|

시장보고서

상품코드

1876812

마이크로캡슐화 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Microencapsulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

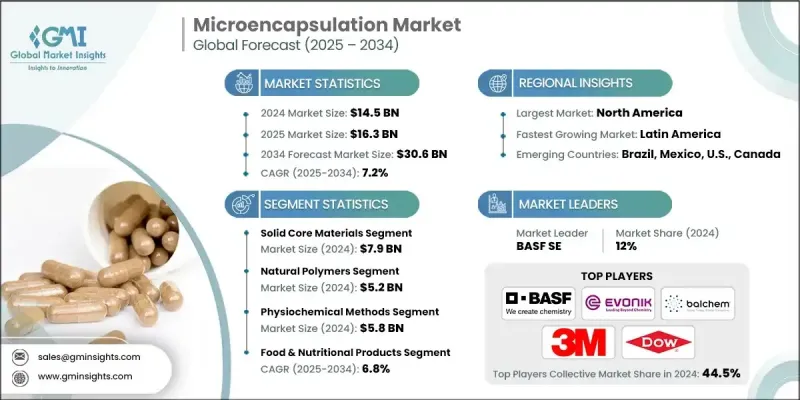

세계의 마이크로캡슐화 시장은 2024년에 145억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 7.2%를 나타내 306억 달러에 이를 것으로 예측됩니다.

제어된 약물전달 시스템의 채용 증가는 마이크로캡슐화 수요를 견인하고 있습니다. 이는 유효성분의 정밀한 보호와 제어된 방출을 실현하기 때문입니다. 영양 강화와 식품의 영양 강화에 대한 관심 증가는 시장 성장을 더욱 촉진하고 있으며, 각국에서는 영양 부족 대책 프로그램을 실시했습니다. 식품, 영양 보충 식품, 의약품에서의 기능성 성분의 안정성, 생물학적 이용능력, 보존 기간의 개선 니즈의 높아짐이, 본 기술의 중요성을 높이고 있습니다. 게다가 세계적인 지속가능성에 대한 노력으로 알긴산염이나 리그닌 유도체 등 생분해성·바이오계 코팅재료의 사용이 가속화되고 있습니다. 이들은 환경 및 규제 기준에도 적합합니다. 업계가 건강 지향적이고 환경 친화적 인 처방으로 전환하는 동안 마이크로 캡슐화 기술은 원료 효율성과 소비자에게 호소력을 높이는 데 필수적입니다. 강력한 규제 지원, 향상된 건강 지향 추세, 캡슐화 기술의 진보가 이 시장의 세계적인 꾸준한 확대를 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 145억 달러 |

| 예측 금액 | 306억 달러 |

| CAGR | 7.2% |

고체 코어 재료 부문은 2024년에 79억 달러를 차지하며 세계 시장에서 가장 큰 점유율을 유지했습니다. 이 이점은 의약품, 영양 보조 식품 및 식품 제품의 광범위한 용도로 인해 발생합니다. 미네랄, 효소, 프로바이오틱스, 비타민 등의 고체 활성 성분은 산화 방지, 안정성 향상, 영양소의 서방을 목적으로 널리 캡슐화되어 있습니다. 이러한 재료는 분무 건조 및 유동층 코팅과 같은 여러 코팅 기술과 효율적으로 협력하여 균일한 입자 형성과 제품의 장기 보존을 실현합니다.

천연 폴리머 부문은 2024년에 52억 달러로 평가되었으며 코팅재료에서 주도적인 점유율을 차지했습니다. 천연 폴리머는 생분해성, 안전성, 식품 등급의 특성으로부터 그 선호가 높아지고 있습니다. 전분, 젤라틴, 알긴산염, 아라비아 검, 셀룰로오스 유도체 등의 물질은 피막 형성 능력과 유효성분과의 뛰어난 상용성으로부터 식품, 의약품, 화장품 용도로 점점 활용되고 있습니다. 지속가능하고 깨끗한 라벨 소재에 대한 수요 급증은 산업 전반에 걸쳐 천연 폴리머계 코팅의 채택을 더욱 촉진하고 있습니다.

