|

시장보고서

상품코드

1876628

농산물용 포장 장비 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Packaging Equipment for Agricultural Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

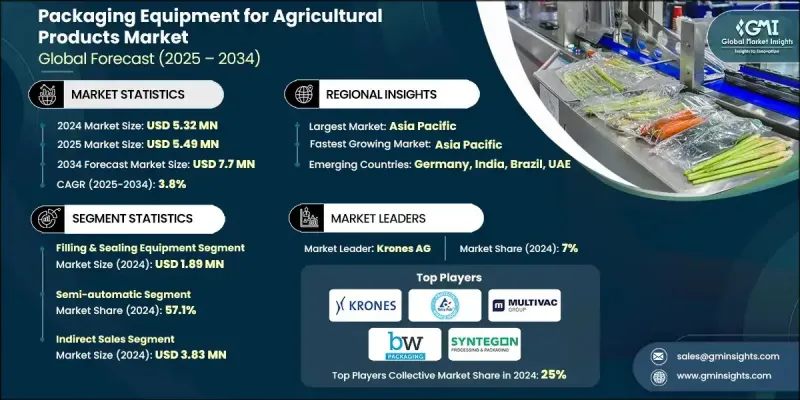

세계의 농산물용 포장 장비 시장은 2024년에 532만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 3.8%로 성장할 전망이며, 770만 달러에 이를 것으로 예측됩니다.

시장 확대는 업무 효율, 정밀도, 생산성을 향상시키는 자동 포장 시스템의 채용 증가에 의해 견인되고 있습니다. 자동화 설비는 충전, 밀봉, 라벨링 등의 공정을 간소화하고, 생산자가 대규모 농업 사업에 있어서 인건비에 대한 의존도를 저감하며, 인적 실수를 최소한으로 억제해, 처리 능력을 가속화하는데 기여하고 있습니다. 실시간 추적 및 데이터 수집을 가능하게 하는 기능을 포함한 스마트 포장 기술의 통합은 큰 부가가치를 가져옵니다. 이러한 기술은 추적성을 강화하고 식품 안전 규정 준수를 지원하며 고급 농산물을 다루는 수출업체 및 공급업체의 재고 관리를 최적화합니다. 품질 보증 및 투명성에 대한 소비자의 기대 고조도 자동화 및 지능화 포장 솔루션의 도입을 촉진하고 있습니다. 세계적으로 식품안전규제가 강화되고 있는 가운데, 생산자는 디지털 감시 및 예지보전 기능을 갖춘 기계에 대한 투자를 확대하고 있습니다. 이러한 마이그레이션은 운영 신뢰성 향상, 데이터 기반 의사결정 개선, 포장 폐기물 감소를 실현합니다. 모듈형 및 IoT 대응 포장 시스템을 개발하는 기업은 이 진화하는 업계 상황에서 경쟁 우위를 얻는 좋은 위치에 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 532만 달러 |

| 예측 금액 | 770만 달러 |

| CAGR | 3.8% |

2024년 반자동 포장기 부문은 57.1%의 점유율을 차지했습니다. 반자동 시스템은 합리적인 가격과 유연성으로 인해 중소규모의 농업 생산자에게 여전히 선호되는 옵션입니다. 이러한 구성은 수작업과 완전 자동화 작업의 균형을 맞추고 기업이 생산 적응성을 유지하면서 인건비를 줄일 수 있도록 도와줍니다. 생산자는 대규모 자본 투자 없이 생산 능력을 확대할 수 있으며 생산 규모 확대를 위한 비용 효율적인 접근 방식을 제공합니다.

간접 판매 채널은 2024년 383만 달러를 창출해 시장의 상당 부분을 차지했습니다. 간접 판매 모델을 통해 제조업체는 지역 리셀러 및 딜러와 제휴할 수 있어 직접 액세스가 어려운 시장으로의 진출이 용이해집니다. 이 접근법은 확립된 리셀러 네트워크가 시장 침투와 현지 농업 관행에 대한 이해를 촉진하는 신흥 지역에서 특히 가치가 있습니다. 이러한 유통 파트너십을 통해 기업은 독립적인 판매 인프라를 구축하지 않고도 고객 기반을 효율적으로 확장할 수 있습니다.

