|

시장보고서

상품코드

1876594

후면 전력 공급 네트워크 기술 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Backside Power Delivery Network Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

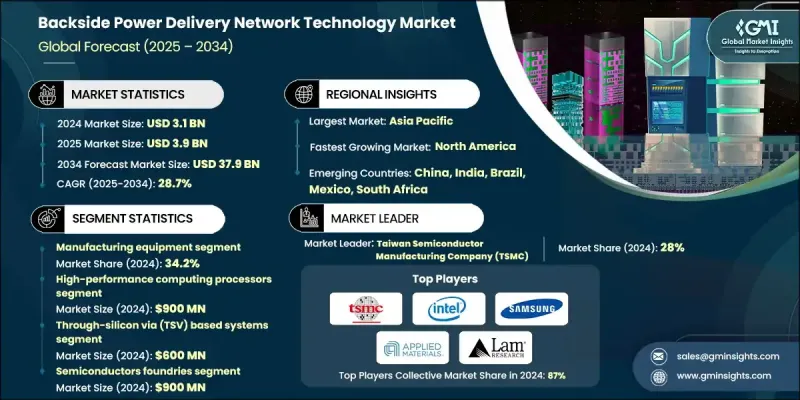

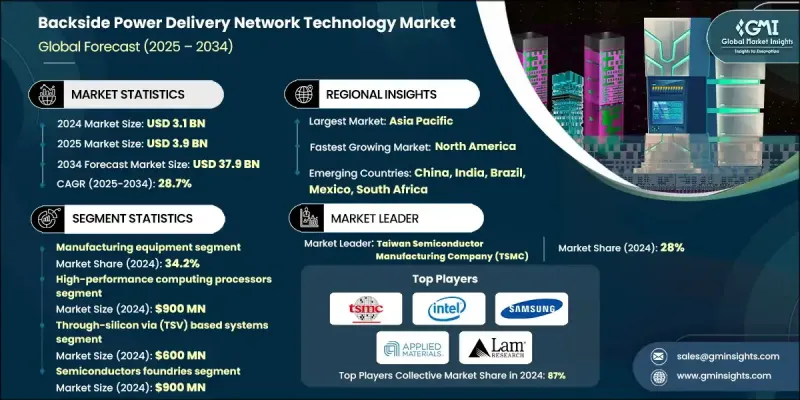

세계의 후면 전력 공급 네트워크 기술 시장은 2024년에 31억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 28.7%를 나타내 379억 달러에 이를 것으로 예측됩니다.

이러한 급속한 성장은 AI, 5G, 고성능 컴퓨팅 용도를 위한 에너지 효율 향상, 신호 잡음 감소, 칩 성능 개선을 실현하는 첨단 반도체 설계에 대한 수요 급증으로 추진되고 있습니다. 후면 전력 공급 네트워크(BSPDN) 기술이 IR 드롭을 최소화하고 트랜지스터의 지속적인 미세화를 지원하는 능력은 주요 반도체 파운드리 및 칩 제조업체에서 광범위한 채택을 촉진하고 있습니다. 인공지능, 데이터센터 인프라, 클라우드 기반 컴퓨팅에 대한 수요 가속화는 컴팩트하고 고성능 디바이스에서 안정적이고 효율적인 전력 공급을 보장하는 BSPDN의 중요성을 더욱 높여줍니다. 또한 3D 칩 아키텍처와 칩렛 기반 설계의 상승으로 BSPDN 시스템의 통합이 가속화되고 있습니다. 이 기술은 전원 배선과 신호 배선을 분리하여 상호 연결 밀도를 높이고 신호 무결성을 향상시키고 자동차, IoT 및 차세대 컴퓨팅 플랫폼에서 사용되는 첨단 프로세서의 성능을 최적화합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 31억 달러 |

| 예측 금액 | 379억 달러 |

| CAGR | 28.7% |

제조 장비 부문은 2024년에 34.2%의 점유율을 차지했습니다. 이 부문은 제조 성능과 에너지 효율을 향상시키는 혁신적인 전력 공급 시스템 수요 증가로 인해 후면 공급 네트워크 기술 시장을 선도했습니다. 반도체 제조 분야의 기업은 전력 손실 감소, 열 성능 향상 및 종합 설비 생산성 향상을 위해 후면 전력 공급을 채택하고 있습니다. 이 기술의 통합은 보다 우수한 방열성, 고속 데이터 처리량 및 고전력 밀도를 실현하여 현대 칩 제조 공정에서 중요한 구성 요소가 되었습니다.

