|

시장보고서

상품코드

1876808

슬관절 전치환술 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Total Knee Replacement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

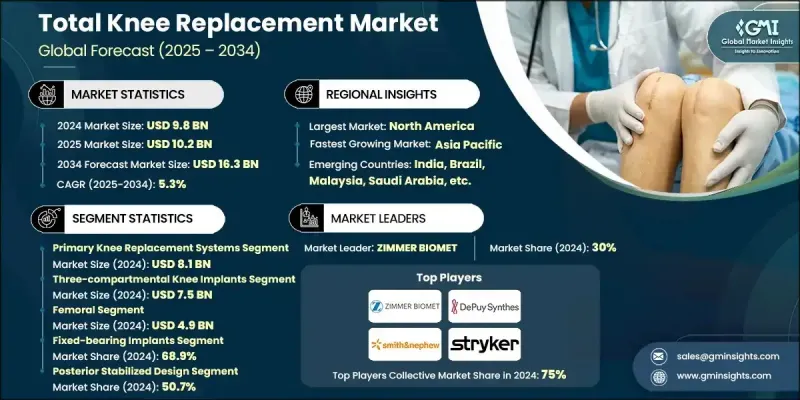

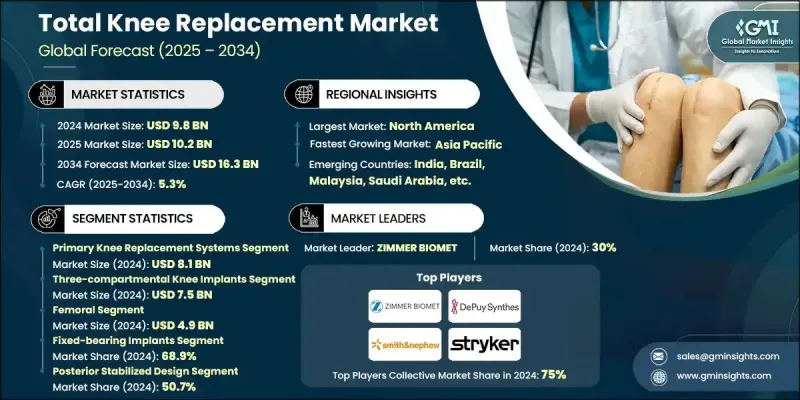

세계의 슬관절 전치환술 시장은 2024년에 98억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.3%로 성장하여 163억 달러에 이를 것으로 예측됩니다.

시장 성장은 골관절염과 골다공증의 유병률 증가, 재수술이 필요한 관절 감염 증가율, 수술 기술의 지속적인 발전으로 인해 크게 견인되고 있습니다. 외래수술센터 및 당일수술센터의 확대는 수술 접근성 향상에 더욱 기여하고 있습니다. 퇴행성 관절질환은 특히 노년층에서 이동성을 저하시키고 만성 통증을 유발하기 때문에 기능 회복과 삶의 질 향상을 목적으로 하는 무릎 인공관절 전치환술에 대한 수요를 촉진하고 있습니다. 외과 의사와 의료기기 제조업체들은 첨단 영상 진단 기술과 디지털 계획 도구를 활용한 혁신적인 임플란트 설계와 환자 맞춤형 솔루션으로 이에 대응하고 있습니다. 이러한 기술은 임플란트의 적합성, 편안함, 장기적인 성능을 향상시키는 동시에 수술 후 합병증을 감소시킵니다. 또한, 정밀하게 설계된 맞춤형 임플란트에 대한 수요가 증가함에 따라 제조업체들은 환자의 고유한 해부학적 요구 사항을 충족하고 회복 결과를 최적화하는 솔루션을 개발할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 98억 달러 |

| 예측 금액 | 163억 달러 |

| CAGR | 5.3% |

1차 무릎관절 치환술 분야는 2024년 81억 달러 시장 규모를 형성했습니다. 비만율 증가, 스마트 임플란트 기술 채택, 3D 프린팅 기술 혁신이 이 분야를 주도하고 있습니다. 임상적 신뢰성과 장기적인 내구성으로 인해 1차 슬관절 치환술은 여전히 1차적 무릎 관절 치환술이 가장 선호되는 수술법입니다.

