|

시장보고서

상품코드

1876806

재활용 열가소성 플라스틱 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Recycled Thermoplastic Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 재활용 열가소성 플라스틱 시장은 2024년에 375억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 9.3%로 성장하여 920억 달러에 이를 것으로 예측됩니다.

본 시장에서는 화학적 탈중합, 효소 재활용, 플라즈마 처리, 마이크로파 보조법 등 첨단 재활용 기술이 빠르게 보급되고 있습니다. 이러한 기술을 통해 혼합, 오염, 다층 플라스틱을 고품질 재생 폴리머로 전환하여 버진 소재의 기준을 충족시킬 수 있습니다. 순환경제 원칙의 확산, 소비자 인식의 변화, 재활용 의무화 및 일회용 플라스틱 규제 등 강력한 정부 정책이 수요를 견인하고 있습니다. 폐쇄형 루프 시스템과 재활용 인프라에 대한 투자 확대로 재활용 열가소성 플라스틱공급량은 더욱 증가하고 있습니다. 자동차, 포장, 전자 산업이 주요 최종 사용자로서 지속 가능한 제조를 위해 이러한 소재를 활용하고 있습니다. 친환경 생산과 고부가가치 용도에 대한 관심이 높아짐에 따라 향후 10년간 시장은 안정적인 성장을 유지할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 375억 달러 |

| 예측 금액 | 920억 달러 |

| CAGR | 9.3% |

첨단 및 하이브리드 재활용 기술 부문은 연평균 성장률(CAGR)로 성장할 것으로 예측됩니다. 세계 재활용 열가소성 플라스틱 시장은 2024년 375억 달러로 평가되었고, 2034년까지 연평균 9.3% 성장하여 920억 달러에 이를 것으로 예측됩니다.

본 시장에서는 화학적 탈중합, 효소 재활용, 플라즈마 처리, 마이크로파 보조법 등 첨단 재활용 기술이 빠르게 보급되고 있습니다. 이러한 기술을 통해 혼합, 오염, 다층 플라스틱을 고품질 재생 폴리머로 전환하여 새로운 소재의 기준을 충족시킬 수 있습니다. 순환경제 원칙의 확산, 소비자 인식의 변화, 재활용 소재의 최소 함량 의무화 및 일회용 플라스틱 규제 등 강력한 정부 정책이 수요를 견인하고 있습니다. 폐쇄형 루프 시스템과 재활용 인프라에 대한 투자 확대로 재활용 열가소성 플라스틱공급량은 더욱 증가하고 있습니다. 자동차, 포장, 전자 산업이 주요 최종 사용자로서 지속 가능한 제조를 위해 이러한 소재를 활용하고 있습니다. 친환경 생산과 고부가가치 용도에 대한 관심이 높아짐에 따라 향후 10년간 시장은 안정적인 성장을 유지할 것으로 예측됩니다.

첨단 재활용 기술 및 하이브리드 재활용 기술 부문은 2034년까지 연평균 복합 성장률(CAGR) 9.8%를 보일 것으로 예측됩니다. 이 기술은 복잡하고 처리하기 어려운 플라스틱 폐기물을 재활용할 수 있게 하고, 탄소 발자국을 최소화하며, 고급 용도에 적합한 고성능 폴리머를 생산할 수 있습니다.

2024년 폴리에틸렌 테레프탈레이트(PET)는 식수병, 포장재, 재생 PET(rPET) 섬유 응용 분야로 인해 131억 달러 시장 규모를 차지했습니다. PET 재활용은 높은 재생성과 다재다능함으로 인해, 특히 식품용 및 섬유용도에서 지속적으로 확대되고 있습니다.

미국의 재활용 열가소성 수지 시장은 고도의 재활용 인프라와 선별 및 회수 공정의 개선으로 2024년 94억 달러 규모에 달했습니다. 미국과 캐나다는 모두 원료 회수율과 재료 품질 향상을 위해 기계적 재활용과 화학적 재활용에 많은 투자를 하고 있습니다. 주요 수요는 포장, 자동차, 전자기기 분야에서 발생하며, 폐쇄형 루프 시스템과 순환 경제에 대한 노력이 점점 더 강조되고 있습니다.

세계 재활용 열가소성 수지 시장의 주요 기업으로는 PreZero Polymers AG,Veolia Environmental Services,Eastman Chemical Company,KW Plastics Manufacturing,Loop Industries Inc.,Republic Services Inc.,Carbios SA,Lyondell Basell,Biffa plc,Remondis Recycling GmbH,Plastipak Holdings Inc. amp;&Recovery,Avient Corporation,Clear Path Recycling,Indorama Ventures Public Company Limited 등이 있습니다. 재활용 열가소성 수지 시장의 기업들은 시장에서의 입지를 강화하고 사업 범위를 확대하기 위해 여러 가지 전략을 채택하고 있습니다. 여기에는 폴리머 품질 향상을 위한 첨단 화학적, 기계적 재활용 기술에 대한 투자, 처리 능력 확대, 안정적인 원료 공급을 위한 원료 공급업체와의 제휴 등이 포함됩니다. 많은 기업들이 고급 최종 용도에 대응하기 위해 폐쇄형 루프 시스템과 고성능 재생 폴리머 개발에 집중하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 가공 방법별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- LATAM