미국의 농산물용 포장 장비 시장은 2024년에 78.2%의 점유율을 차지해 89만 달러의 매출을 계상했습니다. 미국 시장은 선진적인 농업 운영과 지속가능성 및 식품 안전을 촉진하는 정부의 지원 규제에 의해 고도의 성숙도를 나타내고 있습니다. 업계 전체에서 자동화가 널리 도입되고 있으며, 농장 및 가공 시설은 속도, 일관성, 컴플라이언스에 대한 수요 증가에 대응하기 위해 선진적인 충전, 밀봉 및 팔레타이징 설비에 다액의 투자를 실시했습니다.

세계 농산물 포장 장비 시장의 주요 기업은 BW Packaging, Combi Packaging Systems, Concetti Group, General Packer, Haver & Boecker, IMA Group, Krones AG, Landpack, MULTIVAC Group, Paglierani, Premier Tech Systems & Automation, STATEC BINDER, Syntegon Technology, Tetra Pak, WOLF Packaging 등을 들 수 있습니다. 농산물용 포장 장비 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 몇 가지 전략적 노력에 주력하고 있습니다. 많은 기업들이 스마트하고 자동화된 포장 솔루션에 대한 수요 증가에 대응하기 위해 모듈식 IoT 대응 및 에너지 효율적인 시스템 개발을 통해 제품 혁신을 우선시하고 있습니다. 특히 신흥경제국에서는 시장에 대한 리치 및 고객 액세스의 향상을 도모하기 위해, 현지 유통업체이나 지역 딜러와의 제휴를 확대하고 있습니다. 또한 운영 신뢰성을 높이고 가동 중지 시간을 줄이기 위해 디지털 감시 기능 및 예지 보전 기능에 대한 투자를 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동화 및 스마트 포장의 통합

- 농약 및 특수제품에 대한 다각화

- 지속가능성을 중시한 설비 수요

- 업계의 잠재적 리스크 및 과제

- 높은 자본 비용 및 ROI에 대한 압력

- 공급망의 변동성

- 기회

- 스마트 포장 장비

- 친환경 포장 라인

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 기기 유형별(2021-2034년)

- 주요 동향

- 충전 및 밀봉 기기

- 세로형 폼, 필 및 씰(VFFS)

- 수평식 충전 및 밀봉 시스템(HFFS)

- 기타

- 선별 및 등급 구분 기기

- 봉투 포장 및 포장 라인

- 계량 및 분포 시스템

- 팔레타이징 및 랩핑 기기

제6장 시장 추계 및 예측 : 조작별(2021-2034년)

- 주요 동향

- 수동

- 반자동

- 자동식

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 신선한 식품 포장

- 곡물 및 종자 가공

- 사료 및 농업 자재

- 기타(계란, 유제품 포장 등)

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 1차 농업 생산자

- 농업 및 식품 가공 시설

- 기타(농업 협동 조합 및 농업 단체, 농가 소유의 가공 시설 등)

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- BW Packaging

- Combi Packaging Systems

- Concetti Group

- General Packer

- Haver &Boecker

- IMA Group

- Krones AG

- Landpack

- MULTIVAC Group

- Paglierani

- Premier Tech Systems &Automation

- STATEC BINDER

- Syntegon Technology

- Tetra Pak

- WOLF Packaging

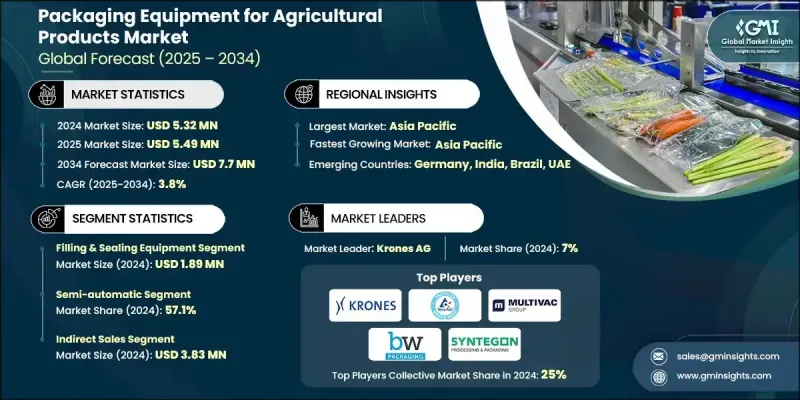

The Global Packaging Equipment for Agricultural Products Market was valued at USD 5.32 million in 2024 and is estimated to grow at a CAGR of 3.8% to reach USD 7.7 million by 2034.

