|

시장보고서

상품코드

1876656

800V 전기자동차 아키텍처 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)800V Electric Vehicle Architecture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 800V 전기자동차 아키텍처 시장은 2024년 34억 5,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 21.3%로 성장할 전망이며, 244억 1,000만 달러에 이를 것으로 예측됩니다.

800V 아키텍처의 채용은 보다 빠른 충전, 높은 에너지 효율, 배선 무게 절감, 우수한 열 관리를 실현함으로써 세계 EV 산업을 변화시키고 있습니다. 이러한 고전압 시스템은 배터리, 인버터, 모터 및 차량용 전자 기기를 통합하고 초고속 충전 및 향상된 출력 성능을 지원하므로 차세대 EV에 필수적입니다. OEM 제조업체, 반도체 공급업체, 배터리 제조업체, 파워 일렉트로닉스 기업 간의 투자와 협업이 도입을 가속화하고 있습니다. COVID-19의 팬데믹은 정부와 제조업체들이 지속가능성, 저배출, 비접촉 기술을 우선시함으로써 EV의 보급과 인프라 개발을 더욱 촉진했습니다. 첨단 규제, 강력한 OEM의 존재감, 충전 인프라의 정비 상황에 의해 북미와 유럽이 도입을 리드하고 있습니다. 800V 차량을 지원할 수 있는 초급속 충전 네트워크가 전 세계적으로 확장되어 충전 시간을 몇 시간에서 몇 분으로 단축하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 34억 5,000만 달러 |

| 예측 금액 | 244억 1,000만 달러 |

| CAGR | 21.3% |

승용차 부문은 2024년에 74%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 20.8%로 성장할 것으로 예측됩니다. 이 성장은 항속거리 연장, 급속충전, 에너지 효율 향상을 갖춘 고성능 EV에 대한 소비자 수요에 견인되고 있습니다. 주요 자동차 제조업체는 프리미엄이며 기술적으로 첨단 EV에 대한 선호도를 높이고 가속 성능과 뛰어난 충전 성능을 실현하기 위해 800V 플랫폼의 채택을 확대하고 있습니다.

OEM 부문은 2024년에 63%의 점유율을 차지하였고, 2025-2034년 CAGR 20.4%로 성장할 것으로 전망되고 있습니다. OEM은 효율성, 열 관리 및 충전 속도를 높이기 위해 차세대 EV에 고전압 아키텍처를 신속하게 통합하고 있습니다. 각사는 배선 복잡성의 저감과 에너지 이용의 최적화를 도모하는 독자적인 시스템의 개발에 주력해, 진화하는 EV 시장에서의 경쟁 우위성을 강화하고 있습니다.

중국의 800V 전기자동차 아키텍처 시장은 40%의 점유율을 차지했으며, 2024년에는 5억 3,420만 달러의 규모가 되었습니다. 이 나라의 주도적 입장은 견고한 제조 생태계, 정부 지원 인센티브, 주요 자동차 제조업체의 고전압 플랫폼의 광범위한 채용으로 인한 것입니다. 배터리에서 반도체, 충전 인프라에 이르는 통합 공급망은 대규모 생산과 비용 효율성을 제공합니다. 중국은 초급속 충전 네트워크의 적극적인 확충과 배터리 기술 혁신을 주도하고 있으며, 800V 시스템으로의 이행을 더욱 가속화하고 있습니다.

800V 전기자동차 아키텍처 시장의 주요 기업은 Hyundai Motor Company, Lucid Motors, BYD Company, Kia, Xpeng Motors, BorgWarner, Zeekr Automobile, NIO, Volkswagen 및 Porsche 등을 포함합니다. 이 시장의 기업은 시장 포지션 강화를 위해 여러 전략을 채택하고 있습니다. 고전압 플랫폼 최적화, 열 관리 개선, 배선 복잡성 저감을 위해 연구 개발에 많은 투자를 실시했습니다. 배터리 제조업체, 반도체 공급업체, 인프라 제공업체와의 전략적 제휴 및 협업으로 기술 도입과 생태계 통합이 가속화되고 있습니다. 자동차 제조업체 각사는 또한 초급속 충전 기능을 갖춘 프리미엄으로 고성능 EV 모델의 투입에 주력하여 기술에 익숙한 고객과 성능 중시 고객층의 획득을 도모하고 있습니다. 또한 지리적 확대, 현지 생산, 공급망 최적화로 비용 절감, 확장성 강화, 급성장 시장에서 세계 사업 기반 강화가 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별 및 국가별

- 기본 추정치 및 계산

- 기준 연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 급속 충전 및 항속 거리 연장에 대한 수요 증가

