|

시장보고서

상품코드

1876625

자동차 영상 신호 프로세서(ISP) 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Image Signal Processor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

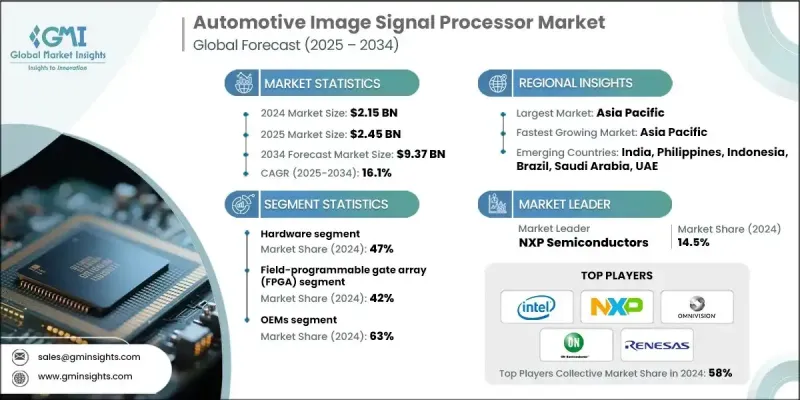

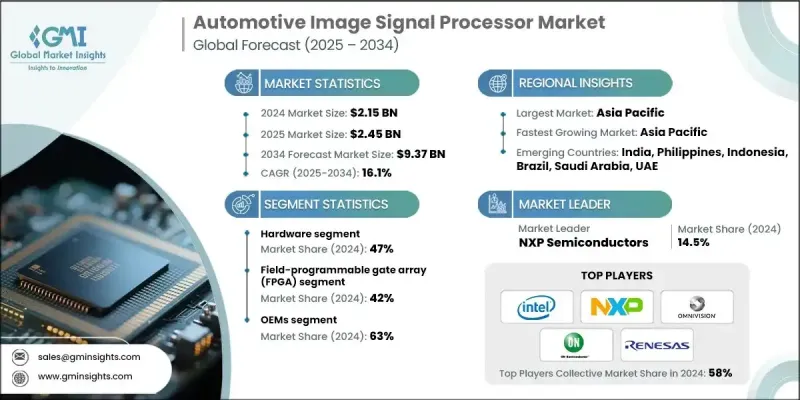

세계의 자동차 영상 신호 프로세서(ISP) 시장은 2024년 21억 5,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 16.1%로 성장할 전망이며, 93억 7,000만 달러에 이를 것으로 예측됩니다.

현대 차량에서의 지능형 영상 기술의 활용 확대는 자동차 ISP 시장 구조를 변화시키고 있습니다. 첨단 ISP는 여러 카메라에서 실시간 이미지 처리를 실현하여 물체 감지, 차선 추적, 360도 뷰 시스템 등의 주요 기능을 지원합니다. 이 프로세서는 엄격한 조명 및 기상 조건에서도 초저지연, 높은 동적 범위, 안정적인 성능을 제공하여 보다 안전하고 에너지 효율적인 차량 운용을 촉진합니다. 자동화 및 소프트웨어 정의 차량 아키텍처로의 지속적인 발전은 고성능 ISP의 통합을 강화하고 있습니다. 반도체 제조업체, 자동차 제조업체, AI 소프트웨어 기업 간의 전략적 제휴도 고급 ADAS(첨단 운전 지원 시스템) 및 지각 시스템을 위한 AI 구동 이미지 처리를 추진하고 있습니다. 칩 제조업체 및 카메라 모듈 공급업체와의 제휴를 통해 중앙 집중식 전자 설계의 열 관리, 화질 및 시스템 통합이 최적화되어 자동차 제조업체는 안전성, 편안함 및 자율주행 수준을 향상시키고 있습니다. 차량이 지능형 이동성 생태계로 이동하는 동안 ISP는 차세대 ADAS 및 자율주행 플랫폼에서 중요한 구성 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 21억 5,000만 달러 |

| 예측 금액 | 93억 7,000만 달러 |

| CAGR | 16.1% |

Field Programmable Gate Array(FPGA) 부문은 2024년에 42%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 14.9%로 성장할 것으로 예측됩니다. FPGA 기반 프로세서는 재구성 가능한 아키텍처, 확장성, 뛰어난 병렬 연산 성능으로 자동차 ISP 시장을 독점하고 있습니다. 이를 통해 자동차 제조업체는 운전자 모니터링, 물체 감지 및 차선 유지와 같은 용도를 위한 고급 이미지 처리 알고리즘을 대규모 하드웨어 재설계 없이 통합할 수 있습니다. 또한 변화하는 카메라와 지각 요건에 대한 적응성으로 시장 투입까지의 시간을 단축할 수 있기 때문에 차세대 ADAS 및 자율주행차의 개발에 필수적인 존재가 되고 있습니다.