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 처리 방법별, 2021-2034

- 주요 동향

- 기계적 재활용

- 수집 및 선별 시스템

- 세정 및 청정화 프로세스

- 파쇄 및 사이즈 축소

- 용해 및 펠릿화

- 화학적 재활용

- 열분해 기술

- 탈중합 프로세스

- 가스화법

- 용해 분해 기술

- 촉매 분해

- 효소 분해에 의한 탈중합

- 첨단 기술

- 바이오 재활용 방법

- 플라즈마 기반 기술

- 마이크로파 강화 처리

- 기타 신기술

제6장 시장 추산·예측 : 제품 유형별, 2021-2034

- 주요 동향

- PET

- HDPE

- LDPE

- PP

- PS

- 기타

제7장 시장 추산·예측 : 용도별, 2021-2034

- 주요 동향

- 포장

- 식품 및 음료 용기

- 비식품 포장

- 연포장 및 필름

- 뚜껑 및 마개

- 자동차 및 운송

- 내장 부품

- 보닛내 용도

- 외장 패널 및 트림

- 배터리 하우징 및 EV 부품

- 건축 및 건설

- 파이프 및 피팅

- 단열재

- 지붕재 및 데크재

- 창문 프로파일

- 전자 및 전기 기기

- 디바이스 케이스

- 커넥터 및 부품

- 케이블 절연재

- 소비재 및 가구

- 가정용품

- 야외 용가구

- 완구 및 스포츠 용품

- 농업 및 원예

- 온실용 필름

- 관개 시스템

- 화분 및 컨테이너

- 섬유 및 의류

- 합성 섬유

- 카펫 및 바닥재

- 부직포

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- Avient Corporation

- Biffa plc

- Carbios SA

- Clear Path Recycling

- Eastman Chemical Company

- Indorama Ventures Public Company Limited

- KW Plastics Manufacturing

- Loop Industries Inc.

- Lyondell Basell

- Plastipak Holdings Inc.

- PreZero Polymers AG

- Remondis Recycling GmbH

- Republic Services Inc.

- SUEZ Recycling &Recovery

- Veolia Environmental Services

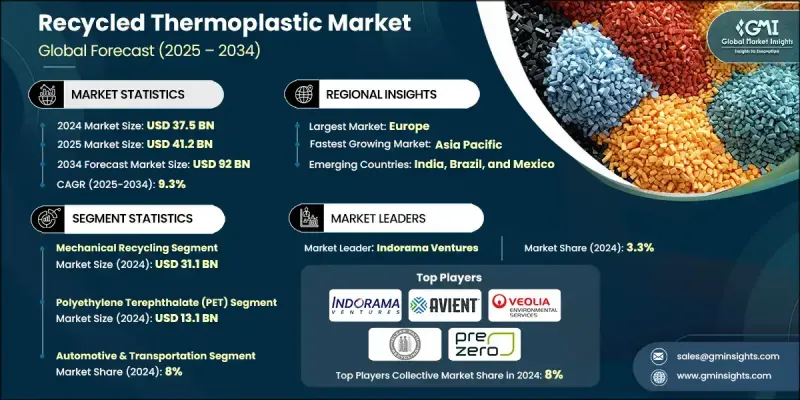

The Global Recycled Thermoplastic Market was valued at USD 37.5 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 92 billion by 2034.

The market is witnessing rapid adoption of advanced recycling technologies such as chemical depolymerization, enzymatic recycling, plasma processing, and microwave-assisted methods. These techniques enable the transformation of mixed, contaminated, and multilayer plastics into high-quality recycled polymers that meet the standards of virgin materials. Rising adoption of circular economy principles, growing consumer awareness, and strong government policies mandating minimum recycled content and restricting single-use plastics are fueling demand. Closed-loop systems and increased investments in recycling infrastructure are further enhancing the availability of recycled thermoplastics. The automotive, packaging, and electronics industries are among the primary end-users, leveraging these materials for sustainable manufacturing. Rising emphasis on eco-efficient production and high-value applications is expected to sustain consistent growth in the market over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.5 Billion |

| Forecast Value | $92 Billion |

| CAGR | 9.3% |

The advanced and hybrid recycling technologies segment is projected to grow at a CAGR The Global Recycled Thermoplastic Market was valued at USD 37.5 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 92 billion by 2034.

