|

시장보고서

상품코드

1876791

유전자 합성 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Gene Synthesis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

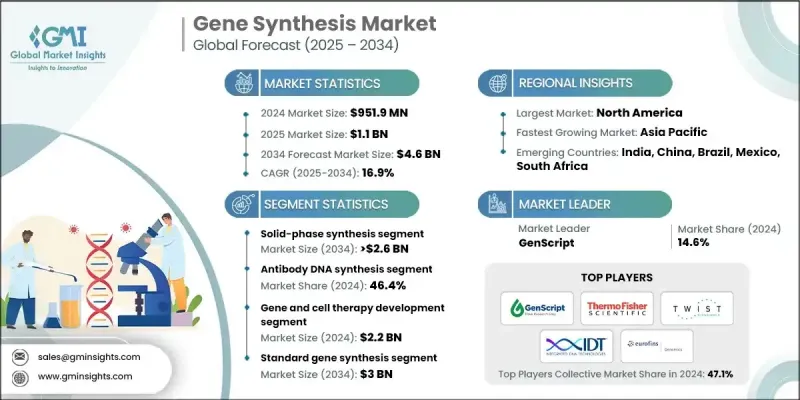

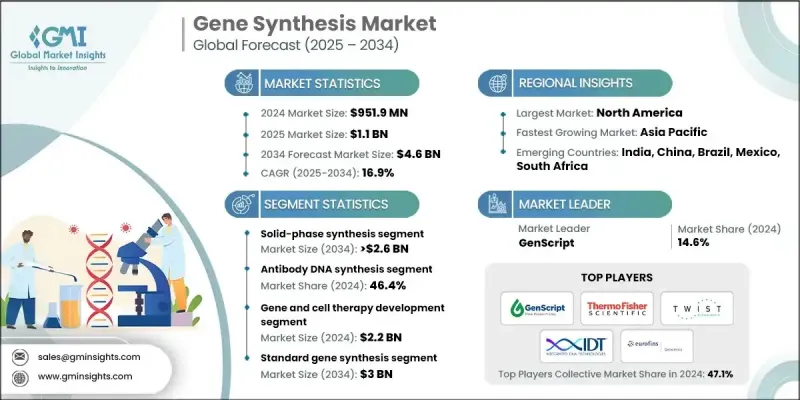

세계의 유전자 합성 시장은 2024년에 9억 5,190만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 16.9%로 성장할 전망이며, 46억 달러에 이를 것으로 예측됩니다.

시장 확대는 합성 생물학의 상승, DNA 합성 기술의 지속적인 진보 및 세계 유전체 연구에 대한 투자 증가로 추진되고 있습니다. 개인화된 의료 및 바이오마커 개발의 확대는 또한 고정밀 유전자 구축 도구에 대한 수요를 높이고 있습니다. 유전자 합성 산업은 맞춤형 유전자 합성, DNA 라이브러리 구축 및 고급 복제 서비스를 제공함으로써 제약 기업, 생명 공학 기업, 학술 연구 기관 및 의료 기술 개발자에게 필수적인 솔루션을 제공합니다. 이 솔루션은 유전 공학 워크 플로우, 창약 연구 및 분자 진단의 효율성을 향상시킵니다. 자동화된 합성 플랫폼과 첨단 오류 보정 기술을 통해 정밀도가 향상되는 동시에 비용과 소요 시간을 줄이고 유전자 합성을 널리 사용할 수 있게 되었습니다. 대규모 유전체학 계획에 대한 정부 및 민간 자금 증가는 질병 모델링, 농업 및 산업용 생명 공학 분야에서의 용도를 지원합니다. 항체 공학, 백신 개발, 치료제 설계에 있어서 합성 유전자의 이용 확대가 업계의 발전을 더욱 추진하고 있습니다. 유행 이후의 상황은 치료제 혁신의 가속화를 향한 신속한 합성 유전자 생산의 중요성을 더욱 견고하게 만듭니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 9억 5,190만 달러 |

| 예측 금액 | 46억 달러 |

| CAGR | 16.9% |

고상 합성 부문은 2024년에 58.6%의 점유율을 차지했으며, 2024년 확장성, 고정밀도, 조사 및 상업적 용도 모두에서 긴 DNA 서열 생성에 적합합니다. 단계적인 뉴클레오티드 부가법은 신뢰성과 정제 효율을 높여 선호되는 합성 기술이 되고 있습니다.