2024년 현재 OEM 부문은 63%의 점유율을 차지했습니다. 자동차 제조업체는 생산 공정에서 이러한 프로세서를 신형 차량에 직접 통합하기 위해 자동차 ISP의 주요 채용자입니다. 이를 통해 이미징 시스템이 최적으로 작동하고 안전 규정을 충족하며 신뢰할 수 있는 운영을 실현할 수 있습니다. 자동차 제조업체가 ADAS 기능을 강화하고 운전자 안전을 향상시키기 위해 고해상도 카메라, 센서 퓨전 기술 및 실시간 이미지 분석을 도입함에 따라 공장 출하 시 탑재형 ISP에 대한 선호도가 높아지고 있습니다. 멀티 카메라 구성과 고급 지각 기능의 보급 확대도 세계 OEM의 ISP 채용을 더욱 뒷받침하고 있습니다.

중국의 자동차 영상 신호 프로세서(ISP) 시장은 2024년에 39%의 점유율을 차지했고, 3억 2,490만 달러의 규모가 되었습니다. 이 나라는 강력한 자동차 전자기기 및 반도체 제조 에코시스템을 보유하고 있기 때문에 지역 내에서 지배적인 지위를 유지하고 있습니다. 주요 국내 자동차 제조업체들이 ADAS와 준자율 기술을 급속히 도입하면 ISP에 대한 큰 수요가 이어지고 있습니다. 스마트 차량과 칩 설계 혁신을 촉진하는 정부 지원 프로그램은 시장 성장을 더욱 가속화하고 있습니다. 중국이 반도체 생산과 지능화 모빌리티 솔루션의 국내 발전에 주력하고 있는 것은 자동차용 ISP 분야에 있어서 동국의 리더십을 더욱 강화해 가고 있습니다.

세계 자동차 영상 신호 프로세서(ISP) 시장의 주요 시장 진출 기업으로는 Texas Instruments, ON Semiconductor, Renesas Electronics, Analog Devices, STMicroelectronics, Arm Limited, NXP Semiconductors, Microchip Technology, Intel (Mobileye) 및 OmniVision Technologies 등이 있습니다. 자동차 영상 신호 프로세서(ISP) 시장의 주요 시장 진출 기업은 경쟁 우위를 강화하기 위해 다각적인 전략을 채택하고 있습니다. 많은 기업들이 AI 구동 이미징 기능, 엣지 처리, 실시간 컴퓨터 비전 강화를 ISP 아키텍처에 통합하는 데 주력하고 있습니다. 자동차 제조업체나 소프트웨어 기업과의 제휴에 의해 ADAS(선진 운전 지원 시스템), 자동 운전, 차내 감시에 최적화된 커스텀 ISP 플랫폼의 공동 개발을 진행하고 있습니다. 또한 멀티 센서 융합을 지원하는 저전력 설계, 첨단 열 솔루션, 카메라 동기화 기능 강화를 위한 연구개발 투자가 추진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별 및 국가별

- 기본 추정치 및 계산

- 기준 연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- ADAS 및 자율주행차 개발의 급증

- 고해상도 자동차용 카메라의 보급 확대

- 자동차 안전 규제 강화

- 전기자동차(EV)의 보급 확대 및 스마트 조종석 기능

- 업계의 잠재적 위험 및 과제

- 높은 개발 및 통합 비용

- 소프트웨어 및 센서 교정의 복잡성

- 시장 기회

- 소프트웨어 정의 차량의 등장

- 플릿 및 상용차용 애널리틱스 성장

- 이륜차 및 엔트리 레벨 차량에 도입

- 자동차 제조업체 및 반도체 제조업체 간 제휴

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA 지역

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 가격 동향

- 지역별

- 컴포넌트별

- 비용 내역 분석

- 비즈니스 케이스 및 투자 이익률(ROI) 분석

- 총소유 비용의 틀

- ROI 산출 조사 방법

- 실시 스케줄 및 주요 이정표

- 리스크 평가 및 경감 전략

- 지속가능성 및 환경 영향 분석

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 전망 및 기회

- 기술 진화 및 차세대 ISP 아키텍처

- AI 및 머신러닝의 통합 동향

- 엣지 컴퓨팅 및 분산 처리 모델

3.14.4. 5G 연결성 및 V2X(차량과 모든 것 간의 통신) 통합

- 지속가능성 및 환경 영향에 대한 고려사항

- 규제 진화 및 세계 조화의 동향

- 시장 통합 및 업계 구조의 변화

- 신흥 용도 및 이용 사례의 개발

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 공동 사업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 아날로그 프론트 엔드

