치는 머신러닝 알고리즘을 사용하여 망막 이미지를 분석하고 주요 안 질환을 정확하고 신속하게 확인하고 고품질 안과 진단에 대한 액세스 향상을 실현합니다.

2024년 기준에서 안저 이미지 기반 AI 부문은 56.7%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 12.7%로 35억 달러 규모에 이를 것으로 예측되고 있습니다. 이 부문의 이점은 시력 상실을 초래하는 눈 질환의 조기 발견에 대한 수요 증가로 인한 것입니다. 안저 이미지 기반 AI 도구는 고해상도 2D 망막 이미지를 사용하여 미세 동맥류, 출혈, 시신경 유두 이상과 같은 표면 수준의 이상을 감지합니다. 이러한 모델은 당뇨병성 망막증 및 고혈압성 망막증과 같은 병태를 인식하도록 훈련되었으며, 자동화된 영상 평가를 통해 신속하고 신뢰할 수 있는 진단을 가능하게 합니다.

당뇨병성 망막증 분야는 2024년 9억 8,780만 달러에 달했습니다. 당뇨병 환자의 시력 상실의 주요 원인 중 하나인 당뇨병성 망막증은 AI 구동 스크리닝 솔루션의 가장 흔한 응용 분야로 계속되고 있습니다. 이러한 장치는 망막 영상의 신속하고 비침습적인 분석을 제공하며 전문의의 개입 없이 1차 의료 환경에서 효과적으로 작동합니다. 당뇨병 관리 시설이나 지역 진료소에의 도입에 의해 특히 안과 의료 서비스에의 액세스가 제한되어 있는 지역에서 스크리닝의 보급 범위가 대폭 확대되었습니다. 당뇨병성 망막증의 높은 유병률과 예방 가능성은 업계 내에서 가장 영향력 있는 분야로 계속되는 요인이 되고 있습니다.

북미의 AI 구동형 망막 스크리닝 장치 시장은 2024년 47.3%의 점유율을 차지했습니다. 이 지역 시장 확대는 광범위한 혁신, 첨단 의료 에코시스템, AI 기술을 활용한 진단 가속화에 주목을 받고 있습니다. 확립된 인프라 외에, 예방적 안과 의료에 대한 강한 의식, 수많은 AI 의료 스타트업의 존재가 이러한 시스템의 꾸준한 도입을 지원하고 있습니다. 당뇨병과 노화 관련 안 질환 증가는 신속하고 정확한 질병 검출이 가능한 지능형 망막 스크리닝 도구에 대한 수요를 뒷받침하고 있습니다.

세계의 AI 구동형 망막 스크리닝 장치 시장에서 활동하는 주요 기업으로는 iCare, RetinaLyze, Heart Eye, EYENUK, Retmarker, Airdoc, AEYE Health, Evolucare, Topcon Healthcare, Remidio, MONA 등이 있습니다. Health, Forus Health, Identififeye Health, Visionix, Digital Diagnostics, EyRIS 등이 있습니다. 이러한 기업들은 세계 존재감을 강화하기 위해 기술 혁신과 시장 확대에 대한 투자를 계속하고 있습니다. AI 구동 망막 스크리닝 장치 시장의 주요 기업은 경쟁 우위를 높이기 위해 여러 전략을 채택하고 있습니다. 주요 초점은 보다 광범위한 망막 질환을 보다 정확하고 검출 가능한 첨단 AI 알고리즘의 개발을 위한 연구 개발에 있습니다. 많은 기업들이 AI 기반 스크리닝 툴의 도입 확대를 위해 병원, 클리닉, 원격 의료 제공업체와 전략적 제휴를 구축하고 있습니다. 또한 원활한 임상 워크플로우를 실현하기 위해 전자 건강 기록 플랫폼과의 시스템 통합을 중시하는 움직임도 볼 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 당뇨병 증가 경향

- 고령화 인구 증가

- 기술적 진보

- 높아지는 의식과 스크리닝 프로그램

- 업계의 잠재적 위험 및 과제

- 데이터 프라이버시와 보안에 대한 우려

- 엄격한 규제 지침

- 기회

- 다질환 검출 플랫폼의 개발

- 모바일 헬스(m 헬스)와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 투자환경

- 상환 시나리오

- 기술 진화의 타임라인

- 새로운 이용 사례와 응용 분야

- 망막 화상으로부터의 전신 질환 스크리닝

- 심혈관 위험 평가

- 신경질환의 검출

- 밸류체인 분석

- 하드웨어 제조업체

- AI 알고리즘 개발 기업

- 소프트웨어 플랫폼 제공 기업

- 의료 서비스 제공업체

- 최종 사용자 통합 파트너

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 향후 시장 동향

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 안저 영상 기반 AI

- OCT 기반 AI

- 다중 모달 AI

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 당뇨병성 망막증

- 노화 황반변성

- 녹내장

- 백내장

- 기타 용도

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 안과 클리닉

- 이동 진료소/농촌 진료 캠프

- 기타 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AEYE Health

- Airdoc

- DIGITAL DIAGNOSTICS

- evolucare

- EYENUK

- EyRIS

- Forus Health

- HEART EYE

- iCare

- identifeye HEALTH

- MONA.health

- remidio

- RetinaLyze

- Retmarker

- Topcon Healthcare

- Visionix

The Global AI-Driven Retinal Screening Device Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 6.1 billion by 2034.