항체 DNA 합성 부문은 2024년에 46.4%의 점유율을 차지했으며, 예측 기간 동안 22억 달러에 달할 것으로 전망되고 있습니다. 암 치료, 면역계 질환, 감염증, 각종 희귀질환에 이용되는 단일클론항체 요법 수요 증가가 성장을 견인하고 있습니다. 이러한 수요가 급증함에 따라 치료 개발 파이프라인을 가속화하기 위한 맞춤형 설계 항체 유전자의 필요성이 증가하고 있습니다.

북미의 유전자 합성 시장은 2024년 40.3%의 점유율을 차지했습니다. 이 지역의 주도적 지위는 주요 생명 공학 및 제약 기업, 강력한 연구 생태계, 유전체학 및 합성 생물학에 대한 엄청난 투자로 지원됩니다. 지원 규제 구조와 고급 임상 연구 능력은 유전자 합성 기술의 채택을 지속적으로 촉진하고 있습니다.

세계의 유전자 합성 시장에 참여하는 주요 기업으로는 Azenta, Inc. (GENEWIZ), BIOMATIK, Bio Basic Inc., BIONEER CORPORATION, Gene Universal Inc., Eurofins Scientific SE, Integrated DNA Technologies, Inc., GenScript, Macrogen, Inc., ProMab Biotechnologies, Inc., OriGene Technologies, Inc., ProteoGenix, Synbio Technologies, Thermo Fisher Scientific Inc. 및 Twist Bioscience Corporation 등이 있습니다. 유전자 합성 시장의 기업은 자동화 합성 플랫폼의 규모 확대, 에러 보정 능력 향상, 커스텀 유전자 설계 서비스의 확충에 의해 경쟁력을 강화하고 있습니다. 많은 기업들이 제약회사 및 생명공학 기업과 전략적 제휴를 맺고 합성 기술을 창약과 항체 설계 워크플로우에 직접 통합하는 움직임을 볼 수 있습니다. 높은 처리량 시스템 및 클라우드 기반 배열 설계 툴에 투자함으로써 프로젝트의 신속한 수행과 대량 처리 능력의 향상이 가능해지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- DNA 합성 기술의 급속한 진보

- 유전자 합성 프로젝트 및 합성 생물학 연구 개발에 대한 투자 확대

- 유전성 질환 및 만성 질환의 유병률 증가

- 유전자 치료의 도입 확대

- 업계의 잠재적 위험 및 과제

- 숙련된 전문가의 부족

- 복잡한 유전자 합성 기술 및 높은 공정 비용

- 시장 기회

- CRISPR 기반 유전자 편집 기술의 용도 범위 확대

- RNA 기반 백신 및 치료제 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 동향

- 현재의 기술 동향

- 신흥 기술 및 그 영향

- 장래 시장 동향

- 가격 분석

- 투자 및 자금 조달 환경

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신서비스의 개시

- 확대 계획

제5장 시장 추계 및 예측 : 방법별(2021-2034년)

- 주요 동향

- 고상 합성

- PCR 기반 효소 합성

- 칩 베이스 합성

제6장 시장 추계 및 예측 : 서비스별(2021-2034년)

- 주요 동향

- 항체 DNA 합성

- 바이러스 DNA 합성

- 기타 서비스

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 유전자 및 세포 치료의 개발

- 질병 진단

- 백신 개발

- 기타 용도

제8장 시장 추계 및 예측 : 복잡도별(2021-2034년)

- 주요 동향

- 표준 유전자 합성

- 복잡한 유전자 합성

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 바이오의약품기업

- 학술연구기관

- 수탁연구기관

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Azenta, Inc.(GENEWIZ)

- Bio Basic Inc.

- BIOMATIK

- BIONEER CORPORATION

- Eurofins Scientific SE

- Gene Universal Inc.

- GenScript

- Integrated DNA Technologies, Inc.

- Macrogen, Inc.

- OriGene Technologies, Inc.

- ProMab Biotechnologies, Inc.

- ProteoGenix

- Synbio Technologies

- Thermo Fisher Scientific Inc.

- Twist Bioscience Corporation

The Global Gene Synthesis Market was valued at USD 951.9 million in 2024 and is estimated to grow at a CAGR of 16.9% to reach USD 4.6 billion by 2034.