북미의 마이크로캡슐화 시장은 2024년 49억 달러에 이르렀으며 34%의 점유율을 차지했습니다. 이 지역은 2034년까지 견조한 성장이 전망되고 있으며, 확립된 의약품·영양보조식품산업을 배경으로 미국이 견인역이 됩니다. 강화 식품, 고급 약물전달 기술, 맞춤형 영양 제품에 대한 수요 증가가 시장 확대를 뒷받침하고 있습니다. FDA(미국 식품의약품국)에 의한 규제면의 지원과 동지역에서의 연구개발에 대한 투자가 캡슐화 프로세스의 혁신을 촉진하고 있습니다. 건강 지향 증가와 선진적인 캡슐화 재료에 대한 접근이 결합되어 북미는 세계 시장의 발전에 크게 공헌하는 지역으로서의 지위를 확립하고 있습니다.

마이크로캡슐화 시장의 주요 기업으로는 Coating Place Inc., Aveka Inc., Syngenta AG, DOW Corning, DSM NV, Ashland Global Holdings Inc., BASF SE, 3M Company, Evonik Industries AG, Balchem Corporation, Capsugel(Lonza Group) 등이 있습니다. 마이크로 캡슐화 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 제품 혁신, 파트너십 및 지속 가능한 기술 개발에 주력하고 있습니다. 많은 기업들이 생물학적 이용능력, 안정성, 서방 특성을 향상시키는 새로운 캡슐화 재료의 개발을 위한 연구개발에 많은 투자를 하고 있습니다. 식품, 의약품, 화장품 제조업체와의 전략적 제휴에 의해 응용 분야의 확대가 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급업체의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 제어된 약물전달 시스템에 대한 수요 증가

- 식품 강화·영양 보조 식품 용도의 확대

- 생분해성 코팅 재료의 채용 확대

- 섬유·기능성 코팅 분야에 있어서 응용 확대

- 업계의 잠재적 리스크 및 과제

- 높은 제조 비용과 설비 투자

- 복잡한 규제 승인 프로세스

- 스케일업 조작에 있어서 기술적 과제

- 시장 기회

- 자기 복구 재료의 새로운 응용 분야

- 맞춤형 의료에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 코어 재료 유형

- 코팅재료

- 기술

- 용도

- 향후 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계·예측 : 코어 재료별(2021-2034년)

- 주요 동향

- 고체 코어 재료

- 의약품 원료의약품(API)

- 비타민 및 미네랄

- 효소 및 프로바이오틱스

- 액체 코어 재료

- 에센셜 오일 및 향료

- 향미제

- 액체 의약품

- 가스 코어 재료

- 산소 및 의료용 가스

- 추진제

- 특수 코어 재료

- 소수성 활성제

- 생물학적 재료(백신, 박테리오파지)

- 상변화 재료(PCMs)

제6장 시장 추계·예측 : 코팅 재료별(2021-2034년)

- 주요 동향

- 천연 고분자

- 젤라틴

- 키토산-알긴산 복합재료

- 실크 피브로인

- 식물 기반 재료

- 합성 고분자

- 폴리비닐 알코올(PVA)

- 에틸셀룰로오스

- 셀룰로오스 아세테이트 프탈레이트(CAP)

- PLGA(폴리유산-코-글리콜릭산)

- 카보폴 중합체

- 복합재료

- 단백질-탄수화물 복합체

- 실리카계 재료

- 포름알데히드-멜라민 수지

- 기타

- 생분해성 폴리머 블렌드

- 스마트 반응성 중합체

- 무기-유기 하이브리드

제7장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 화학적 방법

- 현장 중합

- 계면 중합

- 복합 응집

- 단순 응집

- 물리화학적 방법

- 분무 건조

- 유동층 코팅

- 용매 증발

- 정전기적 방법

- 전기분무

- 전기유체역학적 가공

- 기계적 방법

- 공기 현탁 코팅

- 팬 코팅

- 원심 압출

- 첨단 기술법

- 초임계 유체법(RESS, SAS, GSSP)