삼실형 무릎 관절 임플란트 부문은 2024년 75억 달러 시장 규모를 형성했습니다. 이 임플란트는 무릎의 세 개의 관절실을 모두 재표면화하도록 설계되어 광범위한 관절 퇴행이 있는 환자에게 광범위하게 권장되며, 종합적인 관절 수복물을 제공합니다.

북미 전체 무릎 관절 치환술 시장은 2024년 54.1%의 점유율을 차지했습니다. 이 지역의 성장은 첨단 의료 인프라, 고령화 인구, 로봇 보조 수술 및 스마트 임플란트 도입으로 정확성과 재활 결과를 향상시키는 로봇 보조 수술 및 스마트 임플란트 도입에 의해 주도되고 있습니다. 확립된 상환제도로 인해 최소침습수술과 외래 수술이 지원되고 있으며, 이는 시장의 추가 확대를 촉진하고 있습니다.

슬관절 전치환술 시장의 주요 기업으로는 알레그라, 비브라운, 콜린, 데퓨 신세스(존슨앤드존슨), 에노비스, 엑사텍, 메닥터 인터내셔널, 마이크로포트 오소페딕스, 오소 개발, 레스토 3D, 스미스 앤 네퓨, 스트라이커, 발데마르 링크, 지머 바이오메트, 앰플리튜드 등이 있습니다. 스미스 앤 네퓨, 스트라이커, 발데마르 링크, 지머 바이오메트, 앰플리튜드 등이 있습니다. 슬관절 전치환술 시장을 선도하는 주요 기업들은 환자 맞춤형 임플란트 및 차세대 수술 시스템 개발을 위한 연구개발 투자를 강화하며 시장에서의 존재감을 높여가고 있습니다. 많은 기업들이 디지털 계획 기술과 로봇 지원 기술을 접목하여 수술의 정확성과 치료 결과를 향상시키고 있습니다. 병원, 수술센터, 의료기관과의 전략적 제휴를 통해 시장 접근성을 강화하고 제품 도입을 촉진하고 있습니다. 또한, 수요가 많은 지역에 제조시설과 유통망을 구축하여 지리적 확장도 추진하고 있습니다. 스마트 임플란트 및 3D 프린팅 부품의 혁신은 내구성과 기능성을 향상시키기 위한 우선순위 과제입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 기회

- 성장 가능성 분석

- 규제 상황

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 상환 시나리오

- 수술 실패율 및 성공률 상황 개요

- 가격 분석, 2021-2034

- 슬관절 수술 현황

- 측정 절제술

- 인대 균형(Gap balancing technique)

- 균형 사이저

- 측정 사이저

- 환자층 및 역학적 동향

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 향후 시장 동향

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산·예측 : 제품별, 2021-2034

- 주요 동향

- 1차 인공 슬관절 치환 시스템

- 부분 슬관절 치환 시스템

- 재치환용 슬관절 치환 시스템

제6장 시장 추산·예측 : 디바이스 유형별, 2021-2034

- 주요 동향

- Three-compartmental knee implants

- Bicompartmental knee implants

- Unicompartmental knee implants

제7장 시장 추산·예측 : 컴포넌트별, 2021-2034

- 주요 동향

- 대퇴골

- 경골

- 종지뼈

제8장 시장 추산·예측 : 임플란트 유형별, 2021-2034

- 주요 동향

- 고정형 베어링 임플란트

- 이동형 베어링 임플란트

- 내측 피벗 임플란트

- 기타 임플란트 유형

제9장 시장 추산·예측 : 설계별, 2021-2034

- 주요 동향

- 후방 안정화 설계

- 십자 인대 온존형 설계

- 기타 설계

제10장 시장 추산·예측 : 수술 유형별, 2021-2034

- 주요 동향

- 기존 수술

- 기술 지원형 수술 유형

제11장 시장 추산·예측 : 고정 재료별, 2021-2034

- 주요 동향

- 시멘트 고정

- 시멘트리스

- 하이브리드

제12장 시장 추산·예측 : 재료별, 2021-2034

- 주요 동향

- Metal-on-plastic

- Ceramic-on-plastic

- Metal-on-metal

- Ceramic-on-ceramic

제13장 시장 추산·예측 : 폴리에틸렌 인서트별, 2021-2034

- 주요 동향

- 항산화 폴리에틸렌 인서트

- 고도로 가교된 폴리에틸렌 인서트

- 기존 폴리에틸렌 인서트

제14장 시장 추산·예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제15장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 태국

