|

시장보고서

상품코드

1876617

풀러렌계 특수 화학제품 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Fullerene-Based Specialty Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

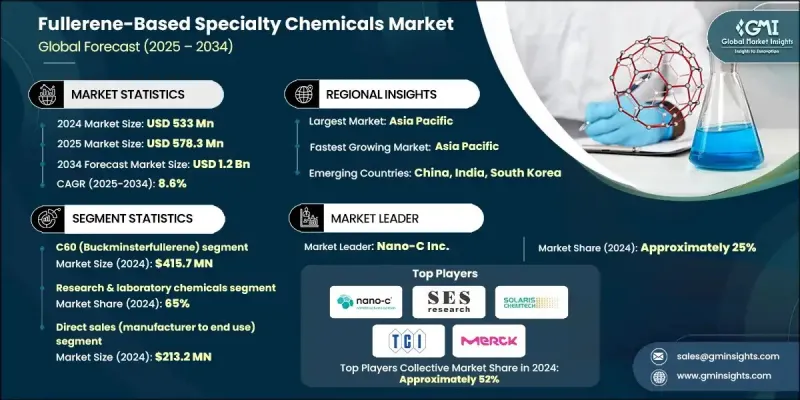

세계의 풀러렌계 특수 화학제품 시장은 2024년에 5억 3,300만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.6%로 성장할 전망이며, 12억 달러에 이를 것으로 예측되고 있습니다.

성장의 기세는 주로 풀러렌의 기능화와 합성에 있어서 현저한 진보에 힘입어 유기 태양전지(OPV) 및 관련 전자 용도 분야에서 확대될 기회에 의해 견인되고 있습니다. C-60 및 C-70 풀러렌의 용해성, 안정성 및 전자 수용 특성의 향상은 유기 전자 및 에너지 시스템으로의 통합을 가속화하고 있습니다. 나노기술에 대한 강력한 조사 자금 제공에 더해, 성숙하고 있는 규제 프레임워크과 정책 인센티브에 의해 에너지, 일렉트로닉스, 의약품의 연구 개발 분야에 있어서, 풀러렌계 재료의 적용 범위는 계속 확대되고 있습니다. 고성능 나노 재료에 대한 수요가 증가함에 따라 풀러렌 및 그 유도체는 차세대 디바이스, 유연한 전자 제품 및 첨단 화학 제제에서 잠재적 가능성이 점점 인식되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 5억 3,300만 달러 |

| 예측 금액 | 12억 달러 |

| CAGR | 8.6% |

2024년 전자 및 OPV 부문은 1억 1,730만 달러의 매출을 창출하였고, 22%의 점유율을 차지했습니다. 이 부문은 유기 일렉트로닉스의 발전과 확장성 및 디바이스 성능의 향상을 보장하는 솔루션 공정 가능한 풀러렌 유도체의 채택 확대를 통해 계속 성장하고 있습니다. 이러한 첨단 재료를 유연하고 에너지 효율적인 기술에 활용함으로써 여러 분야의 추가 수요가 촉진되고 있습니다.

직접 판매 채널은 2024년에 2억 1,320만 달러로 평가되어 40%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 8.6%로 성장할 것으로 예측됩니다. 이 채널이 지배적인 지위를 유지하는 배경에는 풀러렌 제품의 높은 전문성이 있습니다. 이러한 제품은 종종 맞춤형 사양, 엄격한 품질 관리, 연구 기관, 전자 기기 제조업체, 제약 회사 등 최종 사용자와 긴밀한 협력이 필요합니다.

아시아태평양의 풀러렌계 특수 화학제품 시장은 2024년 2억 5,590만 달러 규모로 48%의 점유율을 차지했습니다. 이 지역은 2025-2034년 연평균 복합 성장률(CAGR) 10.2%로 성장할 것으로 예측됩니다. 이러한 견조한 성장은 견고한 전자기기 제조 능력, 광범위한 화학물질 공급 인프라, 나노물질 및 차세대 태양광 발전 연구를 촉진하는 정부의 적극적인 조치에 의해 지원됩니다. 중국, 일본, 한국, 인도는 역동적인 스타트업 에코시스템과 첨단 연구개발 프로그램을 지원하며 생산과 혁신의 최전선에 서 있습니다.