2024년 고성능 컴퓨팅(HPC) 프로세서 분야는 9억 달러 시장 규모를 창출했습니다. HPC 프로세서는 까다로운 워크로드를 지원하는 효율적이고 컴팩트한 전력 공급 시스템이 필요하기 때문에 시장을 견인하고 있습니다. 이러한 프로세서는 지연을 최소화하고 대역폭을 향상시키기 위해 고급 패키징 및 상호 연결 기술에 의존합니다. AI 구동 워크로드, 복잡한 시뮬레이션 및 데이터 분석에 대한 수요가 증가함에 따라 안정적이고 확장 가능한 전력 솔루션의 필요성이 점점 중요해지고 있습니다. HPC 프로세서에서 BSPDN 기술을 채택함으로써 제조업체는 빠르고 전력 집약적인 컴퓨팅 환경 요구 사항을 충족 할 수 있으며 반도체 아키텍처의 혁신의 중요한 추진력이 되었습니다.

북미의 후면 전력 공급 네트워크 기술 시장은 2024년에 29.4%의 점유율을 차지했습니다. 이 지역의 이점은 첨단 컴퓨팅 시스템, AI 구동 기술 및 대규모 데이터센터에 대한 강한 수요에 의해 지원됩니다. 확립된 반도체 에코시스템, 엄청난 연구 개발 투자, 칩 제조 이니셔티브에 대한 정부 지원이 시장 개척을 더욱 가속화하고 있습니다. 이 지역의 기술 개발 기업과 주요 파운드리 간의 협력은 전력 공급 설계와 통합 기술의 진보를 지속적으로 촉진하고 있습니다. 이 역동적인 환경이 선진적 상호접속 기술의 보급을 추진하고, 북미가 반도체 혁신과 생산 효율의 주요 거점으로서의 지위를 확립하는 원인이 되고 있습니다.

세계 후면 전력 공급 네트워크 기술 시장의 주요 기업으로는 Synopsys Inc., Samsung Electronics, Veeco Instruments Inc., Applied Materials, Inc., Tokyo Electron Limited, ASE Technology Holding Co., Ltd., GlobalFoundries, Intel Corporation, Ansys, Inc., Taiwan Semiconductor Manufacturing Company (TSMC), Infineon Technologies AG, Amkor Technology, KLA Corporation, ASML Holding N.V., Cadence Design Systems, Inc., Lam Research Corporation, Advantest Corporation, Entegris, Inc., Onto Innovation Inc., Screen Holdings Co., Ltd 등을 들 수 있습니다. 이러한 기업들은 전력공급기술의 혁신을 추진하고 세계 반도체 제조능력 강화에 적극적으로 임하고 있습니다. 후면 전력 공급 네트워크 기술 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 다양한 전략을 추구하고 있습니다. 주요 초점은 정밀한 전력 배선 및 칩 성능 향상을 가능하게 하는 첨단 리소그래피 및 에칭 기술 개발을 위한 집중적인 연구 개발에 있습니다. 많은 기업들이 BSPDN 대응 칩의 대량 생산을 지원하기 위한 장치 최적화에 투자하고 있습니다. 반도체 제조업체, 설계 소프트웨어 공급자 및 장비 공급업체 간의 전략적 제휴는 업계를 통한 혁신을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 고도의 반도체 노드(3nm 미만)에 대한 수요 증가에 수반해, 전력 효율의 향상과 IR 강하의 저감이 요구되고 있습니다.

- AI 및 고성능 컴퓨팅(HPC) 칩의 채용 확대에 의해 보다 높은 트랜지스터 밀도의 필요성이 높아지고 있습니다.

- 모바일 및 데이터센터용 프로세서의 보급 확대에 따라 보다 우수한 전력 무결성과 열 관리가 요구되고 있습니다.