The market is witnessing rapid adoption of advanced recycling technologies such as chemical depolymerization, enzymatic recycling, plasma processing, and microwave-assisted methods. These techniques enable the transformation of mixed, contaminated, and multilayer plastics into high-quality recycled polymers that meet the standards of virgin materials. Rising adoption of circular economy principles, growing consumer awareness, and strong government policies mandating minimum recycled content and restricting single-use plastics are fueling demand. Closed-loop systems and increased investments in recycling infrastructure are further enhancing the availability of recycled thermoplastics. The automotive, packaging, and electronics industries are among the primary end-users, leveraging these materials for sustainable manufacturing. Rising emphasis on eco-efficient production and high-value applications is expected to sustain consistent growth in the market over the coming decade.

The advanced and hybrid recycling technologies segment is projected to grow at a CAGR of 9.8% through 2034. These methods can recycle complex and hard-to-process plastic waste streams while minimizing carbon footprint, producing high-performance polymers suitable for premium applications.

In 2024, the polyethylene Terephthalate (PET) accounted for USD 13.1 billion, driven by its use in beverage bottles, packaging, and recycled PET (rPET) fibers. PET recycling continues to expand, particularly for food-grade and textile applications, due to its high recyclability and versatility.

U.S. Recycled Thermoplastic Market reached USD 9.4 billion in 2024, supported by advanced recycling infrastructure and improved sorting and collection processes. Both the U.S. and Canada are investing heavily in mechanical and chemical recycling to enhance feedstock recovery and material quality. Key demand stems from the packaging, automotive, and electronics sectors, with increasing focus on closed-loop systems and circular economy initiatives.

Leading players in the Global Recycled Thermoplastic Market include PreZero Polymers AG, Veolia Environmental Services, Eastman Chemical Company, KW Plastics Manufacturing, Loop Industries Inc., Republic Services Inc., Carbios SA, Lyondell Basell, Biffa plc, Remondis Recycling GmbH, Plastipak Holdings Inc., SUEZ Recycling & Recovery, Avient Corporation, Clear Path Recycling, and Indorama Ventures Public Company Limited. Companies in the Recycled Thermoplastic Market are employing multiple strategies to enhance their market position and expand their reach. These include investing in advanced chemical and mechanical recycling technologies to improve polymer quality, expanding processing capacity, and establishing partnerships with feedstock suppliers to secure consistent input. Many players are focusing on developing closed-loop systems and high-performance recycled polymers to cater to premium end-use applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Processing method

- 2.2.3 Product type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa (MEA)

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By processing method

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Processing Method, 2021-2034 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Mechanical recycling

- 5.2.1 Collection & sorting systems

- 5.2.2 Washing & cleaning processes

- 5.2.3 Shredding & size reduction

- 5.2.4 Melting & pelletizing

- 5.3 Chemical recycling

- 5.3.1 Pyrolysis technologies

- 5.3.2 Depolymerization processes

- 5.3.3 Gasification methods

- 5.3.4 Solvolysis techniques

- 5.3.5 Catalytic cracking

- 5.3.6 Enzymatic depolymerization

- 5.4 Advanced technologies

- 5.4.1 Bio based recycling methods

- 5.4.2 Plasma based technologies

- 5.4.3 Microwave enhanced processing

- 5.4.4 Other emerging technologies

Chapter 6 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 PET

- 6.3 HDPE

- 6.4 LDPE

- 6.5 PP

- 6.6 PS

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.2.1 Food & beverage containers

- 7.2.2 Non-food packaging

- 7.2.3 Flexible packaging & films

- 7.2.4 Caps & closures

- 7.3 Automotive & transportation

- 7.3.1 Interior components

- 7.3.2 Under-hood applications

- 7.3.3 Exterior panels & trim

- 7.3.4 Battery housing & EV components

- 7.4 Building & construction

- 7.4.1 Pipes & fittings

- 7.4.2 Insulation materials

- 7.4.3 Roofing & decking

- 7.4.4 Window profiles

- 7.5 Electronics & electrical

- 7.5.1 Device housings

- 7.5.2 Connectors & components

- 7.5.3 Cable insulation

- 7.6 Consumer goods & furniture

- 7.6.1 Household items

- 7.6.2 Outdoor furniture

- 7.6.3 Toys & sporting goods

- 7.7 Agriculture & horticulture

- 7.7.1 Greenhouse films

- 7.7.2 Irrigation systems

- 7.7.3 Plant pots & containers

- 7.8 Textiles & apparel

- 7.8.1 Synthetic fibers

- 7.8.2 Carpeting & flooring

- 7.8.3 Non-woven fabrics

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Avient Corporation

- 9.2 Biffa plc

- 9.3 Carbios SA

- 9.4 Clear Path Recycling

- 9.5 Eastman Chemical Company

- 9.6 Indorama Ventures Public Company Limited

- 9.7 KW Plastics Manufacturing

- 9.8 Loop Industries Inc.

- 9.9 Lyondell Basell

- 9.10 Plastipak Holdings Inc.

- 9.11 PreZero Polymers AG

- 9.12 Remondis Recycling GmbH

- 9.13 Republic Services Inc.

- 9.14 SUEZ Recycling & Recovery

- 9.15 Veolia Environmental Services