|

시장보고서

상품코드

1876613

3D 프린팅 수술 기구 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)3D Printed Surgical Instrument Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

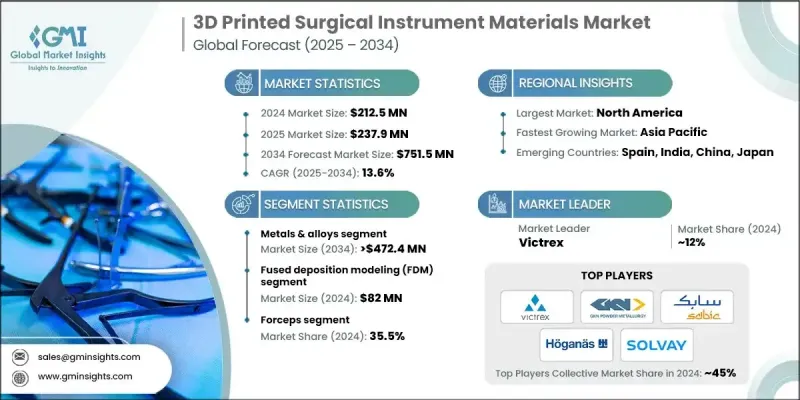

세계의 3D 프린팅 수술 기구 시장은 2024년에 2억 1,250만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 13.6%로 성장할 전망이며, 7억 5,150만 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 생체적합성 및 멸균 가능한 재료의 지속적인 진보, 환자 특화형 수술 기구에 대한 수요 증가, 의료 시설에 있어서 3D 프린팅 기술의 보급 확대, 저침습 및 복잡한 수술 증가를 들 수 있습니다. 3D 프린팅 수술 기구에는 암, 집게, 클램프, 견인기 등의 기구 제조에 사용되는 금속, 폴리머, 복합재료가 포함됩니다. 이러한 재료는 높은 기계적 강도, 살균 가능성 및 생체 적합성을 보장해야 합니다. 외과의사는 수술의 정확성 및 환자의 치료 성과를 높이기 위해 맞춤형 기구를 점점 더 요구하고 있습니다. 적층 성형 기술은 정밀한 설계, 인체 공학을 기반으로 한 맞춤화, 비용 효율적인 생산을 가능하게 합니다. 가볍고 내구성이 뛰어난 멸균 가능한 금속, 폴리머 및 복합재료의 지속적인 혁신은 의료 분야에서 3D 프린팅의 적용 범위를 넓혀 특수 수술 도구의 급속한 개발을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 2억 1,250만 달러 |

| 예측 금액 | 7억 5,150만 달러 |

| CAGR | 13.6% |

금속 및 합금 부문은 탁월한 기계적 강도, 정밀도 및 멸균 호환성으로 2024년에 62.6%의 점유율을 차지했습니다. 티타늄, 스테인레스 스틸, 코발트 크롬 등의 재료는 우수한 인장 강도, 내마모성, 장기 내구성을 갖추고 있으며 반복 수술 용도에 이상적입니다. 이러한 특성은 높은 스트레스 수술 환경에서 신뢰성을 보장하고 광범위한 채용을 촉진합니다.

용융 적층법(FDM) 부문은 2024년에 8,200만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 13.5%로 성장할 것으로 예측됩니다. FDM은 비용 효율성이 뛰어나 수술 도구의 신속한 프로토타입 및 초기 단계의 생산을 가능하게 합니다. 간편성, 유지 보수, 병원 및 수술센터 간의 간편한 통합으로 맞춤형 기기의 주문형 인쇄를 촉진하여 개발 가속화와 비용 절감을 실현합니다.

북미의 3D 프린팅 수술 기구 시장은 첨단 의료 인프라, 설비가 잘 갖추어진 병원, 수술 용도에 적층 조형 기술 도입을 추진하는 연구기관에 힘입어 2024년에 42.2%의 점유율을 차지했습니다. 정부, 학술기관, 민간 기업에 의한 3D 인쇄 연구에 대한 엄청난 투자와 생체적합성 폴리머 및 금속 합금의 지속적인 혁신은 지역 성장을 이끌고 있습니다.

세계 3D 프린팅 수술 기구 시장의 주요 기업으로는 3D SYSTEMS, Apium, Arkema, Ensinger, EOS, Evonik, Formlabs, GKN Powder Metallurgy, Hoganas, INDO-MIM, RENISHAW, SABIC, SOLVAY, Stratasys, Victrex 등이 있습니다. 3D 프린팅 수술 기구 시장의 기업은 첨단 생체 적합성 및 멸균 가능한 재료 개발을 위한 연구개발 투자를 통해 경쟁력을 강화하고 있습니다. 각 환자마다 맞춤형 솔루션을 개발하고 복잡한 수술 요구 사항을 충족하기 위해 제품 포트폴리오를 확대하는 데 주력하고 있습니다. 병원, 의료기기 제조업체, 학술 기관과의 전략적 제휴는 시장 침투와 보급을 촉진합니다. 또한 기업은 적층 조형 기술의 혁신을 활용하여 생산 비용 절감, 정밀도 향상, 기구 개발의 신속화를 도모하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 맞춤형 환자 고유의 수술 기구에 대한 수요 증가