세계 풀러렌계 특수 화학제품 시장의 주요 기업으로는 Nano-C Inc., SES Research Inc., Solaris Chem, TCI (Tokyo Chemical Industry), Sigma-Aldrich / Merck KGaA, American Elements, Strem Chemicals, Ossila, Alfa Aesar (Thermo Fisher), Frontier Carbon Corporation, ACS Material, and Abvigen Inc 등을 들 수 있습니다. 풀러렌계 특수 화학제품 시장의 기업은 재료 성능의 향상과 용도 분야의 확대를 위해 연구개발에 적극적으로 투자하고 있습니다. 생산 효율 향상과 안정적인 제품 품질 확보를 목적으로 전략적 제휴와 장기 공급 계약이 맺어지고 있습니다. 다수의 기업은 고도의 전자기기나 태양광 발전 용도의 진화하는 요구에 대응하기 위해 고순도 및 기능화 유도체의 개발을 통해 제품 포트폴리오의 다양화를 추진하고 있습니다. 또한 많은 기업들이 맞춤형 솔루션과 기술 지원을 제공하기 위해 주요 최종 사용자와 직접적인 파트너십에 초점을 맞추고 유통 네트워크를 최적화하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 과제 및 어려움

- 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 형태별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 대한 배려

제4장 경쟁 구도

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- C60(백민스터 풀러렌)

- 95% 순도 등급

- 99% 순도 등급

- 99.5% 순도 등급

- 99.9% 순도 등급

- C70 풀러렌

- 표준 등급

- 고순도 등급

- 관능기화 풀러렌 유도체

- PCBM((6,6)-페닐-C61-부티르산 메틸 에스테르)

- ICBA(인덴-C60 바이어드덕트)

- 수용성 풀러렌 유도체

- 커스텀 기능화 유도체

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 조사 및 실험용 화학제품

- 학술 및 대학 조사

- 의약품 연구 개발 용도

- 재료에 관한 조사

- 정부계 연구기관

- 상업 조사 서비스

- 전자기기 및 유기 태양전지

- 유기 태양전지(OPV)의 용도 분야

- 반도체 용도

- 전자부품의 통합

- 디스플레이 기술 용도

- 특수 산업 용도

- 고급 촉매 용도

- 특수 코팅 및 재료

- 트라이볼로지 용도 분야

- 틈새 산업 용도

- 수탁 연구 및 커스텀 합성

- 의약품 수탁 조사

- 기술계 기업용 연구 개발 지원

- 커스텀 유도체 개발

- 전문 연구 화학제품 서비스

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매(제조업체로부터 최종 용도까지)

- 화학제품 도매업체

- 특수 화학제품 공급업체

- 온라인 화학제품 시장

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Nano-C Inc.

- SES Research Inc.

- Solaris Chem

- TCI(Tokyo Chemical Industry)

- Sigma-Aldrich/Merck KGaA

- American Elements

- Strem Chemicals

- Ossila

- Alfa Aesar(Thermo Fisher)

- Frontier Carbon Corporation

- ACS Material

- Abvigen Inc.

The Global Fullerene-Based Specialty Chemicals Market was valued at USD 533 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.2 billion by 2034.

Growth momentum is primarily driven by expanding opportunities in organic photovoltaics (OPV) and related electronic applications, supported by significant advancements in fullerene functionalization and synthesis. Enhanced solubility, stability, and electron-accepting properties of C-60 and C-70 fullerenes are accelerating their integration into organic electronics and energy systems. The strong research funding for nanotechnology, coupled with maturing regulatory frameworks and policy incentives, continues to expand the scope of fullerene-based materials across energy, electronics, and pharmaceutical R&D. As the demand for high-performance nanomaterials rises, fullerenes and their derivatives are increasingly recognized for their potential in next-generation devices, flexible electronics, and advanced chemical formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $533 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 8.6% |

In 2024, the electronics and OPV segment generated USD 117.3 million, representing a 22% share. The segment continues to thrive on advancements in organic electronics and the growing adoption of solution-processable fullerene derivatives that ensure improved scalability and device performance. The use of these advanced materials in flexible and energy-efficient technologies is fueling further demand across multiple sectors.