Market expansion is propelled by the rise of synthetic biology, continual progress in DNA synthesis technologies, and growing investments in genomics research worldwide. The expanding use of personalized medicine and biomarker development is also increasing the demand for high-precision gene construction tools. The gene synthesis industry provides essential solutions for pharmaceutical companies, biotechnology firms, academic research centers, and healthcare technology developers by offering custom gene synthesis, DNA library creation, and advanced cloning services. These solutions improve the efficiency of genetic engineering workflows, drug discovery studies, and molecular diagnostics. Automated synthesis platforms and sophisticated error-correction technologies have enhanced accuracy while reducing cost and turnaround time, making gene synthesis widely accessible. Increased government and private funding for large-scale genomics initiatives supports applications in disease modeling, agriculture, and industrial biotechnology. Growing utilization of synthetic genes in antibody engineering, vaccine development, and therapeutic design continues to push the industry forward. The post-pandemic landscape has further reinforced the importance of rapid synthetic gene production for accelerated therapeutic innovation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $951.9 Million |

| Forecast Value | $4.6 Billion |

| CAGR | 16.9% |

The solid-phase synthesis segment held 58.6% share in 2024, driven by its scalability, high precision, and suitability for generating long DNA sequences for both research and commercial use. Its stepwise nucleotide addition method enhances reliability and purification efficiency, making it a preferred synthesis technique.

The antibody DNA synthesis segment accounted for a 46.4% share in 2024 and is projected to reach USD 2.2 billion during the forecast period. Growth is driven by rising demand for monoclonal antibody therapies used across cancer treatment, immune system disorders, infectious diseases, and various rare conditions. This surge has increased the need for custom-designed antibody genes to accelerate therapeutic development pipelines.

North America Gene Synthesis Market held a 40.3% share in 2024. The region's leadership is supported by major biotechnology and pharmaceutical companies, strong research ecosystems, and significant investment in genomics and synthetic biology. Supportive regulatory structures and advanced clinical research capabilities continue to elevate the adoption of gene synthesis technologies.

Prominent companies participating in the Global Gene Synthesis Market include Azenta, Inc. (GENEWIZ), BIOMATIK, Bio Basic Inc., BIONEER CORPORATION, Gene Universal Inc., Eurofins Scientific SE, Integrated DNA Technologies, Inc., GenScript, Macrogen, Inc., ProMab Biotechnologies, Inc., OriGene Technologies, Inc., ProteoGenix, Synbio Technologies, Thermo Fisher Scientific Inc., and Twist Bioscience Corporation. Companies in the Gene Synthesis Market are strengthening their competitive position by scaling up automated synthesis platforms, improving error-correction capabilities, and expanding their custom gene design services. Many firms are forming strategic partnerships with pharmaceutical and biotechnology companies to integrate synthesis technologies directly into drug discovery and antibody engineering workflows. Investments in high-throughput systems and cloud-based sequence design tools are enabling faster project turnaround and greater volume capacity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Method trends

- 2.2.3 Services trends

- 2.2.4 Application trends

- 2.2.5 Complexity trends

- 2.2.6 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid advancements in DNA synthesis technology

- 3.2.1.2 Growing investments in gene synthesis projects and synthetic biology R&D

- 3.2.1.3 Increased prevalence of genetic disorders and chronic disease

- 3.2.1.4 Rising adoption of gene therapy

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Complex gene synthesis techniques and high process cost

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of CRISPR-based gene editing applications

- 3.2.3.2 RNA-based vaccines and therapeutics development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies and their impacts

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Investment and funding landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Method, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Solid-phase synthesis

- 5.3 PCR-based enzyme synthesis

- 5.4 Chip-based synthesis

Chapter 6 Market Estimates and Forecast, By Services, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Antibody DNA synthesis

- 6.3 Viral DNA synthesis

- 6.4 Other services

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Gene and cell therapy development

- 7.3 Disease diagnosis

- 7.4 Vaccine development

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Complexity, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Standard gene synthesis

- 8.3 Complex gene synthesis

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Biopharmaceutical companies

- 9.3 Academic and research institutes

- 9.4 Contract research organizations

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Azenta, Inc. (GENEWIZ)

- 11.2 Bio Basic Inc.

- 11.3 BIOMATIK

- 11.4 BIONEER CORPORATION

- 11.5 Eurofins Scientific SE

- 11.6 Gene Universal Inc.

- 11.7 GenScript

- 11.8 Integrated DNA Technologies, Inc.

- 11.9 Macrogen, Inc.

- 11.10 OriGene Technologies, Inc.

- 11.11 ProMab Biotechnologies, Inc.

- 11.12 ProteoGenix

- 11.13 Synbio Technologies

- 11.14 Thermo Fisher Scientific Inc.

- 11.15 Twist Bioscience Corporation