- 이미지 센서

- 신호 처리 코어

- 메모리

- 출력 인터페이스

- 소프트웨어

- 서비스

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- ADAS 시스템

- 자율주행차

- 주차 지원, 리어 뷰 및 서라운드 뷰

- 암시 시스템

- 드라이버 감시 시스템

- 기타

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 디지털 신호 처리(DSP)

- 필드 프로그래머블 게이트 어레이(FPGA)

- 특정 애플리케이션용 집적 회로(ASIC)

제8장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 독립형 영상 신호 프로세서

- 통합형 영상 신호 프로세서

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- ARM

- Broadcom

- Cirrus Logic

- Fujitsu

- Infineon Technologies

- Intel(Mobileye)

- Microchip Technology

- Nikon

- NVIDIA

- NXP Semiconductors

- Olympus

- OmniVision Technologies

- Qualcomm Technologies

- Renesas Electronics

- Sony Semiconductor Solutions

- STMicroelectronics

- Texas Instruments

- ON Semiconductor

- Analog Devices

- 지역 기업

- Allwinner Technology

- Amlogic

- HiSilicon Technologies

- MediaTek

- Rockchip Electronics

- 신흥 기업

11.3.1. 10x 엔지니어스

- Cadence Design Systems

- e-con Systems

- Image Quality Labs

- Indie Semiconductor

- Innodisk

- Lattice Semiconductor

- Leopard Imaging

The Global Automotive Image Signal Processor Market was valued at USD 2.15 billion in 2024 and is estimated to grow at a CAGR of 16.1% to reach USD 9.37 billion by 2034.

The rising use of intelligent imaging technologies in modern vehicles is transforming the landscape of automotive ISPs. Advanced ISPs now enable real-time image processing from multiple cameras, supporting key functions such as object detection, lane tracking, and 360-degree view systems. These processors deliver ultra-low latency, high dynamic range, and dependable performance even in challenging lighting and weather conditions, fostering safer and more energy-efficient vehicle operations. The ongoing evolution toward automated and software-defined vehicle architectures is strengthening the integration of high-performance ISPs. Strategic collaborations between semiconductor manufacturers, automakers, and AI software companies are also advancing AI-driven image processing for enhanced driver-assistance and perception systems. Partnerships with chipmakers and camera module suppliers are optimizing thermal management, image quality, and system integration in centralized electronic designs, helping automakers improve safety, comfort, and autonomy levels. As vehicles transition toward intelligent mobility ecosystems, ISPs are becoming critical components in next-generation ADAS and autonomous driving platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.15 Billion |

| Forecast Value | $9.37 Billion |

| CAGR | 16.1% |

The field-programmable gate array (FPGA) segment held a 42% share in 2024 and is anticipated to grow at a CAGR of 14.9% through 2034. FPGA-based processors dominate the automotive ISP market due to their reconfigurable architecture, scalability, and superior parallel computing performance. They enable vehicle manufacturers to integrate advanced image-processing algorithms for applications such as driver monitoring, object detection, and lane-keeping without extensive hardware redesign. Their adaptability to changing camera and perception requirements also reduces time-to-market, making them essential for next-generation ADAS and autonomous vehicle development.

In 2024, the OEMs segment held a 63% share. Original equipment manufacturers are the leading adopters of automotive ISPs because they directly integrate these processors into new vehicle models during production. This ensures that imaging systems perform optimally, meet safety regulations, and deliver reliable operation. The preference for factory-installed ISPs is increasing as automakers deploy high-resolution cameras, sensor-fusion technologies, and real-time image analysis to enhance ADAS capabilities and improve driver safety. The growing use of multi-camera configurations and advanced perception features further supports ISP adoption among global OEMs.