- 삼유체 노즐 분무 건조

- 피커링 유화 기반 캡슐화

- 이온 겔화

- 막 유화

- 졸-겔법

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 의약품 및 약물전달

- 경구 약물 전달 시스템

- 비경구 제형

- 국소 및 경피 적용

- 백신 및 생물학적 제제 전달

- 식품 및 영양 제품

- 기능성 식품 및 영양 보급 식품

- 식품 첨가물 및 방부제

- 프로바이오틱스 전달 시스템

- 농약 및 살충제

- 제어 방출 비료

- 살충제 제형

- 종자 코팅 용도

- 산업 용도

- 섬유 및 기능성 코팅

- 건설 및 자가 치유 재료

- 석유 및 가스

- 기상 조절

- 소비재

- 화장품 및 의료용 화장품

- 가정용품 및 퍼스널케어

- 향료 및 아로마테라피

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- DOW Corning

- BASF SE

- Evonik Industries AG

- DSM NV

- Syngenta AG

- 3M Company

- Ashland Global Holdings Inc.

- Coating Place Inc.

- Capsugel(Lonza Group)

- Balchem Corporation

- Aveka Inc.

The Global Microencapsulation Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 30.6 billion by 2034.

The increasing adoption of controlled drug delivery systems is driving demand for microencapsulation, as it offers precise protection and controlled release of active compounds. Rising focus on nutritional enhancement and food fortification has further fueled market growth, with countries implementing programs to address nutrient deficiencies. The growing need for improved stability, bioavailability, and shelf life of functional ingredients in foods, nutraceuticals, and pharmaceuticals has boosted the importance of this technology. Moreover, global sustainability initiatives are accelerating the use of biodegradable and bio-based coating materials, such as alginates and lignin derivatives, which align with environmental and regulatory standards. As industries shift toward health-conscious and eco-friendly formulations, microencapsulation technologies are becoming vital in enhancing ingredient efficiency and consumer appeal. Strong regulatory support, rising wellness trends, and advancements in encapsulation techniques are shaping this market's steady expansion worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $30.6 Billion |

| CAGR | 7.2% |

The solid core materials segment accounted for USD 7.9 billion in 2024, holding the largest share of the global market. This dominance is attributed to their extensive application in pharmaceuticals, nutraceuticals, and food products. Solid actives like minerals, enzymes, probiotics, and vitamins are widely encapsulated to prevent oxidation, enhance stability, and ensure slow release of nutrients. These materials work efficiently with multiple coating technologies such as spray drying and fluidized bed coating, delivering uniform particle formation and extended product shelf life.

The natural polymers segment was valued at USD 5.2 billion in 2024, representing the leading share of coating materials. The preference for natural polymers is growing due to their biodegradable, safe, and food-grade characteristics. Substances such as starch, gelatin, alginate, gum Arabic, and cellulose derivatives are increasingly utilized in food, pharmaceutical, and cosmetic applications because of their film-forming capabilities and excellent compatibility with active ingredients. The surge in demand for sustainable and clean-label materials continues to strengthen the adoption of natural polymer-based coatings across industries.

North America Microencapsulation Market reached USD 4.9 billion in 2024, representing 34% share. The region is expected to witness strong growth through 2034, led by the United States, which benefits from a well-established pharmaceutical and nutraceutical sector. The increasing need for fortified foods, advanced drug delivery technologies, and personalized nutrition products continues to boost market demand. Regulatory support from the FDA and the region's investment in R&D are encouraging innovation in encapsulation processes. The growing focus on wellness, coupled with access to advanced encapsulation materials, has positioned North America as a major contributor to global market development.

Major players operating in the Microencapsulation Market include Coating Place Inc., Aveka Inc., Syngenta AG, DOW Corning, DSM N.V., Ashland Global Holdings Inc., BASF SE, 3M Company, Evonik Industries AG, Balchem Corporation, and Capsugel (Lonza Group). Leading companies in the Microencapsulation Market are focusing on product innovation, partnerships, and sustainable technology development to strengthen their market foothold. Many are investing heavily in R&D to develop new encapsulation materials that improve bioavailability, stability, and controlled release properties. Strategic collaborations with food, pharmaceutical, and cosmetic manufacturers are helping expand application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Core Material Type

- 2.2.3 Coating Material

- 2.2.4 Technology

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for controlled drug delivery systems

- 3.2.1.2 Growing food fortification & nutraceutical applications

- 3.2.1.3 Increasing adoption of biodegradable coating materials

- 3.2.1.4 Expanding applications in textiles & functional coating

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs & equipment investment

- 3.2.2.2 Complex regulatory approval processes

- 3.2.2.3 Technical challenges in scale-up operations

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in self-healing materials

- 3.2.3.2 Growing demand for personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Core Material Type