- 인텔이나 TSMC 등 주요 기업에 의한 기술 혁신이 BSPDN의 상용화를 가속시키고 있습니다.

- 업계의 잠재적 위험 및 과제

- 복잡한 통합 프로세스와 새로운 설계 조사 방법으로 개발 비용이 증가합니다.

- 제조 능력의 제한과 선진 팹에의 의존이, 대규모 도입의 방해가 되고 있습니다.

- 시장 기회

- AI 가속기, GPU, 차세대 프로세서에서의 BSPDN 채용 확대

- 이면 급전을 보완하는 2.5D/3D 패키징 기술의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 기술 동향

- 현재의 동향

- 신흥기술

- 파이프라인 분석

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수 및 합병

- 제휴 및 협력 관계

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 제조 장비

- 재료 및 소모품

- 계측 및 검사 시스템

- 설계 및 시뮬레이션 소프트웨어

제6장 시장 추계·예측 : 기술 유형별(2021-2034년)

- 주요 동향

- 실리콘 관통 전극(TSV) 기반 시스템

- 매립형 전력 레일 시스템

- 직접 후면 접촉 시스템

- 하이브리드 통합 시스템

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 고성능 컴퓨팅 프로세서

- 모바일 및 소비자용 프로세서

- 자동차 반도체 소자

- 산업용 및 IoT 애플리케이션

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 반도체 파운드리

- 통합 장치 제조업체(IDM)

- 장비 및 재료 공급업체

- 시스템 통합업체 및 OEM

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Taiwan Semiconductor Manufacturing Company(TSMC)

- Intel Corporation

- Samsung Electronics(Samsung Foundry)

- GlobalFoundries

- ASE Technology Holding Co., Ltd.(ASE Group)

- Amkor Technology

- Applied Materials, Inc.

- Lam Research Corporation

- ASML Holding NV

- Tokyo Electron Limited

- KLA Corporation

- Cadence Design Systems, Inc.

- Synopsys Inc.

- Ansys, Inc.

- Advantest Corporation

- Entegris, Inc.

- Screen Holdings Co., Ltd.

- Veeco Instruments Inc.

- Onto Innovation Inc.

- Infineon Technologies AG

The Global Backside Power Delivery Network Technology Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 28.7% to reach USD 37.9 billion by 2034.

The rapid growth is fueled by the surging need for advanced semiconductor designs that enhance energy efficiency, reduce signal noise, and improve chip performance for AI, 5G, and high-performance computing applications. The capability of BSPDN technology to minimize IR drop and support continued transistor scaling is encouraging widespread adoption among major semiconductor foundries and chip manufacturers. The accelerating demand for artificial intelligence, data center infrastructure, and cloud-based computing is further amplifying the importance of BSPDN, as it ensures reliable and efficient power delivery in compact, high-performance devices. Moreover, the rise of 3D chip architectures and chiplet-based designs is accelerating the integration of BSPDN systems. By separating power and signal routing, this technology increases interconnect density, enhances signal integrity, and optimizes performance in advanced processors used across automotive, IoT, and next-generation computing platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $37.9 Billion |

| CAGR | 28.7% |

The manufacturing equipment segment held a 34.2% share in 2024. This segment leads the Backside Power Delivery Network Technology Market due to the rising need for innovative power delivery systems that improve manufacturing performance and energy efficiency. Companies in the semiconductor manufacturing space are adopting backside power delivery to reduce power loss, improve thermal performance, and enhance overall equipment productivity. The integration of this technology supports better heat dissipation, faster data throughput, and higher power density, making it a critical component for modern chip fabrication processes.

In 2024, the high-performance computing (HPC) processors segment generated USD 900 million. HPC processors are leading the market as they require efficient and compact power delivery systems capable of supporting demanding workloads. These processors depend on advanced packaging and interconnect technologies to minimize latency and improve bandwidth. As demand for AI-driven workloads, complex simulations, and data analytics grows, the need for reliable and scalable power solutions becomes increasingly essential. The adoption of BSPDN technology within HPC processors allows manufacturers to meet the requirements of high-speed, power-intensive computing environments, making it a key enabler of innovation in semiconductor architecture.