Rising diabetes prevalence, growing technological innovation, and increasing adoption of AI-based medical imaging tools are among the major forces driving this growth. Expanding awareness programs and screening initiatives, supported by government and private healthcare systems, are further propelling demand. The integration of artificial intelligence into retinal diagnostics enables precise, real-time screening and supports early detection of multiple eye conditions. As healthcare providers move toward preventive care and remote diagnostics, AI-powered retinal devices are becoming essential tools for improving global eye health outcomes and enhancing accessibility, especially in low-resource regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 12.3% |

Advancements in deep learning algorithms, imaging technologies, and portable diagnostic equipment have significantly enhanced the performance and usability of AI-based retinal screening systems. These devices now provide real-time analytics, detect multiple eye disorders simultaneously, and seamlessly integrate with digital health record systems. The emergence of compact and cloud-enabled imaging tools has made retinal screening faster, more affordable, and more accessible across various healthcare settings. Next-generation AI algorithms are becoming more refined, capable of identifying subtle retinal changes that allow for earlier interventions and personalized treatment planning. Alongside global health organizations, local authorities, and medical institutions, they are implementing awareness drives and mass screening campaigns to fight preventable blindness. Mobile diagnostic units with AI technology are reaching underserved communities, while AI screening tools are being incorporated into standard checkups to strengthen early detection and preventive eye care. AI-driven retinal screening devices rely on machine learning algorithms to interpret images of the retina, providing accurate and timely identification of major ocular diseases and improving accessibility to quality eye diagnostics.

In 2024, the fundus image-based AI segment held 56.7% and is projected to reach USD 3.5 billion by 2034, growing at a CAGR of 12.7%. This segment's dominance is attributed to the rising demand for early detection of vision-threatening eye diseases. Fundus image-based AI tools use high-resolution 2D retinal images to detect surface-level irregularities, including microaneurysms, hemorrhages, and optic disc abnormalities. These models are trained to recognize conditions such as diabetic and hypertensive retinopathy, enabling rapid and reliable diagnostics through automated image assessment.

The diabetic retinopathy segment reached USD 987.8 million in 2024. As one of the primary causes of vision loss among individuals with diabetes, diabetic retinopathy continues to be the most common application for AI-driven screening solutions. These devices deliver rapid, non-invasive analysis of retinal images and can function effectively in primary healthcare environments without requiring specialist intervention. Their implementation in diabetes care facilities and community clinics has greatly expanded screening outreach, particularly in regions with limited access to ophthalmology services. The high prevalence and preventable nature of diabetic retinopathy continue to make it the most influential segment within the industry.

North America AI-Driven Retinal Screening Device Market held a 47.3% share in 2024. Market expansion in the region is driven by widespread innovation, an advanced healthcare ecosystem, and a heightened focus on accelerating diagnosis using AI technologies. The region's established infrastructure, coupled with strong awareness of preventive eye health and the presence of numerous AI healthcare startups, supports steady adoption of these systems. A growing incidence of diabetes and aging-related eye conditions is also fueling demand for intelligent retinal screening tools capable of fast and accurate disease detection.

Prominent companies operating in the Global AI-Driven Retinal Screening Device Market include iCare, RetinaLyze, Heart Eye, EYENUK, Retmarker, Airdoc, AEYE Health, Evolucare, Topcon Healthcare, Remidio, and MONA. Health, Forus Health, Identifeye Health, Visionix, Digital Diagnostics, and EyRIS. These players continue to invest in technological innovation and market expansion to strengthen their global presence. Leading companies in the AI-driven retinal screening device market are employing multiple strategies to enhance their competitive position. A major focus lies in research and development to create advanced AI algorithms capable of detecting a wider range of retinal conditions with greater accuracy. Many firms are forming strategic alliances with hospitals, clinics, and telemedicine providers to expand the deployment of AI-based screening tools. Companies are also emphasizing the integration of their systems with electronic health record platforms to enable seamless clinical workflows.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes

- 3.2.1.2 Rising geriatric population

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.3 Opportunities

- 3.2.3.1 Multi-disease detection platform development

- 3.2.3.2 Integration with mobile health (mHealth)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Reimbursement scenario

- 3.8 Technology evolution timeline

- 3.9 Emerging use cases & applications

- 3.9.1 Systemic disease screening from retinal images

- 3.9.2 Cardiovascular risk assessment

- 3.9.3 Neurological condition detection

- 3.10 Value chain analysis

- 3.10.1 Hardware manufacturers

- 3.10.2 AI algorithm developers

- 3.10.3 Software platform providers

- 3.10.4 Healthcare service providers

- 3.10.5 End use integration partners

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fundus image-based AI

- 5.3 OCT-based AI

- 5.4 Multi-modal AI

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetic retinopathy

- 6.3 Age-related macular degeneration

- 6.4 Glaucoma

- 6.5 Cataract

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ophthalmology clinics

- 7.4 Mobile clinics/Rural camps

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AEYE Health

- 9.2 Airdoc

- 9.3 DIGITAL DIAGNOSTICS

- 9.4 evolucare

- 9.5 EYENUK

- 9.6 EyRIS

- 9.7 Forus Health

- 9.8 HEART EYE

- 9.9 iCare

- 9.10 identifeye HEALTH

- 9.11 MONA.health

- 9.12 remidio

- 9.13 RetinaLyze

- 9.14 Retmarker

- 9.15 Topcon Healthcare

- 9.16 Visionix