- 3.7.3 Coating Material

- 3.7.4 Technology

- 3.7.5 Application

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Core Material, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Solid core materials

- 5.2.1 Pharmaceutical APIs

- 5.2.2 Vitamins & minerals

- 5.2.3 Enzymes & probiotics

- 5.3 Liquid core materials

- 5.3.1 Essential oils & fragrances

- 5.3.2 Flavoring agents

- 5.3.3 Liquid pharmaceuticals

- 5.4 Gas core materials

- 5.4.1 Oxygen & medical gases

- 5.4.2 Propellants

- 5.5 Specialized core materials

- 5.5.1 Hydrophobic actives

- 5.5.2 Biological materials (vaccines, bacteriophages)

- 5.5.3 Phase change materials (PCMs)

Chapter 6 Market Estimates and Forecast, By Coating Material, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural polymers

- 6.2.1 Gelatin

- 6.2.2 Chitosan-alginate composites

- 6.2.3 Silk fibroin

- 6.2.4 Plant-based materials

- 6.3 Synthetic polymers

- 6.3.1 Polyvinyl alcohol (PVA)

- 6.3.2 Ethyl cellulose

- 6.3.3 Cellulose acetate phthalate (CAP)

- 6.3.4 PLGA (Poly Lactic-co-Glycolic Acid)

- 6.3.5 Carbopol polymers

- 6.4 Composite materials

- 6.4.1 Protein-carbohydrate combinations

- 6.4.2 Silica-based materials

- 6.4.3 Formaldehyde-melamine resins

- 6.5 Others

- 6.5.1 Biodegradable polymer blends

- 6.5.2 Smart responsive polymers

- 6.5.3 Inorganic-organic hybrids

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Chemical methods

- 7.2.1 In-situ polymerization

- 7.2.2 Interfacial polymerization

- 7.2.3 Complex coacervation

- 7.2.4 Simple coacervation

- 7.3 Physiochemical methods

- 7.3.1 Spray drying

- 7.3.2 Fluid bed coating

- 7.3.3 Solvent evaporation

- 7.4 Electrostatic methods

- 7.4.1 Electro spraying

- 7.4.2 Electrohydrodynamic processing

- 7.5 Mechanical methods

- 7.5.1 Air suspension coating

- 7.5.2 Pan coating

- 7.5.3 Centrifugal extrusion

- 7.6 Advanced technology methods

- 7.6.1 Supercritical fluid methods (RESS, SAS, GSSP)

- 7.6.2 Three-fluid nozzle spray drying

- 7.6.3 Pickering emulsion-based encapsulation

- 7.6.4 Ionic gelation

- 7.6.5 Membrane emulsification

- 7.6.6 Sol-gel methods

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceuticals & drug delivery

- 8.2.1 Oral drug delivery systems

- 8.2.2 Parenteral formulations

- 8.2.3 Topical & transdermal applications

- 8.2.4 Vaccine & biological delivery

- 8.3 Food & nutritional products

- 8.3.1 Functional foods & nutraceuticals

- 8.3.2 Food additives & preservatives

- 8.3.3 Probiotic delivery systems

- 8.4 Agrochemicals & pesticides

- 8.4.1 Controlled release fertilizers

- 8.4.2 Pesticide formulations

- 8.4.3 Seed coating applications

- 8.5 Industrial applications

- 8.5.1 Textiles & functional coatings

- 8.5.2 Construction & self-healing materials

- 8.5.3 Oil & gas applications

- 8.5.4 Weather modification

- 8.6 Consumer products

- 8.6.1 Cosmetics & dermo cosmetics

- 8.6.2 Household & personal care

- 8.6.3 Fragrance & aromatherapy

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 DOW Corning

- 10.2 BASF SE

- 10.3 Evonik Industries AG

- 10.4 DSM N.V.

- 10.5 Syngenta AG

- 10.6 3M Company

- 10.7 Ashland Global Holdings Inc.

- 10.8 Coating Place Inc.

- 10.9 Capsugel (Lonza Group)

- 10.10 Balchem Corporation

- 10.11 Aveka Inc.