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제16장 기업 개요

- Allegra

- amplitude

- B BRAUN

- Corin

- Depuy Synthes(Johnson &Johnson)

- enovis

- exactech

- Medacta International

- MicroPort Orthopedics

- ORTHO Development

16.11.복원 3 D

- 스미스·앤드·네퓨

- 스트라이커

- 바르데마르·링크

- 지마·바이오멧트

The Global Total Knee Replacement Market was valued at USD 9.8 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 16.3 billion by 2034.

The market's growth is largely fueled by the rising prevalence of osteoarthritis and osteoporosis, increasing rates of joint infections necessitating revisions, and continuous advancements in surgical techniques. The expansion of outpatient and ambulatory surgical centers has further contributed to higher procedure accessibility. Degenerative joint diseases reduce mobility and cause chronic pain, particularly in aging populations, driving the demand for total knee replacement procedures to restore function and improve quality of life. Surgeons and medical device manufacturers are responding with innovative implant designs and patient-specific solutions using advanced imaging and digital planning tools. These technologies enhance implant fit, comfort, and long-term performance while reducing postoperative complications. Additionally, demand for precision-engineered and customizable implants is growing, encouraging manufacturers to develop solutions that meet patient-specific anatomical requirements and optimize recovery outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.8 Billion |

| Forecast Value | $16.3 Billion |

| CAGR | 5.3% |

The primary knee replacement systems segment generated USD 8.1 billion in 2024. Rising obesity rates, the adoption of smart implant technologies, and 3D printing innovations are driving the segment. Primary knee replacements remain the preferred first-line procedure due to their established clinical reliability and long-term durability.

The three-compartmental knee implants segment generated USD 7.5 billion in 2024. These implants are designed to resurface all three compartments of the knee and are widely recommended for patients with extensive joint degeneration, offering comprehensive joint restoration.

North America Total Knee Replacement Market accounted for a 54.1% share in 2024. Growth in the region is driven by advanced healthcare infrastructure, an aging population, and the adoption of robotic-assisted surgery and smart implants that enhance precision and rehabilitation outcomes. Minimally invasive procedures and outpatient surgical care are supported by established reimbursement mechanisms, further encouraging market expansion.

Key companies operating in the Total Knee Replacement Market include Allegra, B BRAUN, Corin, Depuy Synthes (Johnson & Johnson), enovis, Exactech, Medacta International, MicroPort Orthopedics, ORTHO Development, Restor3D, Smith+Nephew, Stryker, Waldemar LINK, ZIMMER BIOMET, and Amplitude. Leading companies in the Total Knee Replacement Market are enhancing their presence by investing in research and development to produce patient-specific implants and next-generation surgical systems. Many are incorporating digital planning and robotic-assisted technologies to improve surgical precision and outcomes. Strategic partnerships with hospitals, surgical centers, and healthcare providers are strengthening market reach and facilitating product adoption. Firms are also expanding geographically by establishing manufacturing facilities and distribution networks in high-demand regions. Innovation in smart implants and 3D-printed components is a priority, supporting improved durability and functionality.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Device type trends

- 2.2.4 Component trends

- 2.2.5 Implant type trends

- 2.2.6 Design trends

- 2.2.7 Surgery type trends

- 2.2.8 Fixation material trends

- 2.2.9 Material trends

- 2.2.10 Polyethylene inserts trends

- 2.2.11 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of arthritis and osteoporosis