The direct sales channel was valued at USD 213.2 million in 2024, captured a 40% share, and is forecast to grow at an 8.6% CAGR through 2034. This channel remains dominant due to the highly specialized nature of fullerene products, which often require tailored specifications, rigorous quality control, and close collaboration between manufacturers and end users such as research organizations, electronics firms, and pharmaceutical companies.

Asia-Pacific Fullerene-Based Specialty Chemicals Market generated USD 255.9 million and held a 48% share in 2024. The region is expected to grow at a 10.2% CAGR during 2025-2034. Strong growth is supported by robust electronics manufacturing capabilities, an extensive chemical supply infrastructure, and active government initiatives promoting nanomaterials and next-generation photovoltaic research. China, Japan, South Korea, and India remain at the forefront of production and innovation, supported by dynamic start-up ecosystems and advanced R&D programs.

Key players operating in the Global Fullerene-Based Specialty Chemicals Market include Nano-C Inc., SES Research Inc., Solaris Chem, TCI (Tokyo Chemical Industry), Sigma-Aldrich / Merck KGaA, American Elements, Strem Chemicals, Ossila, Alfa Aesar (Thermo Fisher), Frontier Carbon Corporation, ACS Material, and Abvigen Inc. Companies in the Fullerene-Based Specialty Chemicals Market are actively investing in research and development to enhance material performance and expand their application base. Strategic collaborations and long-term supply agreements are being formed to strengthen production efficiency and ensure consistent product quality. Several players are diversifying their product portfolios by developing high-purity and functionalized derivatives to meet the evolving needs of advanced electronic and photovoltaic applications. Many firms are also optimizing their distribution networks, focusing on direct partnerships with key end users to provide customized solutions and technical support.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 Distribution Channel trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product format

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 C60 (buckminsterfullerene)

- 5.2.1 95% purity grade

- 5.2.2 99% purity grade

- 5.2.3 99.5% purity grade

- 5.2.4 99.9% purity grade

- 5.3 C70 fullerene

- 5.3.1 Standard grade

- 5.3.2 High purity grade

- 5.4 Functionalized Fullerene Derivatives

- 5.4.1 PCBM ([6,6]-Phenyl-C61-butyric Acid Methyl Ester)

- 5.4.2 ICBA (Indene-C60 Bisadduct)

- 5.4.3 Water-soluble fullerene derivatives

- 5.4.4 Custom functionalized derivatives

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Research & laboratory chemicals

- 6.2.1 Academic & university research

- 6.2.2 Pharmaceutical R&D applications

- 6.2.3 Material science research

- 6.2.4 Government research institutes

- 6.2.5 Commercial research services

- 6.3 Electronics & organic photovoltaics

- 6.3.1 Organic photovoltaic (OPV) applications

- 6.3.2 Semiconductor applications

- 6.3.3 Electronic component integration

- 6.3.4 Display technology applications

- 6.4 Specialty industrial applications

- 6.4.1 Advanced catalyst applications

- 6.4.2 Specialty coatings & materials

- 6.4.3 Tribological applications

- 6.4.4 Niche industrial uses

- 6.5 Contract research & custom synthesis

- 6.5.1 Pharmaceutical contract research

- 6.5.2 Technology company R&D support

- 6.5.3 Custom derivative development

- 6.5.4 Specialized research chemical services

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales (manufacturer to end use)

- 7.3 Chemical distributors

- 7.4 Specialty chemical suppliers

- 7.5 Online chemical marketplaces

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Nano-C Inc.

- 9.2 SES Research Inc.

- 9.3 Solaris Chem

- 9.4 TCI (Tokyo Chemical Industry)

- 9.5 Sigma-Aldrich / Merck KGaA

- 9.6 American Elements

- 9.7 Strem Chemicals

- 9.8 Ossila

- 9.9 Alfa Aesar (Thermo Fisher)

- 9.10 Frontier Carbon Corporation

- 9.11 ACS Material

- 9.12 Abvigen Inc.

(주말 및 공휴일 제외)