- 고성능 전기차 생산 급증

- 전기자동차(EV)에 대한 정부의 인센티브 및 규제 지원 증가

- OEM 제조업체 및 반도체 공급업체 간의 협력 강화

- 에너지 효율이 뛰어난 프리미엄 EV에 대한 높은 소비자 기호

- 업계의 잠재적 위험 및 과제

- 800V 부품 및 통합의 고비용

- 호환성이 있는 충전 인프라의 한정된 공급

- 시장 기회

- 상용차 및 플릿 EV에서 800V 시스템의 채용 증가

- 차세대 전지 기술에 대한 투자 급증

- 800V 대응의 자율주행차 및 커넥티드카에 대한 수요 증가

- 신흥 경제국의 전기자동차 제조 확대

- 경량화 및 고효율화를 위한 파워 일렉트로닉스 분야의 연구 개발 진전

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 가격 동향

- 지역별

- 컴포넌트별

- 비용 내역 분석

- 지속가능성 및 환경 영향 분석

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 전망 및 기회

- 신흥 용도

- 차세대 혁신

- 투자 기회

- 소비자 수용도 및 시장 준비도

- 총소유비용(TCO) 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 공동 사업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백 자동차

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제6장 시장 추계 및 예측 : 아키텍처별(2021-2034년)

- 주요 동향

- 풀 800V 시스템

- 하이브리드 및 부스트 시스템

제7장 시장 추계 및 예측 : 충전 방식별(2021-2034년)

- 주요 동향

- 초급속 충전(350kW 초과)

- 급속 충전(350kW 미만)

- 표준 충전

제8장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 배터리식 전기자동차(BEV)

- 플러그인 하이브리드 전기자동차(PHEV)

- 연료전지 전기자동차(FCEV)

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 배터리

- 인버터

- 차재 충전기

- 전기 모터

- 배전 모듈

- 기타

제11장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 비공개

- 상용차 및 플릿

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- LAMEA 지역

- 브라질

- 멕시코

- 아르헨티나

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- 세계 기업

- Audi(Volkswagen)

- BMW

- BYD Company

- General Motors Company

- Hyundai Motor

- Kia

- Lucid Motors

- Mercedes-Benz

- NIO

- Porsche

- Xpeng

- 전력 전자 및 반도체 공급업체

- Hitachi

- Infineon Technologies

- ON Semiconductor

- ROHM Semiconductor

- STMicroelectronics

- Wolfspeed

- 충전 인프라 공급업체

- ABB

- ChargePoint

- EVgo

- Tritium DCFC

- 배터리 및 에너지 저장 공급업체

- CATL

- LG Energy Solution

- Panasonic

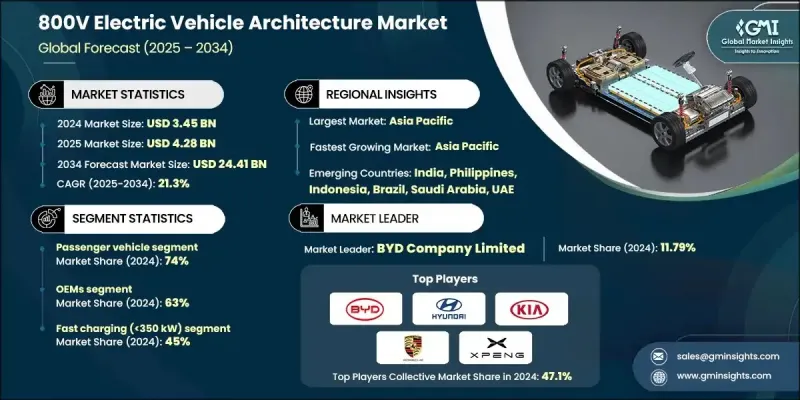

The Global 800V Electric Vehicle Architecture Market was valued at USD 3.45 billion in 2024 and is estimated to grow at a CAGR of 21.3% to reach USD 24.41 billion by 2034.

The adoption of 800V architectures is transforming the global EV industry by enabling faster charging, higher energy efficiency, reduced wiring weight, and superior thermal management. These high-voltage systems integrate batteries, inverters, motors, and onboard electronics to support ultra-fast charging and enhanced power output, making them essential for next-generation EVs. Investments and collaborations among OEMs, semiconductor suppliers, battery manufacturers, and power electronics companies are accelerating their deployment. The COVID-19 pandemic further boosted EV adoption and infrastructure development, as governments and manufacturers prioritized sustainability, low emissions, and contactless technologies. North America and Europe lead adoption due to advanced regulations, strong OEM presence, and charging infrastructure readiness. Ultra-fast charging networks capable of supporting 800V vehicles are expanding worldwide, reducing charging times from hours to minutes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.45 Billion |

| Forecast Value | $24.41 Billion |

| CAGR | 21.3% |

The passenger vehicle segment held a 74% share in 2024 and is forecasted to grow at a 20.8% CAGR through 2034. The growth is driven by consumer demand for high-performance EVs with extended driving ranges, rapid charging, and improved energy efficiency. Leading automakers are increasingly adopting 800V platforms to deliver faster acceleration and superior charging performance, responding to the rising preference for premium and technologically advanced EVs.