- 3.2.1.2 Need for personalized and patient specific implants

- 3.2.1.3 Growing infection rates contributing to rise in knee revisions

- 3.2.1.4 Surging preference for bicruciate-retaining total knee arthroplasty

- 3.2.1.5 Increasing usage of unicondylar knee procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increased number of knee implant recalls

- 3.2.2.2 High cost associated with the surgery

- 3.2.3 Opportunities

- 3.2.3.1 Smart implants and IoT integration

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Procedure failure/success rate landscape

- 3.8 Pricing analysis, 2021-2034

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 MEA

- 3.9 Knee surgery landscape

- 3.9.1 Measured resection technique

- 3.9.2 Gap balancing technique

- 3.9.3 Balanced sizer

- 3.9.4 Measured sizer

- 3.10 Patient demographics and epidemiological trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Primary knee replacement systems

- 5.3 Partial knee replacement systems

- 5.4 Revision knee replacement systems

Chapter 6 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Three-compartmental knee implants

- 6.3 Bicompartmental knee implants

- 6.4 Unicompartmental knee implants

Chapter 7 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Femoral

- 7.3 Tibial

- 7.4 Patellar

Chapter 8 Market Estimates and Forecast, By Implant Type, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 Fixed-bearing implants

- 8.3 Mobile-bearing implants

- 8.4 Medial pivot implants

- 8.5 Other implant types

Chapter 9 Market Estimates and Forecast, By Design, 2021 - 2034 ($ Mn and Units)

- 9.1 Key trends

- 9.2 Posterior stabilized design

- 9.3 Cruciate retaining design

- 9.4 Other designs

Chapter 10 Market Estimates and Forecast, By Surgery Type, 2021 - 2034 ($ Mn and Units)

- 10.1 Key trends

- 10.2 Traditional surgery type

- 10.3 Technology assisted surgery type

Chapter 11 Market Estimates and Forecast, By Fixation Material, 2021 - 2034 ($ Mn and Units)

- 11.1 Key trends

- 11.2 Cemented

- 11.3 Cementless

- 11.4 Hybrid

Chapter 12 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn and Units)

- 12.1 Key trends

- 12.2 Metal-on-plastic

- 12.3 Ceramic-on-plastic

- 12.4 Metal-on-metal

- 12.5 Ceramic-on-ceramic

Chapter 13 Market Estimates and Forecast, By Polyethylene Inserts, 2021 - 2034 ($ Mn and Units)

- 13.1 Key trends

- 13.2 Antioxidant polyethylene inserts

- 13.3 Highly cross-linked polyethylene inserts

- 13.4 Conventional polyethylene inserts

Chapter 14 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn and Units)

- 14.1 Key trends

- 14.2 Hospitals

- 14.3 Ambulatory surgery centers

- 14.4 Other End Use

Chapter 15 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 15.1 Key trends

- 15.2 North America

- 15.2.1 U.S.

- 15.2.2 Canada

- 15.3 Europe

- 15.3.1 Germany

- 15.3.2 UK

- 15.3.3 France

- 15.3.4 Spain

- 15.3.5 Italy

- 15.3.6 Netherlands

- 15.4 Asia Pacific

- 15.4.1 China

- 15.4.2 Japan

- 15.4.3 India

- 15.4.4 Australia

- 15.4.5 South Korea

- 15.4.6 Thailand

- 15.4.7 Malaysia

- 15.5 Latin America

- 15.5.1 Brazil

- 15.5.2 Mexico

- 15.5.3 Argentina

- 15.6 MEA

- 15.6.1 South Africa

- 15.6.2 Saudi Arabia

- 15.6.3 UAE

Chapter 16 Company Profiles

- 16.1 Allegra

- 16.2 amplitude

- 16.3 B BRAUN

- 16.4 Corin

- 16.5 Depuy Synthes (Johnson & Johnson)

- 16.6 enovis

- 16.7 exactech

- 16.8 Medacta International

- 16.9 MicroPort Orthopedics

- 16.10 ORTHO Development

16.11. restor3 d

- 16.12 Smith+Nephew

- 16.13 stryker

- 16.14 Waldemar LINK

- 16.15 ZIMMER BIOMET