China Automotive Image Signal Processor Market held a 39% share in 2024, generating USD 324.9 million. The country maintains a dominant position in the region due to its strong automotive electronics and semiconductor manufacturing ecosystem. Rapid implementation of ADAS and semi-autonomous technologies by major domestic automakers has fueled significant demand for ISPs. Supportive government programs encouraging innovation in smart vehicles and chip design are further accelerating market growth. China's commitment to advancing local semiconductor production and intelligent mobility solutions continues to reinforce its leadership in the automotive ISP space.

Key industry participants in the Global Automotive Image Signal Processor Market include Texas Instruments, ON Semiconductor, Renesas Electronics, Analog Devices, STMicroelectronics, Arm Limited, NXP Semiconductors, Microchip Technology, Intel (Mobileye), and OmniVision Technologies. Leading players in the Automotive Image Signal Processor Market are adopting multi-faceted strategies to strengthen their competitive positioning. Many are focusing on integrating AI-driven imaging capabilities, edge processing, and real-time computer vision enhancements into their ISP architectures. Companies are forming partnerships with automakers and software firms to co-develop customized ISP platforms optimized for ADAS, autonomous driving, and in-cabin monitoring. R&D investments are being directed toward low-power designs, advanced thermal solutions, and enhanced camera synchronization to support multi-sensor fusion.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Technology

- 2.2.5 End Use

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in ADAS and autonomous vehicle development

- 3.2.1.2 Expansion of high-resolution automotive cameras

- 3.2.1.3 Rise in vehicle safety regulations

- 3.2.1.4 Growing EV adoption and smart cockpit features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Complexity in software and sensor calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of software-defined vehicles

- 3.2.3.2 Growth in fleet and commercial vehicle analytics

- 3.2.3.3 Adoption in two-wheelers and entry-level vehicles

- 3.2.3.4 Collaborations between OEMs and semiconductor firms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Cost breakdown analysis

- 3.11 Business Case & ROI Analysis

- 3.11.1 Total cost of ownership framework

- 3.11.2 ROI calculation methodologies

- 3.11.3 Implementation timeline & milestones

- 3.11.4 Risk assessment & mitigation strategies

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Future outlook & opportunities

- 3.14.1 Technology evolution & next-generation ISP architectures

- 3.14.2 AI & machine learning integration trends

- 3.14.3 Edge computing & distributed processing models

3.14.4. 5G connectivity & vehicle-to-everything (V2X) integration

- 3.14.5 Sustainability & environmental impact considerations

- 3.14.6 Regulatory evolution & global harmonization trends

- 3.14.7 Market consolidation & industry structure changes

- 3.14.8 Emerging applications & use case development

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Analog Front-End

- 5.2.2 Image Sensor

- 5.2.3 Signal Processing Core

- 5.2.4 Memory

- 5.2.5 Output Interface

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ADAS Systems

- 6.3 Autonomous Vehicles

- 6.4 Parking Assistance / Rear-View / Surround View

- 6.5 Night Vision Systems

- 6.6 Driver Monitoring Systems

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Digital signal processing (DSP)

- 7.3 Field-programmable gate array (FPGA)

- 7.4 Application-specific integrated circuits (ASIC)

Chapter 8 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Standalone image signal processors

- 8.3 Integrated image signal processors

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ARM

- 11.1.2 Broadcom

- 11.1.3 Cirrus Logic

- 11.1.4 Fujitsu

- 11.1.5 Infineon Technologies

- 11.1.6 Intel (Mobileye)

- 11.1.7 Microchip Technology

- 11.1.8 Nikon

- 11.1.9 NVIDIA

- 11.1.10 NXP Semiconductors

- 11.1.11 Olympus

- 11.1.12 OmniVision Technologies

- 11.1.13 Qualcomm Technologies

- 11.1.14 Renesas Electronics

- 11.1.15 Sony Semiconductor Solutions

- 11.1.16 STMicroelectronics

- 11.1.17 Texas Instruments

- 11.1.18 ON Semiconductor

- 11.1.19 Analog Devices

- 11.2 Regional Players

- 11.2.1 Allwinner Technology

- 11.2.2 Amlogic

- 11.2.3 HiSilicon Technologies

- 11.2.4 MediaTek

- 11.2.5 Rockchip Electronics

- 11.3 Emerging Players

11.3.1. 10xEngineers

- 11.3.2 Cadence Design Systems

- 11.3.3 e-con Systems

- 11.3.4 Image Quality Labs

- 11.3.5 Indie Semiconductor

- 11.3.6 Innodisk

- 11.3.7 Lattice Semiconductor

- 11.3.8 Leopard Imaging