The market's expansion is driven by the increasing adoption of automated packaging systems that enhance operational efficiency, accuracy, and productivity. Automated equipment simplifies processes such as filling, sealing, and labeling, helping producers reduce dependence on manual labor, minimize human error, and accelerate throughput for large-scale agricultural operations. The integration of smart packaging technologies, including features that enable real-time tracking and data collection, is adding significant value. These technologies enhance traceability, support food safety compliance, and optimize inventory management for exporters and suppliers dealing with premium agricultural goods. Rising consumer expectations for quality assurance and transparency are also fueling the adoption of automated and intelligent packaging solutions. As food safety regulations continue to tighten globally, producers are increasingly investing in machinery that offers digital monitoring and predictive maintenance capabilities. This shift enables greater operational reliability, improves data-driven decision-making, and reduces packaging waste. Companies developing modular and IoT-enabled packaging systems are well-positioned to gain a competitive edge in this evolving industry landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.32 Million |

| Forecast Value | $7.7 Million |

| CAGR | 3.8% |

In 2024, the semi-automatic packaging machines segment held a 57.1% share. Semi-automatic systems remain a preferred choice among small and medium agricultural producers due to their affordability and flexibility. These configurations strike a balance between manual and fully automated operations, helping businesses reduce labor costs while maintaining adaptability in production. They allow producers to expand output capacity without requiring major capital investment, offering a cost-efficient approach for scaling production.

The indirect sales channels generated USD 3.83 million in 2024, capturing a substantial portion of the market. Indirect sales models enable manufacturers to collaborate with regional distributors and dealers, making it easier to reach markets that are challenging to access directly. This approach is especially valuable in emerging regions where established distributor networks provide better market penetration and understanding of local agricultural practices. Such distribution partnerships allow companies to grow their customer base efficiently without building independent sales infrastructures.

United States Packaging Equipment for Agricultural Products Market held a 78.2% share and generated USD 0.89 million in 2024. The U.S. market demonstrates high sophistication due to advanced agricultural operations and supportive government regulations promoting sustainability and food safety. Automation is widely implemented across the industry, with farms and processing facilities investing heavily in advanced filling, sealing, and palletizing equipment to meet growing demand for speed, consistency, and compliance.

Key players in the Global Packaging Equipment for Agricultural Products Market include BW Packaging, Combi Packaging Systems, Concetti Group, General Packer, Haver & Boecker, IMA Group, Krones AG, Landpack, MULTIVAC Group, Paglierani, Premier Tech Systems & Automation, STATEC BINDER, Syntegon Technology, Tetra Pak, and WOLF Packaging. Leading companies in the Packaging Equipment for Agricultural Products Market are focusing on several strategic initiatives to strengthen their market position. Many are prioritizing product innovation by developing modular, IoT-enabled, and energy-efficient systems to cater to the growing demand for smart and automated packaging solutions. Partnerships with local distributors and regional dealers are being expanded to enhance market reach and customer accessibility, especially in emerging economies. Firms are also investing in digital monitoring capabilities and predictive maintenance features to boost operational reliability and reduce downtime.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Operation

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Automation & smart packaging integration

- 3.2.1.2 Diversification into agrochemicals & specialty products

- 3.2.1.3 Sustainability-driven equipment demand

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital costs & ROI pressure

- 3.2.2.2 Supply chain volatility

- 3.2.3 Opportunities

- 3.2.3.1 Smart packaging equipment

- 3.2.3.2 Eco-friendly packaging lines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling & sealing equipment

- 5.2.1 Vertical form-fill-seal (VFFS)

- 5.2.2 Horizontal form-fill-seal (HFFS) systems

- 5.2.3 Others

- 5.3 Sorting & grading equipment

- 5.4 Bagging & packaging lines

- 5.5 Weighing and portioning systems

- 5.6 Palletizing and wrapping equipment

Chapter 6 Market Estimates and Forecast, By Operation, 2021 - 2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Fresh produce packaging

- 7.3 Grain & seed processing

- 7.4 Animal feed & agricultural inputs

- 7.5 Others (eggs, dairy pack, etc.)

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Primary agricultural producers

- 8.3 Agro & food processing facilities

- 8.4 Others (agricultural cooperatives & associations, farmer-owned processing facilities, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 BW Packaging

- 11.2 Combi Packaging Systems

- 11.3 Concetti Group

- 11.4 General Packer

- 11.5 Haver & Boecker

- 11.6 IMA Group

- 11.7 Krones AG

- 11.8 Landpack

- 11.9 MULTIVAC Group

- 11.10 Paglierani

- 11.11 Premier Tech Systems & Automation

- 11.12 STATEC BINDER

- 11.13 Syntegon Technology

- 11.14 Tetra Pak

- 11.15 WOLF Packaging