North America Backside Power Delivery Network Technology Market held a 29.4% share in 2024. The region's dominance is supported by strong demand for advanced computing systems, AI-driven technologies, and large-scale data centers. A well-established semiconductor ecosystem, significant R&D investments, and government support for chip manufacturing initiatives have further accelerated market development. The collaboration between technology developers and leading foundries in the region continues to foster advancements in power delivery design and integration. This dynamic environment is driving widespread adoption of advanced interconnect technologies, contributing to North America's position as a major hub for semiconductor innovation and production efficiency.

Prominent players in the Global Backside Power Delivery Network Technology Market include Synopsys Inc., Samsung Electronics, Veeco Instruments Inc., Applied Materials, Inc., Tokyo Electron Limited, ASE Technology Holding Co., Ltd., GlobalFoundries, Intel Corporation, Ansys, Inc., Taiwan Semiconductor Manufacturing Company (TSMC), Infineon Technologies AG, Amkor Technology, KLA Corporation, ASML Holding N.V., Cadence Design Systems, Inc., Lam Research Corporation, Advantest Corporation, Entegris, Inc., Onto Innovation Inc., and Screen Holdings Co., Ltd. These companies are actively engaged in advancing power delivery innovations and strengthening global semiconductor manufacturing capabilities. Key players in the Backside Power Delivery Network Technology Market are pursuing diverse strategies to reinforce their market position. A primary focus is on intensive R&D to develop advanced lithography and etching technologies that enable precise power routing and improved chip performance. Many companies are investing in equipment optimization to support high-volume production of BSPDN-enabled chips. Strategic alliances between semiconductor manufacturers, design software providers, and equipment suppliers are fostering cross-industry innovation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional Trends

- 2.2.2 Component Trends

- 2.2.3 Technology Type Trends

- 2.2.4 End Use Trends

- 2.2.5 Application Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for advanced semiconductor nodes (below 3nm) requiring improved power efficiency and reduced IR drop.

- 3.2.1.2 Increasing adoption of AI and high-performance computing (HPC) chips driving need for higher transistor density.

- 3.2.1.3 Rising use of mobile and data center processors demanding better power integrity and thermal management.

- 3.2.1.4 Technological innovation by key players like Intel and TSMC accelerating BSPDN commercialization.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex integration process and new design methodologies increase development costs.

- 3.2.2.2 Limited manufacturing capacity and dependence on advanced fabs slow large-scale adoption.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing use of BSPDN in AI accelerators, GPUs, and next-generation processors.

- 3.2.3.2 Expansion of 2.5D/3D packaging technologies complementing backside power delivery.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Manufacturing Equipment

- 5.3 Materials & Consumables

- 5.4 Metrology & Inspection Systems

- 5.5 Design & Simulation Software

Chapter 6 Market Estimates and Forecast, By Technology Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Through-Silicon Via (TSV) Based Systems

- 6.3 Buried Power Rail Systems

- 6.4 Direct Backside Contact Systems

- 6.5 Hybrid Integration Systems

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 High-Performance Computing Processors

- 7.3 Mobile & Consumer Processors

- 7.4 Automotive Semiconductor Devices

- 7.5 Industrial & IoT Applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Semiconductor Foundries

- 8.3 Integrated Device Manufacturers (IDMs)

- 8.4 Equipment & Materials Suppliers

- 8.5 System Integrators & OEMs

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Taiwan Semiconductor Manufacturing Company (TSMC)

- 10.2 Intel Corporation

- 10.3 Samsung Electronics (Samsung Foundry)

- 10.4 GlobalFoundries

- 10.5 ASE Technology Holding Co., Ltd. (ASE Group)

- 10.6 Amkor Technology

- 10.7 Applied Materials, Inc.

- 10.8 Lam Research Corporation

- 10.9 ASML Holding N.V.

- 10.10 Tokyo Electron Limited

- 10.11 KLA Corporation

- 10.12 Cadence Design Systems, Inc.

- 10.13 Synopsys Inc.

- 10.14 Ansys, Inc.

- 10.15 Advantest Corporation

- 10.16 Entegris, Inc.

- 10.17 Screen Holdings Co., Ltd.

- 10.18 Veeco Instruments Inc.

- 10.19 Onto Innovation Inc.

- 10.20 Infineon Technologies AG