The OEM segment accounted for a 63% share in 2024 and is expected to grow at a CAGR of 20.4% from 2025 to 2034. OEMs are rapidly integrating high-voltage architectures into next-generation EVs to improve efficiency, thermal management, and charging speed. Companies are focusing on developing proprietary systems that reduce wiring complexity and optimize energy use, strengthening their competitive edge in the evolving EV market.

China 800V Electric Vehicle Architecture Market held a 40% share, generating USD 534.2 million in 2024. The country's leadership stems from a strong manufacturing ecosystem, government-backed incentives, and widespread adoption of high-voltage platforms by key automakers. Its integrated supply chain, from batteries to semiconductors and charging infrastructure, allows large-scale production and cost efficiency. China is aggressively expanding ultra-fast charging networks and leading innovations in battery technologies, further accelerating the transition to 800V systems.

Major players in the 800V Electric Vehicle Architecture Market include Hyundai Motor Company, Lucid Motors, BYD Company, Kia, Xpeng Motors, BorgWarner, Zeekr Automobile, NIO, Volkswagen, and Porsche. Companies in the 800V Electric Vehicle Architecture Market are adopting multiple strategies to enhance their market position. They are investing heavily in research and development to optimize high-voltage platforms, improve thermal management, and reduce wiring complexity. Strategic partnerships and collaborations with battery manufacturers, semiconductor suppliers, and infrastructure providers are accelerating technology deployment and ecosystem integration. OEMs are also focusing on launching premium, high-performance EV models with ultra-fast charging capabilities to attract tech-savvy and performance-oriented customers. Additionally, geographic expansion, local production, and supply chain optimization are helping companies lower costs, enhance scalability, and strengthen their global footprint in this rapidly growing market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Charging

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Architecture

- 2.2.7 Component

- 2.2.8 End Use

- 2.3 TAM Analysis, 2026-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in demand for faster charging and extended driving range

- 3.2.1.2 Surge in production of high-performance electric vehicles

- 3.2.1.3 Increase in government incentives and regulatory support for EVs

- 3.2.1.4 Growth in collaboration between OEMs and semiconductor suppliers

- 3.2.1.5 Rise in consumer preference for energy-efficient and premium EVs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of 800V components and integration

- 3.2.2.2 Limited availability of compatible charging infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in adoption of 800V systems in commercial and fleet EVs

- 3.2.3.2 Surge in investment toward next-generation battery technologies

- 3.2.3.3 Increase in demand for 800V-ready autonomous and connected vehicles

- 3.2.3.4 Expansion of EV manufacturing in emerging economies

- 3.2.3.5 Growth in R&D toward lightweight, efficient power electronics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.13.1 Emerging Applications

- 3.13.2 Next-Generation Innovations

- 3.13.3 Investment Opportunities

- 3.14 Consumer Adoption & Market Readiness

- 3.15 Total Cost of Ownership (TCO) Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Architecture, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Full 800V System

- 6.3 Hybrid / Boosted System

Chapter 7 Market Estimates & Forecast, By Charging, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Ultra-Fast Charging (>350 kW)

- 7.3 Fast Charging (<350 kW)

- 7.4 Standard Charging

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery electric vehicles (BEVs)

- 8.3 Plug-in hybrid electric vehicles (PHEVs)

- 8.4 Fuel cell electric vehicles (FCEVs)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Battery

- 10.3 Inverter

- 10.4 On-board Charger

- 10.5 Electric Motor

- 10.6 Power Distribution Module

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Private

- 11.3 Commercial/Fleet

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Philippines

- 12.4.7 Indonesia

- 12.5 LAMEA

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 South Africa

- 12.5.5 Saudi Arabia

- 12.5.6 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Audi (Volkswagen)

- 13.1.2 BMW

- 13.1.3 BYD Company

- 13.1.4 General Motors Company

- 13.1.5 Hyundai Motor

- 13.1.6 Kia

- 13.1.7 Lucid Motors

- 13.1.8 Mercedes-Benz

- 13.1.9 NIO

- 13.1.10 Porsche

- 13.1.11 Xpeng

- 13.2 Power Electronics & Semiconductor Suppliers

- 13.2.1 Hitachi

- 13.2.2 Infineon Technologies

- 13.2.3 ON Semiconductor

- 13.2.4 ROHM Semiconductor

- 13.2.5 STMicroelectronics

- 13.2.6 Wolfspeed

- 13.3 Charging Infrastructure Providers

- 13.3.1 ABB

- 13.3.2 ChargePoint

- 13.3.3 EVgo

- 13.3.4 Tritium DCFC

- 13.4 Battery & Energy Storage Suppliers

- 13.4.1 CATL

- 13.4.2 LG Energy Solution

- 13.4.3 Panasonic