- 생체 적합성 및 멸균 가능한 3D 프린팅 재료의 진보

- 의료 분야에 있어서 적층 조형의 채용 확대

- 의료용 3D 프린팅 연구개발 투자 증가

- 업계의 잠재적 위험 및 과제

- 표준화 부족 및 규제 상 과제

- 특정 폴리머에 있어서 기계적 강도의 한계

- 시장 기회

- 신흥 의료 시장 진출

- 설계 최적화의 AI 및 시뮬레이션 툴 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 동향

- 현재의 기술 동향

- 신흥 기술

- 소비자 인사이트

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 금속 및 합금

- 폴리머

- 생분해성 폴리머

- 기타 재료

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 용융 적층법(FDM)

- 선택적 레이저 소결(SLS)

- 스테레오 리소그래피(SLA)

- 기타 기술

제7장 시장 추계 및 예측 : 기구별(2021-2034년)

- 주요 동향

- 집게

- 클램프

- 리트랙터

- 여성

- 기타 기구

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 지역

제9장 기업 프로파일

- 3D SYSTEMS

- Apium

- Arkema

- Ensinger

- EOS

- Evonik

- Formlabs

- GKN Powder Metallurgy

- Hoganas

- INDO-MIM

- RENISHAW

- SABIC

- SOLVAY

- Stratasys

- Victrex

The Global 3D Printed Surgical Instrument Materials Market was valued at USD 212.5 million in 2024 and is estimated to grow at a CAGR of 13.6% to reach USD 751.5 million by 2034.

Market expansion is fueled by ongoing advancements in biocompatible and sterilizable materials, rising demand for patient-specific surgical instruments, increasing adoption of 3D printing across healthcare facilities, and the growing prevalence of minimally invasive and complex surgical procedures. 3D printed surgical instrument materials include metals, polymers, and composites used to fabricate tools such as scalpels, forceps, clamps, and retractors. These materials must ensure high mechanical strength, sterilizability, and biocompatibility. Surgeons are increasingly seeking customized instruments to enhance surgical accuracy and patient outcomes. Additive manufacturing enables precise design, ergonomic customization, and cost-effective production. Continuous innovation in lightweight, durable, and sterilizable metals, polymers, and composite materials is broadening the application of 3D printing in healthcare, supporting the rapid development of specialized surgical tools.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $212.5 Million |

| Forecast Value | $751.5 Million |

| CAGR | 13.6% |

The metals & alloys segment held a 62.6% share in 2024 owing to their exceptional mechanical strength, precision, and sterilization compatibility. Materials such as titanium, stainless steel, and cobalt-chrome offer superior tensile strength, wear resistance, and long-term durability, making them ideal for repeated surgical use. These properties ensure reliability in high-stress surgical environments, driving their widespread adoption.

The fused deposition modeling (FDM) segment was valued at USD 82 million in 2024 and is expected to grow at a CAGR of 13.5% through 2034. FDM is highly cost-effective, enabling rapid prototyping and early-stage production of surgical instruments. Its simplicity, low maintenance, and ease of integration into hospitals and surgical centers facilitate on-demand printing of customized tools, accelerating development while reducing costs.

North America 3D Printed Surgical Instrument Materials Market held a 42.2% share in 2024, supported by advanced healthcare infrastructure, well-equipped hospitals, and research institutions adopting additive manufacturing for surgical applications. Substantial investments by governments, academia, and private enterprises in 3D printing research, along with continuous innovation in biocompatible polymers and metal alloys, are driving regional growth.

Key players operating in the Global 3D Printed Surgical Instrument Materials Market include 3D SYSTEMS, Apium, Arkema, Ensinger, EOS, Evonik, Formlabs, GKN Powder Metallurgy, Hoganas, INDO-MIM, RENISHAW, SABIC, SOLVAY, Stratasys, and Victrex. Companies in the 3D Printed Surgical Instrument Materials Market are strengthening their position by investing in research and development to create advanced biocompatible and sterilizable materials. They are focusing on developing customizable, patient-specific solutions and expanding their product portfolios to cater to complex surgical requirements. Strategic collaborations with hospitals, medical device manufacturers, and academic institutions enhance market reach and adoption. Firms are also leveraging additive manufacturing innovations to reduce production costs, improve precision, and accelerate instrument development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Material trends

- 2.2.3 Technology trends

- 2.2.4 Instruments trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for customized and patient-specific surgical instruments

- 3.2.1.2 Advancements in biocompatible and sterilizable 3D printing materials

- 3.2.1.3 Increasing adoption of additive manufacturing in healthcare

- 3.2.1.4 Rising investments in medical 3D printing R&D

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited standardization and regulatory challenges

- 3.2.2.2 Mechanical strength limitations of certain polymers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging healthcare markets

- 3.2.3.2 Integration of AI and simulation tools in design optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer insights

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Metals & alloys

- 5.3 Polymers

- 5.4 Biodegradable polymer

- 5.5 Other materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fused deposition modeling (FDM)

- 6.3 Selective laser sintering (SLS)

- 6.4 Stereolithography (SLA)

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Instruments, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Forceps

- 7.3 Clamps

- 7.4 Retractors

- 7.5 Scalpels

- 7.6 Other instruments

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 RoW

Chapter 9 Company Profiles

- 9.1 3D SYSTEMS

- 9.2 Apium

- 9.3 Arkema

- 9.4 Ensinger

- 9.5 EOS

- 9.6 Evonik

- 9.7 Formlabs

- 9.8 GKN Powder Metallurgy

- 9.9 Hoganas

- 9.10 INDO-MIM

- 9.11 RENISHAW

- 9.12 SABIC

- 9.13 SOLVAY

- 9.14 Stratasys

- 9.15 Victrex

(주말 및 공휴일 제외)